1. What are the major growth drivers for the Industrial Diamond Market market?

Factors such as are projected to boost the Industrial Diamond Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

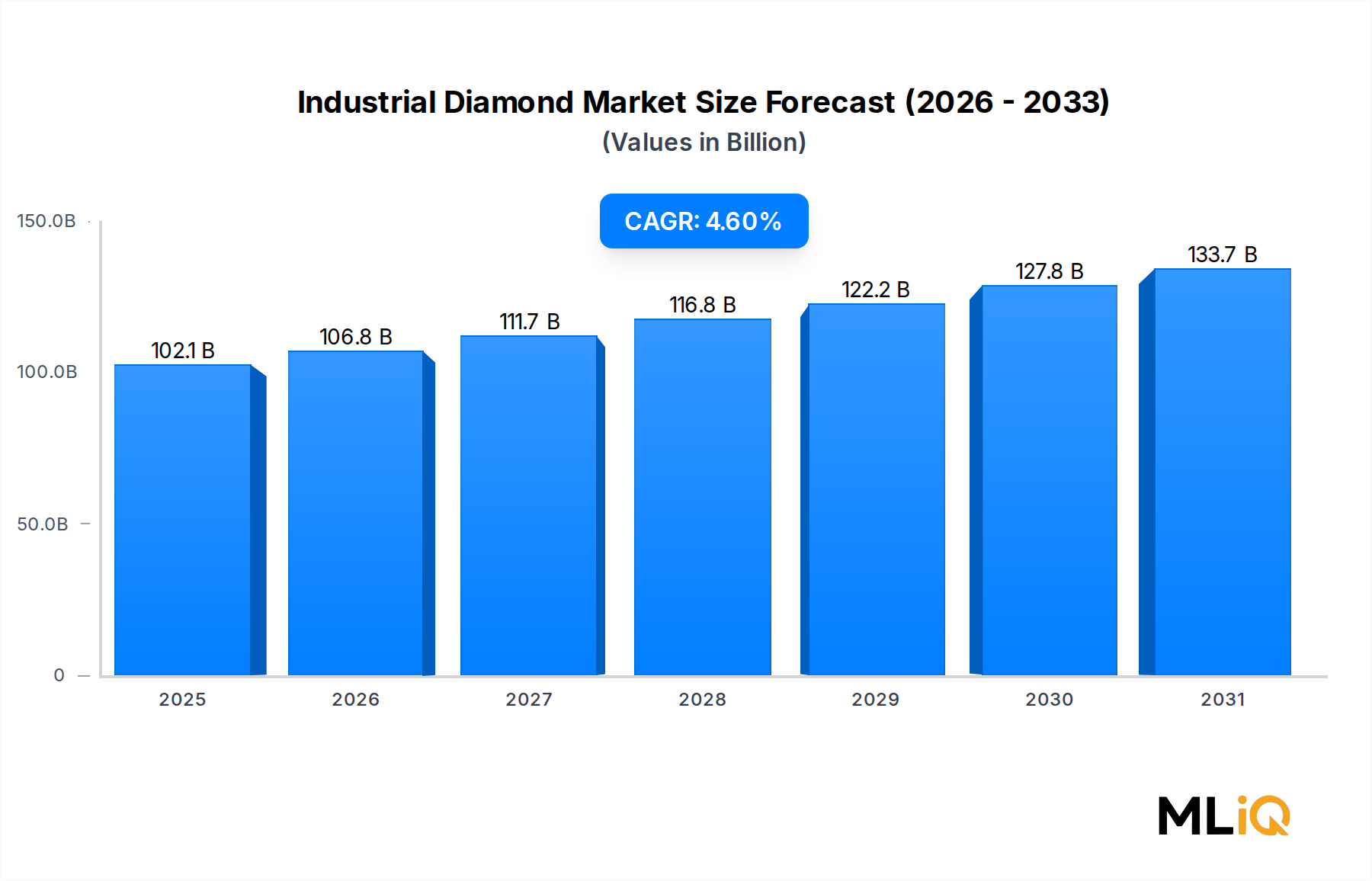

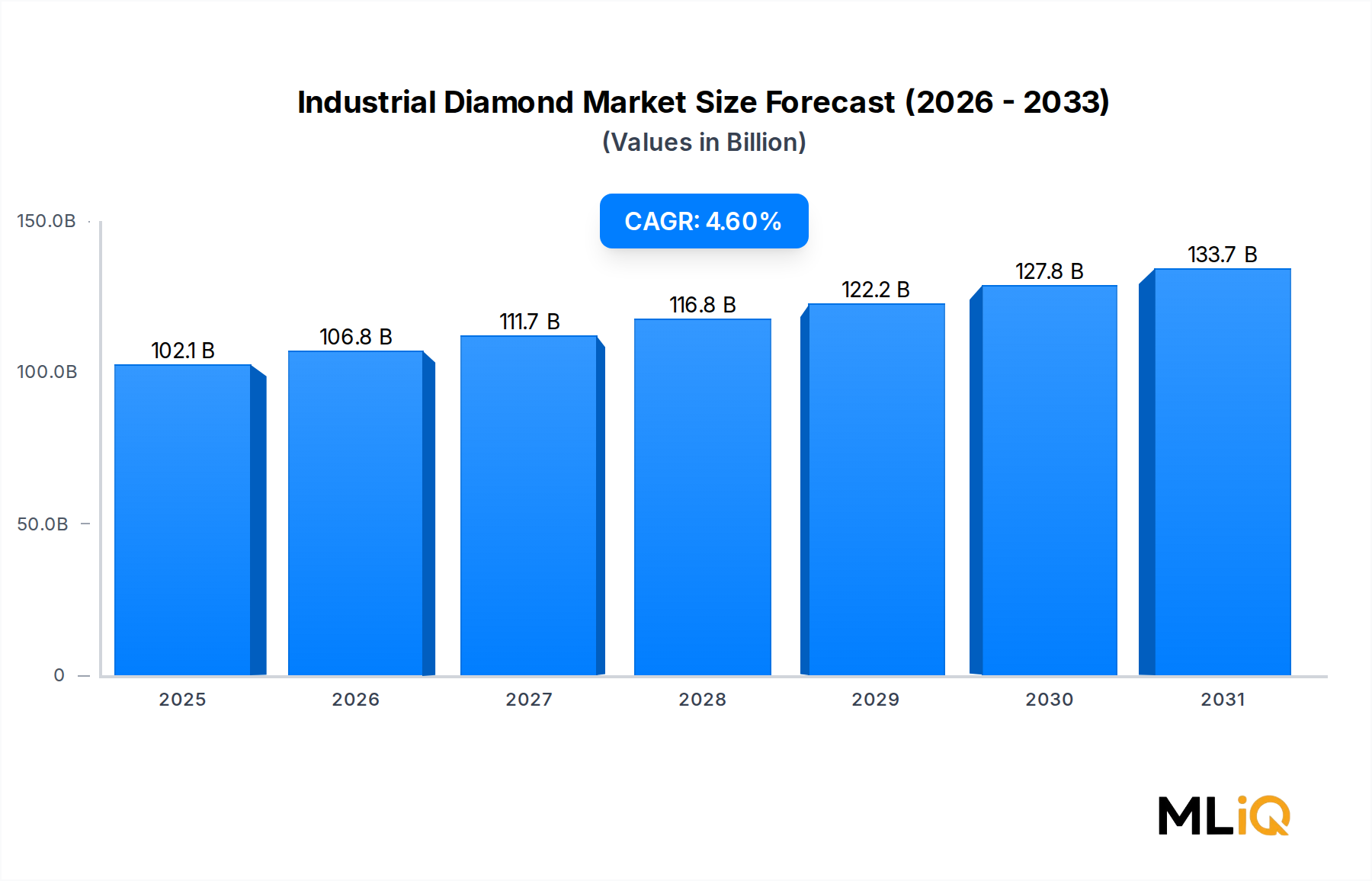

The global Industrial Diamond Market is valued at $102.06 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4.6% through 2033, reflecting robust and sustained demand across construction, mining, machinery manufacturing, and transportation infrastructure sectors. This valuation positions industrial diamonds as one of the most strategically vital material segments within the broader Materials and Chemicals category, underpinned by their unmatched hardness, thermal conductivity, and wear resistance properties.

Several macro-level tailwinds are converging to propel this market forward. Global infrastructure development programs — particularly in Asia Pacific and the Middle East — are driving consumption of diamond-tipped cutting, grinding, and drilling tools at an accelerating pace. Simultaneously, the rapid industrialization of emerging economies in South and Southeast Asia is fueling demand from machinery manufacturing and transportation system development, two segments that collectively account for a significant share of total industrial diamond consumption.

On the supply side, the ongoing transition from natural to synthetic variants is reshaping cost structures and enabling greater scalability. Synthetic production methods, including high-pressure high-temperature (HPHT) and chemical vapor deposition techniques, are delivering consistent quality at lower per-unit costs, attracting procurement teams across heavy industries. This shift is also democratizing access, enabling mid-tier manufacturers in India, South Korea, and ASEAN nations to adopt diamond-based tooling solutions previously reserved for high-budget operations.

From a forward-looking perspective, the market is expected to benefit from increasing automation and precision manufacturing trends. As industries adopt tighter tolerances and advanced materials — including composites, ceramics, and hardened steels — the demand for superhard cutting and finishing solutions will intensify. The proliferation of electric vehicles is also generating indirect demand, as diamond tools are increasingly used in battery component manufacturing and lightweight chassis fabrication.

Geopolitically, supply chain diversification strategies adopted post-2020 are encouraging regional self-sufficiency in diamond tool manufacturing, particularly across North America and Europe. This is driving capital investment in domestic synthesis and tooling facilities, a trend expected to sustain above-average growth rates in these mature markets through the forecast period. Overall, the Industrial Diamond Market presents a compelling investment thesis supported by structural demand drivers, technological evolution, and favorable macroeconomic conditions extending well beyond 2033.

The synthetic segment represents the dominant revenue-generating category within the Industrial Diamond Market, accounting for the majority of global volumes and exhibiting a growth trajectory that is outpacing the natural segment by a meaningful margin. This dominance is not incidental — it is the result of decades of technological refinement, cost optimization, and the growing industrial preference for standardized, scalable material inputs.

Synthetic diamonds are produced primarily via two methods: high-pressure high-temperature (HPHT) synthesis and chemical vapor deposition (CVD). HPHT remains the workhorse of industrial production, generating micron-scale and grit-sized diamonds used in abrasives, grinding wheels, and saw blades. CVD, while more capital-intensive, is gaining ground in precision applications requiring thin-film coatings, semiconductor substrates, and high-performance cutting inserts. The bifurcation of these two production pathways allows manufacturers to serve a spectrum of price-performance requirements, from commodity abrasives to high-value engineered components.

China is the uncontested leader in synthetic diamond production, with manufacturers in Henan Province alone contributing an estimated majority of global HPHT diamond output. Companies such as Hebei Plasma Diamond have invested heavily in large-scale synthesis reactors and process automation, enabling them to offer competitive pricing to both domestic and export markets. This concentration of production capacity in China introduces supply chain dependencies that are increasingly scrutinized by buyers in North America and Europe.

In response, Western and Japanese producers are accelerating R&D and capacity expansion in CVD-based synthesis. Sumitomo Electric, one of Japan's foremost advanced materials conglomerates, has leveraged its deep expertise in powder metallurgy and hard materials to develop high-purity CVD diamond products targeting semiconductor and precision machining applications. Similarly, Scio Diamond Technology Corporation in the United States has positioned itself as a vertically integrated CVD diamond producer, emphasizing quality consistency and domestic supply security.

The synthetic segment's dominance is also reinforced by the cost economics of natural diamond extraction. Natural industrial diamonds, sourced primarily as by-products of gem-quality mining operations in Russia, Australia, and the Democratic Republic of Congo, are subject to volatile supply volumes and elevated logistics costs. Their quality variability further complicates standardization in high-volume manufacturing environments, making synthetics the default choice for engineering-grade applications.

Market consolidation within the synthetic segment is a notable trend, with larger players acquiring niche producers to broaden their product portfolios and geographic reach. Advanced Diamond Solutions Inc. and Applied Diamond Inc. exemplify this pattern, both expanding their application-specific product lines to address emerging demand in aerospace composites, medical device manufacturing, and photonics. The synthetic segment's share of total industrial diamond revenue is expected to continue growing through 2033, driven by cost parity improvements, quality advancements, and the expanding range of industries adopting synthetic diamond-based solutions. The Synthetic Diamond Market is itself a high-growth sub-vertical that commands dedicated analyst coverage and specialized investment frameworks.

Several quantifiable drivers and measurable constraints shape the trajectory of the Industrial Diamond Market, and a data-centric examination reveals a nuanced balance between expansionary forces and structural headwinds.

Construction sector activity is the primary demand driver, accounting for a substantial share of industrial diamond consumption globally. Global construction output is projected to reach approximately $15 trillion annually by 2030 according to industry forecasts, with diamond-tipped saw blades, core drills, and wire saws serving as essential tools for concrete cutting, stone processing, and road surfacing. The Belt and Road Initiative alone has catalyzed hundreds of infrastructure projects across Asia, Africa, and Eastern Europe, each requiring significant quantities of diamond tooling.

Mining services represent another high-intensity demand vector. Diamond drill bits and polycrystalline diamond compact (PDC) cutters are indispensable in oil and gas exploration, mineral extraction, and geotechnical investigation. The Mining Equipment Market is closely correlated with the Industrial Diamond Market, and as global energy transition investments drive expanded lithium, cobalt, and rare earth mining, demand for diamond-enhanced drilling tools is projected to grow commensurately.

Machinery manufacturing is a third driver, with precision grinding and finishing operations across automotive, aerospace, and electronics supply chains consuming significant volumes of diamond abrasive products. The global shift toward high-hardness materials — including silicon carbide, zirconia, and hardened tool steels — is structurally increasing diamond abrasive consumption per unit of manufactured output.

On the constraint side, raw material price volatility poses a persistent challenge. The cost of graphite precursors and high-purity carbon feedstocks — critical inputs in HPHT and CVD synthesis — has experienced meaningful fluctuation due to supply chain disruptions and energy price inflation. Additionally, the high capital expenditure required to establish synthesis facilities creates barriers that limit new entrants and slow capacity expansion responses to demand spikes. Environmental regulations governing synthesis energy consumption are also tightening in the European Union and parts of Asia, adding compliance costs that could compress margins for smaller producers.

The competitive landscape of the Industrial Diamond Market is fragmented at the mid-tier but increasingly concentrated at the premium end, with a mix of vertically integrated global conglomerates and specialized regional producers.

Novatek: A leading manufacturer of polycrystalline diamond compact cutters and drill bits, Novatek holds a strong position in the oil and gas drilling segment, supplying PDC technology to major exploration companies across North America and the Middle East.

Sumitomo Electric: A diversified Japanese industrial giant, Sumitomo Electric's hard materials division produces a wide range of diamond cutting tools and CVD diamond products, with strong market presence in Japan, South Korea, and Europe.

Worldwide Diamond Manufacturers Pvt. Ltd.: An India-based producer of synthetic diamond grits and powders, this company serves the abrasives, lapping, and polishing segments and benefits from competitive labor and energy costs in its domestic manufacturing base.

Advanced Diamond Solutions Inc.: Focused on engineered diamond solutions for precision industries, this company has carved a niche in high-performance cutting and wear applications, with growing exposure to semiconductor and photonics end-markets.

Applied Diamond Inc: A U.S.-based specialist in CVD diamond components, Applied Diamond Inc. serves defense, optical, and scientific instrumentation markets where material purity and thermal performance are paramount.

Diamond Technologies Inc.: This company provides diamond-coated tooling and surface treatment services to the automotive and aerospace industries, emphasizing tool life extension and surface quality improvements.

Scio Diamond Technology Corporation: As a vertically integrated U.S. CVD diamond producer, Scio Diamond Technology Corporation has developed proprietary reactor designs and targets both industrial and near-gem quality markets, differentiating on domestic supply reliability.

Diamonex: A producer of diamond-like carbon coatings and CVD diamond films, Diamonex serves optical, medical, and electronics applications, leveraging thin-film deposition expertise developed over several decades.

Morgan Technical Ceramics: Part of a broader advanced materials group, Morgan Technical Ceramics integrates diamond into ceramic composite components for high-wear industrial environments, offering hybrid solutions that combine the hardness of diamond with the formability of ceramics. The Advanced Ceramics Market intersects significantly with this company's strategic positioning.

Industrial Abrasives Limited: A specialty abrasives producer with a broad diamond grit product line, this company serves grinding wheel manufacturers and surface preparation equipment makers across multiple continents.

Hebei Plasma Diamond: One of China's prominent synthetic diamond producers, Hebei Plasma Diamond leverages large-scale HPHT synthesis capacity and competitive domestic energy pricing to serve both Chinese and export markets at volume.

January 2024: Sumitomo Electric announced the expansion of its CVD diamond production facility in Osaka, targeting a 30% increase in output capacity to meet growing demand from the semiconductor and precision machining sectors.

March 2024: Scio Diamond Technology Corporation entered into a strategic supply agreement with a major U.S. defense contractor for high-purity CVD diamond windows used in directed-energy weapon systems, signaling growing defense sector adoption.

June 2024: The European Commission published updated guidelines on the environmental impact assessment of synthetic diamond manufacturing, requiring producers operating in the EU to report energy consumption and carbon intensity metrics starting 2025.

September 2024: Novatek launched a next-generation PDC drill bit series featuring a redesigned diamond cutter geometry that reportedly delivers 15% longer service life in hard-rock drilling applications, validated through field trials in the Permian Basin.

November 2024: Hebei Plasma Diamond completed a joint venture agreement with a South Korean tooling manufacturer to establish a co-production facility in Incheon, targeting the growing Abrasive Tools Market in Northeast Asia.

February 2025: Advanced Diamond Solutions Inc. secured Series B funding to accelerate commercialization of its diamond-based thermal management substrates, targeting the electric vehicle battery packaging and high-power electronics markets.

April 2025: Morgan Technical Ceramics unveiled a new line of diamond-ceramic composite wear parts for mining conveyor systems, developed in partnership with a major Australian iron ore producer to address extreme abrasion conditions.

The Industrial Diamond Market exhibits significant regional heterogeneity in terms of growth rates, demand composition, and supply chain maturity, with Asia Pacific emerging as the dominant and fastest-growing region while North America maintains technological leadership.

Asia Pacific commands the largest regional share of global industrial diamond revenue, driven overwhelmingly by China's position as both the world's largest producer and consumer of synthetic diamonds. China's infrastructure investment programs, its expansive manufacturing base, and its growing mining services sector collectively generate demand that no other single nation approaches. India is the second-most significant Asia Pacific market, with diamond tool consumption rising sharply as the country scales up highway construction, metro rail networks, and precision manufacturing under its Make in India initiative. The Asia Pacific region is projected to sustain a CAGR of approximately 5.8% through 2033, making it the fastest-growing major region in this market. The Construction Materials Market is a key co-driver of regional demand.

North America represents the most technologically advanced regional market, with the United States leading in CVD diamond innovation, PDC drill bit development, and precision tooling applications. The region's demand is closely linked to oil and gas exploration activity, aerospace manufacturing, and semiconductor fabrication. North American market growth is projected at approximately 3.9% CAGR through 2033, reflecting a more mature base but sustained by technology-driven replacement cycles and reshoring of advanced manufacturing.

Europe is characterized by high-value, low-volume demand, with Germany, France, and the United Kingdom driving consumption through their precision engineering and automotive manufacturing sectors. The region's regulatory focus on sustainable manufacturing is encouraging investment in energy-efficient CVD synthesis and recycled diamond abrasive programs. European market growth is forecast at approximately 3.5% CAGR through 2033.

The Middle East and Africa region is emerging as a meaningful growth market, underpinned by Gulf Cooperation Council infrastructure programs and sub-Saharan mineral extraction activities. South Africa and the GCC nations are the primary demand centers, with diamond drilling tools integral to both gold and platinum mining and large-scale urban construction projects. Regional CAGR is estimated at 4.2% through 2033.

South America, while smaller in absolute terms, is gaining momentum driven by Brazil's mining sector and Argentina's growing industrial base, with a projected CAGR of approximately 4.0% through 2033.

Pricing dynamics within the Industrial Diamond Market are governed by a complex interplay of raw material costs, production method economics, competitive intensity, and end-market price sensitivity. Average selling prices for industrial diamond grits and powders have experienced downward pressure over the past decade, primarily due to the massive expansion of Chinese HPHT synthesis capacity, which has commoditized the lower end of the product spectrum. Prices for standard micron-sized synthetic diamond grits have declined by an estimated 20–30% over the past ten years in real terms, compressing margins for producers unable to differentiate on quality or application engineering.

However, the premium end of the market — encompassing CVD diamond films, polycrystalline diamond compact elements, and application-engineered tooling — has maintained stronger pricing power. These products benefit from higher barriers to replication, proprietary process knowledge, and the willingness of end-users in aerospace, defense, and semiconductor fabrication to pay for performance and consistency guarantees. Margin structures at the premium tier are meaningfully superior to commodity grit producers, with gross margins for specialized CVD components reportedly exceeding 40% in some product lines.

The Carbon Materials Market dynamics directly influence input costs for synthetic diamond producers. Graphite feedstock prices, high-purity methane costs for CVD processes, and electricity tariffs — a significant operating cost in energy-intensive HPHT synthesis — collectively determine the cost floor for synthetic diamond production. Energy price inflation experienced in 2022 and 2023 squeezed margins across the synthesis value chain, particularly in Europe where natural gas prices spiked dramatically.

Value chain margin distribution is uneven. Raw grit producers operating at scale in China capture thin margins, while tooling manufacturers that convert grits into finished diamond saw blades, grinding wheels, or drill bits capture a larger share of end-market value through application engineering and brand equity. Distributors operating in fragmented regional markets add further margin layers. This value chain dynamic incentivizes vertical integration, a strategy pursued by leading players to capture a broader margin pool and reduce exposure to commodity price swings in the Superabrasives Market.

The Industrial Diamond Market is characterized by highly concentrated export flows, with China functioning as the de facto global supplier of synthetic diamond grits, powders, and semi-finished abrasive products. Chinese exports of industrial diamonds reach virtually every manufacturing and construction market globally, with major import destinations including the United States, Germany, Japan, South Korea, India, and Brazil. This trade architecture reflects China's unparalleled cost advantage in HPHT synthesis, backed by low energy costs, vertically integrated supply chains, and government-supported industrial policy.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.6% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Industrial Diamond Market market expansion.

Key companies in the market include Novatek, Sumitomo Electric, Worldwide Diamond Manufacturers Pvt. Ltd., Advanced Diamond Solutions Inc., Applied Diamond Inc, Diamond Technologies Inc., Scio Diamond Technology Corporation, Diamonex, Morgan Technical Ceramics, Industrial Abrasives Limited, Hebei Plasma Diamond.

The market segments include Type, End-User Industry.

The market size is estimated to be USD 102.06 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Industrial Diamond Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Industrial Diamond Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.