Dominance of the Stimulation Segment in the Africa Well Intervention Services Market

Among the major service type segments — logging and bottom hole survey, tubing failure and repair, stimulation, artificial lift, and others — stimulation commands the largest revenue share within the Africa Well Intervention Services Market. This dominance is attributable to the high frequency of stimulation jobs required to restore and enhance production from both mature conventional reservoirs and increasingly complex deepwater formations across the continent.

Stimulation services encompass hydraulic fracturing, matrix acidizing, acid fracturing, and chemical treatments designed to improve reservoir permeability and hydrocarbon flow rates. In the African context, matrix acidizing is particularly prevalent in carbonate and sandstone formations found across North Africa and the Niger Delta, where reservoir damage from drilling fluids, scale, and fines migration routinely impairs well productivity. The economics are compelling: a single successful acidizing treatment can restore or increase a well's output by 20% to 60%, delivering rapid payback relative to the cost of intervention.

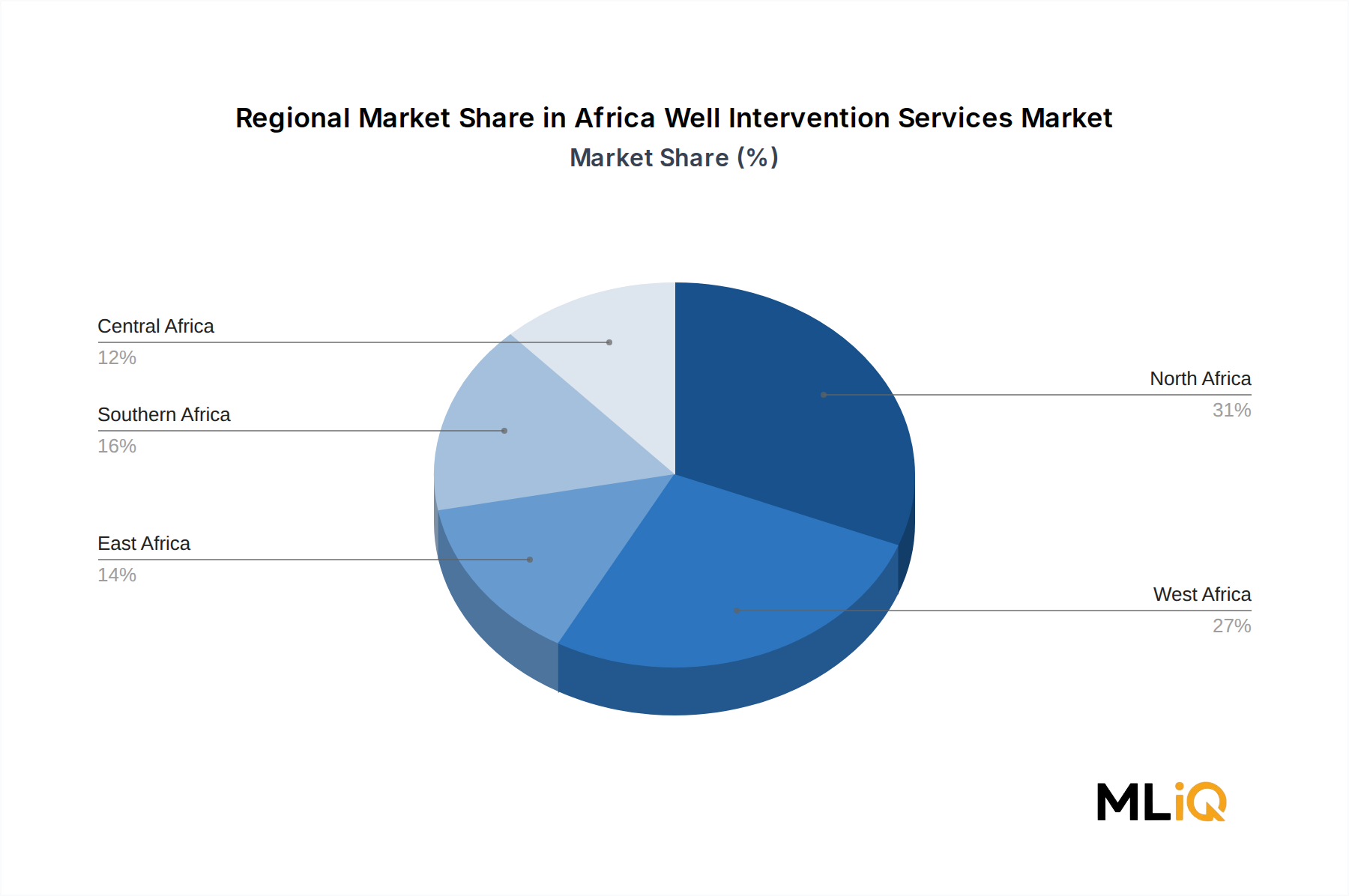

In West Africa, particularly Nigeria and Angola, the complexity of deepwater and pre-salt formations has driven demand for sophisticated hydraulic fracturing and fracture stimulation techniques. Operators are deploying advanced diverter technologies and real-time fracture monitoring to optimize stimulation geometry in heterogeneous reservoirs. Angola's pre-salt Kwanza Basin and Nigeria's deepwater blocks, including Bonga, Egina, and Agbami, represent significant stimulation markets where international service companies have entrenched positions.

North Africa, led by Algeria and Egypt, also represents a substantial stimulation market. Algeria's Hassi Messaoud field — one of Africa's largest producing assets — has seen an increase in stimulation activity as Sonatrach pursues enhanced oil recovery targets. Egypt's Western Desert concessions, operated by a mix of IOCs and independent producers, similarly rely heavily on matrix stimulation to maintain output from aging carbonate reservoirs.

Key players competing for stimulation work in Africa include Halliburton Co., which offers a comprehensive portfolio of stimulation technologies under its Well Completion and Production segment; Baker Hughes Inc., which provides fracturing, acidizing, and specialty chemical stimulation services through its Oilfield Services and Equipment division; and Schlumberger Ltd. (now rebranded as SLB), which has made significant investments in stimulation technology tailored to African reservoir conditions. Weatherford International PLC and Nabors Industries Limited also participate in stimulation-adjacent services, though stimulation is less central to their African portfolios relative to the top three competitors.

The stimulation segment's share is not only dominant but growing. As operators shift focus from conventional to unconventional and tight reservoir plays in North Africa — particularly in Algeria's Ahnet and Timimoun basins — demand for more intensive hydraulic fracturing programs is expected to increase. Moreover, enhanced oil recovery (EOR) initiatives, which frequently incorporate chemical stimulation components, are gaining traction as NOCs seek to maximize recovery factors from fields approaching secondary and tertiary production phases.

The competitive dynamics within stimulation are characterized by technological differentiation. Companies investing in real-time downhole data acquisition, advanced proppant systems, and environmentally adapted stimulation fluids are gaining share over competitors relying on conventional approaches. The segment is expected to maintain its dominant position through 2033, accounting for an estimated 30–35% of total Africa Well Intervention Services Market revenues.