1. What are the major growth drivers for the Industrial Film Industry market?

Factors such as ; Increasing Demand for Packaging in Food Industry; Other Drivers are projected to boost the Industrial Film Industry market expansion.

+1 2315155523

Industrial Film Industry

Industrial Film Industry

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

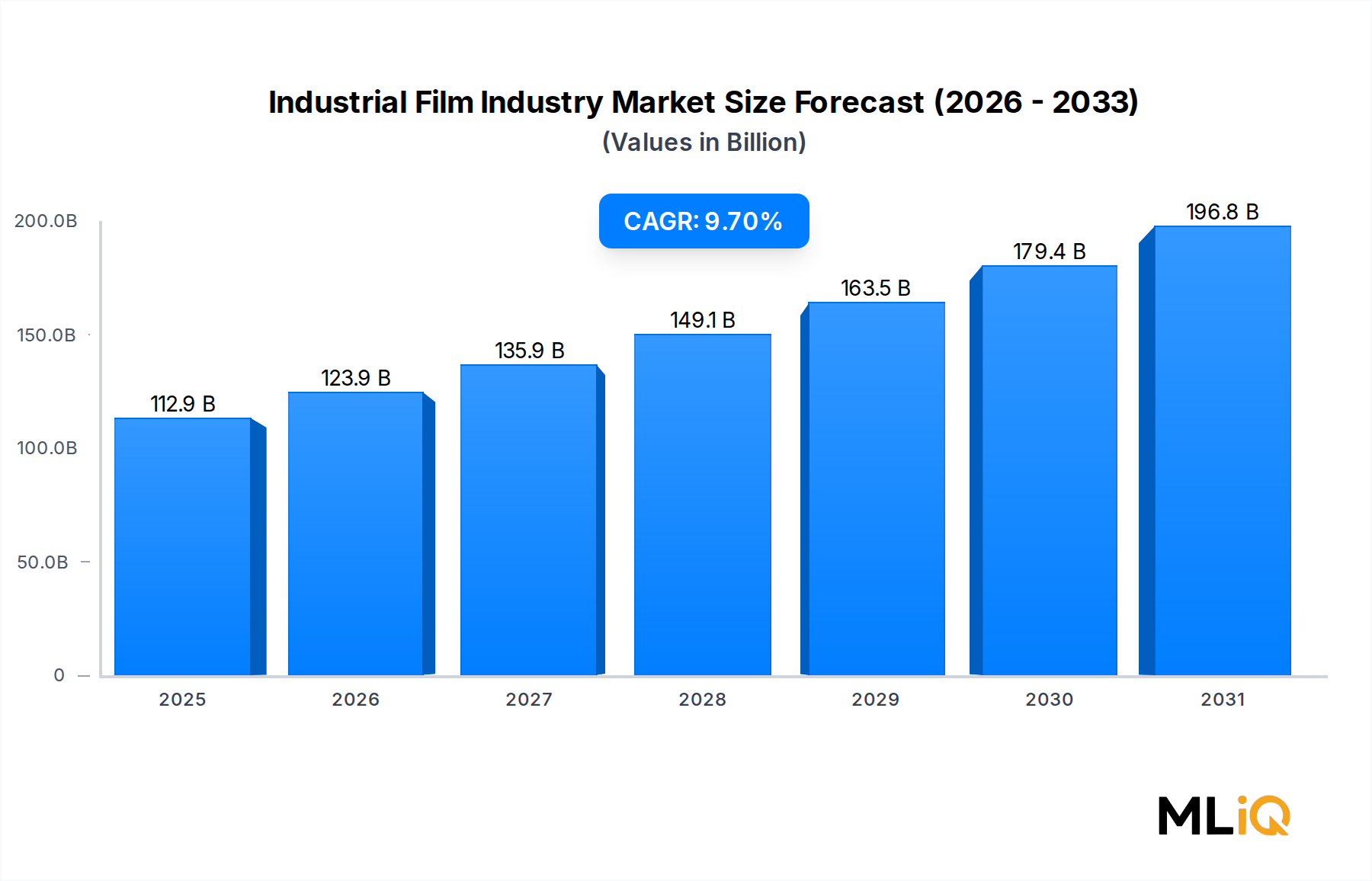

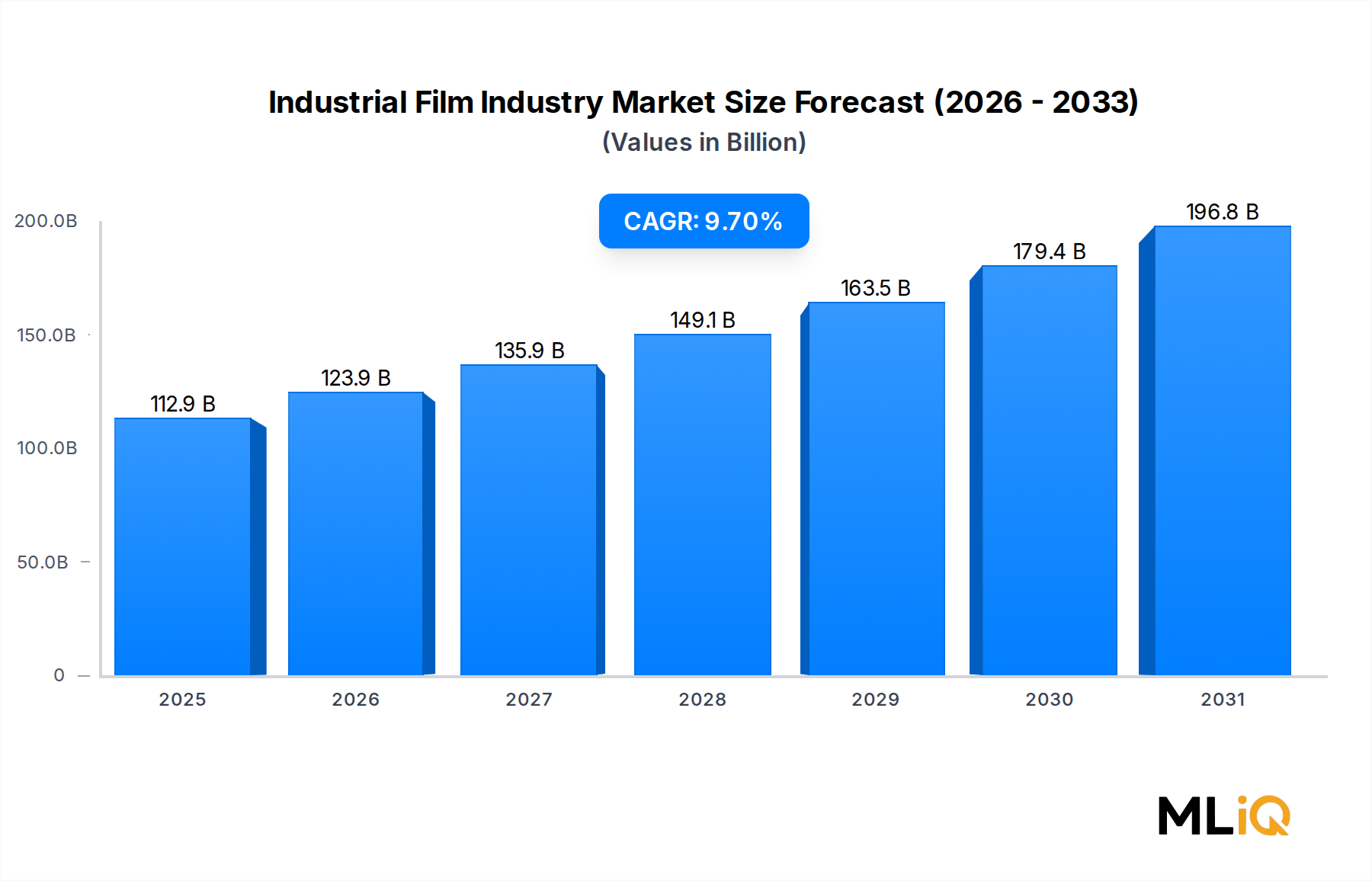

The global Industrial Film Industry Market is valued at $112.93 billion in 2025, advancing at a compound annual growth rate (CAGR) of 9.7% over the forecast period from 2025 to 2033. This robust trajectory reflects accelerating end-use demand across agriculture, packaging, construction, healthcare, and transportation sectors, supported by macro tailwinds including rising global trade volumes, infrastructure investment cycles, and the rapid modernization of agricultural practices in emerging economies.

Industrial films—engineered polymer sheets and membranes used for protective, functional, or aesthetic purposes—are witnessing widening application scope. Food and beverage packaging has emerged as a particularly powerful demand engine, driven by increasing urbanization, e-commerce proliferation, and consumer preference for hygienic, extended-shelf-life packaging solutions. Simultaneously, the agriculture sector is embracing mulch films, silage films, and greenhouse coverings at an accelerated pace, particularly across Asia Pacific and Latin America, where smallholder farm modernization programs are gaining momentum.

The healthcare sector represents a high-value growth vector, with demand for sterile barrier films, medical-grade pouches, and protective wraps escalating in the aftermath of the COVID-19 pandemic. Regulatory emphasis on infection control and single-use sterile packaging continues to buoy healthcare-oriented film demand globally.

On the materials side, polyethylene variants—particularly Linear Low Density Polyethylene (LLDPE) and Low-Density Polyethylene (LDPE)—continue to dominate volume production, benefiting from feedstock availability, process maturity, and cost competitiveness. However, performance polymers such as polyamide and Polyethylene Terephthalate (PET) are gaining share in premium application segments where barrier properties, optical clarity, and dimensional stability are paramount.

From a competitive standpoint, the market features a blend of global polymer conglomerates, regional film converters, and specialty manufacturers. Players are increasingly differentiating through functional coatings, co-extrusion technologies, and recyclable mono-material structures in response to circular economy mandates.

Looking ahead to 2033, the Industrial Film Industry Market is projected to surpass an estimated valuation well above $200 billion at the stated CAGR, underpinned by continued infrastructure expansion in developing markets, digitalization of agricultural value chains, and the structural shift toward sustainable, low-carbon film formulations. Supply chain resilience investments post-pandemic are also prompting nearshoring of film manufacturing capacity, creating localized growth pockets in North America and Europe.

Among all material type segments, polyethylene-based films collectively command the largest revenue share in the Industrial Film Industry Market, with Linear Low Density Polyethylene (LLDPE), Low-Density Polyethylene (LDPE), and High-Density Polyethylene (HDPE) forming a consolidated polyethylene bloc that underpins broad swaths of industrial, agricultural, and packaging film production.

LLDPE holds particular primacy within this cluster. Its unique molecular architecture—characterized by short-chain branching introduced via copolymerization with alpha-olefins such as butene, hexene, or octene—delivers a superior combination of tensile strength, puncture resistance, and elongation at break. These mechanical attributes make LLDPE the preferred substrate for stretch films, pallet wrap, silage films, and heavy-duty shipping sacks, all of which are high-volume, recurring-demand product categories.

The dominance of polyethylene films is further entrenched by feedstock economics. Ethylene, the primary monomer, is derived largely from naphtha cracking in Asia and Europe and from ethane cracking in North America, where the shale gas revolution has kept feedstock costs structurally low. This cost advantage reinforces polyethylene's price competitiveness against alternative polymers such as polypropylene, polyamide, or PET in volume-sensitive applications.

LDPE maintains a strong presence in applications requiring excellent clarity and flexibility, such as shrink films, greenhouse films, and lamination substrates. While LDPE has faced substitution pressure from LLDPE in several segments due to the latter's superior mechanical performance, LDPE retains its position in niche applications where process compatibility with existing blown film lines is valued. HDPE films, characterized by higher stiffness and moisture barrier performance, serve applications in geomembranes, vapor barriers, and heavy-duty industrial liners—segments with steady, non-cyclical demand profiles linked to construction and environmental containment projects.

Key participants shaping this segment include Inteplast Group, which operates one of the largest polyethylene film manufacturing networks in North America, offering a diverse product portfolio spanning agricultural films, packaging films, and industrial covers. Sigma Plastics Group is another major North American force, distinguished by its vertically integrated model that spans resin compounding through finished film conversion. Trioplast Industrier AB is a prominent European player focused on stretch and silage films, consistently investing in thinner-gauge, higher-performance LLDPE formulations that reduce material usage per unit output.

The polyethylene segment's share is in a consolidating phase rather than a rapidly growing one in mature markets, as the addressable volume base is already large. However, in Asia Pacific and Africa, where agricultural modernization and construction activity are still at inflection points, polyethylene film demand is expanding meaningfully. The competitive dynamic is shifting toward functional differentiation—multilayer co-extruded structures, UV-stabilized formulations, and anti-drip greenhouse films—rather than pure price competition, as converters seek margin improvement in an environment of raw material volatility.

Regulatory pressure on single-use plastics is a structural headwind for commodity polyethylene films in European markets, accelerating investment in recyclable monomaterial PE structures and bio-based polyethylene derived from sugarcane ethanol, which several major film producers are piloting at commercial scale.

The Industrial Film Industry Market is propelled by a set of clearly quantifiable drivers while simultaneously navigating a cluster of structural and cyclical restraints.

Driving Force 1 — Food Packaging Demand Escalation: Global food and beverage packaging consumption is estimated to account for approximately 30–35% of total industrial film end-use by volume. Urbanization rates in Asia Pacific, projected to reach 55% by 2030 per United Nations estimates, are driving rapid adoption of packaged food formats. Flexible barrier films incorporating EVOH or metallized PET layers are increasingly specified to meet shelf-life requirements for perishable exports, amplifying demand for high-performance film substrates.

Driving Force 2 — Agricultural Sector Modernization: The global mulch film market alone consumed over 2.5 million metric tons of polyethylene in recent years, with China representing approximately 70% of that volume. Government-backed agronomic programs in India, Brazil, and Southeast Asia are actively subsidizing plasticulture adoption, directly expanding the addressable demand base for Agricultural Plastic Film Market participants and translating into higher procurement volumes for industrial film producers supplying this adjacent segment.

Driving Force 3 — Construction Activity Rebound: Infrastructure stimulus programs, particularly across the United States (Bipartisan Infrastructure Law), the European Union (REPowerEU), and India (National Infrastructure Pipeline), are sustaining demand for vapor retarders, geomembranes, and protective wrap films used in building envelopes and civil engineering projects.

Restraint 1 — COVID-19 Pandemic Legacy Disruptions: The COVID-19 outbreak severely disrupted raw material supply chains, caused sharp polyolefin price spikes, and temporarily collapsed demand from automotive and industrial end-users in 2020 and early 2021. While recovery is well underway, the pandemic exposed concentration risks in Asian petrochemical feedstock supply, prompting buyer-side diversification that has elevated procurement complexity and cost.

Restraint 2 — Regulatory Headwinds on Single-Use Plastics: The European Union Single-Use Plastics Directive and analogous regulations across Canada, the United Kingdom, and several ASEAN nations are restricting specific film applications, creating compliance cost pressures and accelerating the need for reformulation investment across the value chain.

The Industrial Film Industry Market features a diversified competitive landscape spanning multinational polymer groups, regional champions, and specialized film converters:

Cosmo Films Ltd: An India-headquartered BOPP and specialty film manufacturer with a growing global footprint, Cosmo Films is actively expanding its value-added product portfolio including matte films, thermal lamination films, and direct thermal substrates.

Dunmore: A U.S.-based specialty films converter known for precision coating, laminating, and metallizing capabilities, Dunmore serves high-specification markets including aerospace, defense, and energy, where performance over cost is the governing procurement criterion.

Inteplast Group: One of the largest integrated plastics manufacturers in North America, Inteplast Group operates across blown film, injection molding, and profile extrusion, with a particularly strong position in agricultural and industrial packaging film segments.

Jindal Poly Films: A flagship entity of the Jindal Group, this company is among the world's largest producers of BOPP and BOPET films, maintaining significant manufacturing capacity in India and Europe and supplying a broad range of packaging, labeling, and industrial film grades globally.

Kolon Industries: A South Korean diversified materials conglomerate, Kolon Industries is active in polyester and polyamide films, with strategic R&D emphasis on optical films and high-performance specialty substrates for electronics and automotive applications.

Mitsui Chemicals Tohcello Inc: The film business subsidiary of Mitsui Chemicals, this company specializes in functional polyolefin and polyester films, with particular strength in surface protection films and adhesive film solutions for semiconductor and flat-panel display manufacturing.

Polyplex: A global polyester film manufacturer with production facilities across India, Thailand, Turkey, and the United States, Polyplex competes on scale and vertical integration, offering PET film across a wide range of thicknesses and functional coatings.

Raven Industries Inc: Known for its engineered films division, Raven Industries produces geomembranes, silage films, and industrial covers with a focus on durability and UV resistance for agricultural and environmental applications.

Saint-Gobain Performance Plastics: A subsidiary of the Saint-Gobain Group, this entity offers high-performance fluoropolymer, silicone, and engineered plastic films for extreme-environment applications in aerospace, healthcare, and industrial processing.

Sigma Plastics Group: A major North American polyethylene film producer operating multiple plants across the United States, Sigma Plastics serves the retail, foodservice, and industrial packaging sectors with a broad commodity and specialty film offering.

Solvay: A Belgian advanced materials and specialty chemicals group, Solvay's films portfolio is anchored in high-performance polymer substrates including PVDF and specialty fluoropolymer films targeting electronics, clean energy, and industrial filtration markets.

Toyobo Co LTD: A Japanese industrial chemicals and films producer, Toyobo specializes in BOPET and polyamide films with applications spanning food packaging, industrial laminates, and optical display components.

Treofan Group: A European specialist in biaxially oriented polypropylene (BOPP) films, Treofan serves the food packaging, labeling, and tobacco packaging segments with a focus on clarity, barrier performance, and sustainable film development.

Trioplast Industrier AB: A Scandinavian leader in polyethylene films for agriculture and industrial applications, Trioplast is known for its innovation in silage stretch films, agricultural mulch films, and sustainable packaging solutions.

January 2023: Jindal Poly Films announced a capacity expansion at its Nasik manufacturing facility in India, adding BOPET film lines targeting the growing flexible packaging and solar encapsulant film segments.

March 2023: Solvay revealed plans to commercialize a new generation of high-barrier PVDF films for lithium-ion battery separator applications, targeting the rapidly expanding electric vehicle battery supply chain.

June 2023: Treofan Group entered into a strategic development agreement with a major European retail consortium to co-develop fully recyclable monomaterial BOPP-based packaging films compliant with the EU Packaging and Packaging Waste Regulation.

September 2023: Polyplex commissioned a new BOPET film line at its Thailand facility, expanding Asian production capacity by approximately 30,000 metric tons per annum in response to regional demand growth.

November 2023: Cosmo Films Ltd launched a line of compostable and biodegradable specialty films targeting the foodservice sector, positioning the company ahead of anticipated regulatory restrictions in key European markets.

February 2024: Saint-Gobain Performance Plastics secured a long-term supply agreement with a leading U.S. aerospace OEM for high-performance fluoropolymer films used in aircraft interior and thermal management applications.

May 2024: Mitsui Chemicals Tohcello Inc unveiled a new surface protection film series designed for next-generation OLED display panels, incorporating ultra-low adhesive residue chemistry for contamination-sensitive electronics manufacturing environments.

August 2024: Trioplast Industrier AB received European certification for a new agricultural silage film incorporating a minimum of 30% post-consumer recycled polyethylene content, marking a milestone in circular economy compliance for the agricultural films sector.

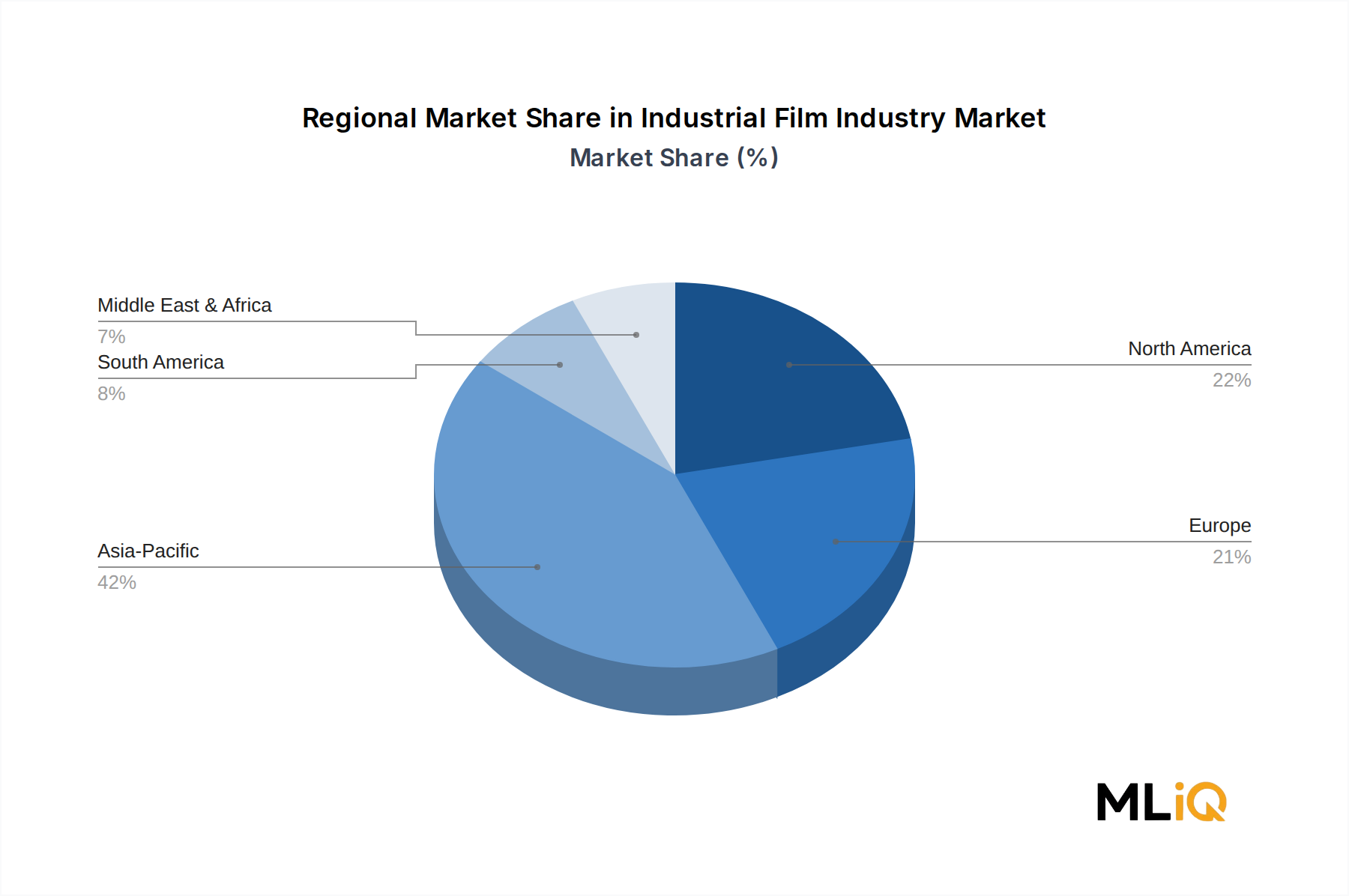

The Industrial Film Industry Market exhibits pronounced regional heterogeneity in terms of growth rates, end-use concentration, and maturity levels.

Asia Pacific: Asia Pacific is both the largest and fastest-growing regional market, accounting for an estimated 45–50% of global industrial film consumption by volume. China remains the dominant national market, fueled by its enormous agricultural sector—where plasticulture adoption covers hundreds of millions of hectares—and its status as the world's largest flexible packaging producer. India is an accelerating secondary growth engine, with domestic film manufacturing capacity expanding rapidly in response to government-backed packaging sector incentives and agricultural modernization schemes. The regional CAGR for Asia Pacific is estimated at approximately 11–12%, outpacing the global average, driven by rising disposable income, food safety regulatory strengthening, and infrastructure investment.

North America: North America represents the second-largest regional market, anchored by the United States, which benefits from a mature food processing industry, advanced cold chain logistics infrastructure, and large-scale agricultural operations reliant on silage and mulch films. The shale-derived ethylene cost advantage sustains competitive domestic polyethylene film manufacturing. Regional CAGR is estimated at 7–8%, reflecting a more mature demand base growing through premiumization—higher-value barrier and functional films—rather than pure volume expansion. Canada and Mexico contribute complementary demand in food packaging and agricultural film categories, respectively.

Europe: Europe's industrial film market is characterized by stringent environmental regulation, a strong emphasis on recyclability, and a sophisticated packaging value chain. Germany, France, the United Kingdom, Italy, and Spain are the primary national markets. Growth is moderated by regulatory-driven volume reductions in single-use film applications, but partially offset by innovation-led demand for sustainable, high-barrier, and bio-based film solutions. Regional CAGR is estimated at 6–7%, with the market evolving qualitatively rather than expanding volumetrically.

Middle East & Africa: This region is an emerging growth zone, particularly Turkey, the GCC countries, South Africa, and North Africa, where construction activity, food processing investments, and agricultural expansion are driving film demand. Regional CAGR is estimated at 9–10%, approaching the global average, reflecting a relatively low base and rapid industrial development.

South America: Brazil and Argentina are the principal markets, with agricultural film demand—particularly silage and mulch films—serving as the primary growth driver given the region's global prominence in soy, corn, and sugarcane production. Regional CAGR is estimated at 8–9%, supported by agribusiness expansion and growing domestic packaging sector sophistication.

Environmental, Social, and Governance (ESG) forces are fundamentally reshaping

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.7% from 2020-2034 |

| Segmentation |

|

Factors such as ; Increasing Demand for Packaging in Food Industry; Other Drivers are projected to boost the Industrial Film Industry market expansion.

Key companies in the market include Cosmo Films Ltd, Dunmore, Inteplast Group, Jindal Poly Films, Kolon Industries, Mitsui Chemicals Tohcello Inc, Polyplex, Raven Industries Inc, Saint-Gobain Performance Plastics, Sigma Plastics Group, Solvay, Toyobo Co LTD, Treofan Group, Trioplast Industrier AB*List Not Exhaustive.

The market segments include Type, End-user Industry.

The market size is estimated to be USD 112.93 billion as of 2022.

; Increasing Demand for Packaging in Food Industry; Other Drivers.

Increasing demand from Agriculture Industry.

; Unfavorable Conditions Arising Due to COVID-19 Outbreak; Other Restraints.

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Industrial Film Industry," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Industrial Film Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.