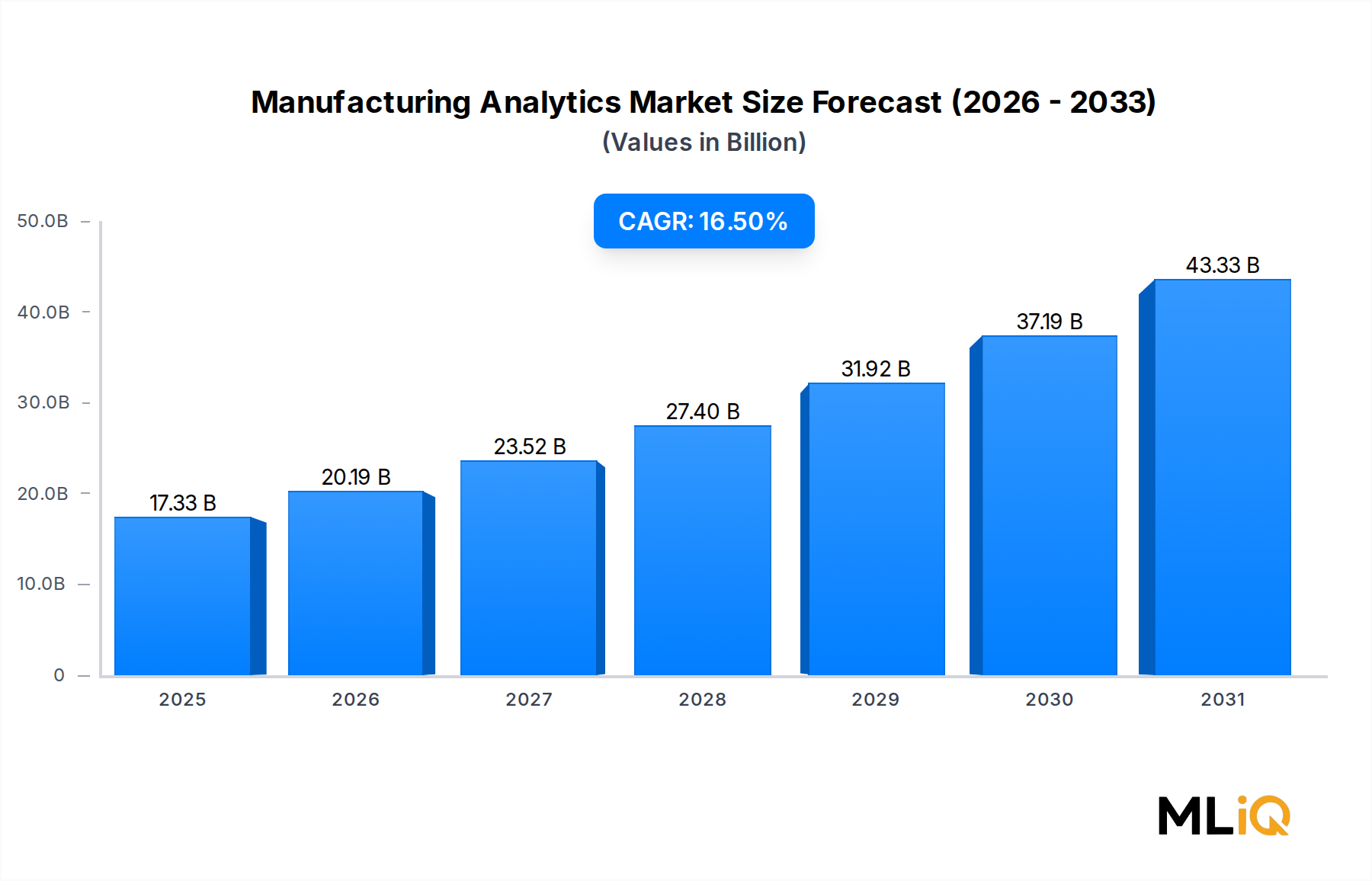

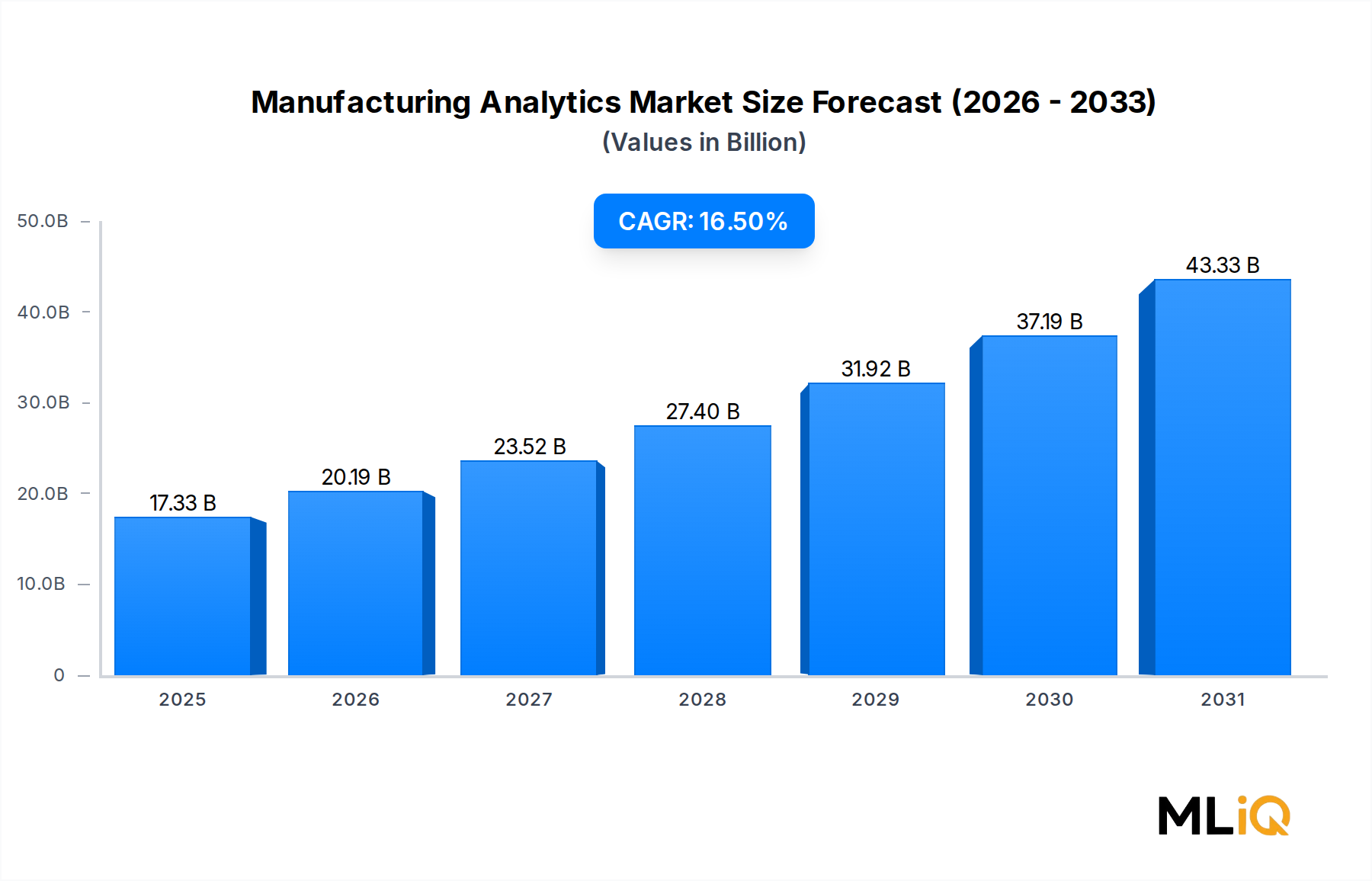

The global Manufacturing Analytics Market is valued at $17,330 million and is projected to expand at a compound annual growth rate (CAGR) of 16.5% over the forecast period, cementing its position as one of the most rapidly scaling verticals within the broader ICT and media landscape. This robust trajectory reflects a fundamental shift in how industrial enterprises approach operational intelligence, quality assurance, and asset utilization.

At its core, the market is propelled by the relentless convergence of operational technology (OT) and information technology (IT) on factory floors worldwide. The proliferation of connected sensors, edge computing nodes, and cloud-native data platforms has generated unprecedented volumes of structured and unstructured manufacturing data, creating an urgent need for advanced analytics frameworks capable of converting raw telemetry into actionable insights. Organizations are under mounting pressure to eliminate unplanned downtime, reduce scrap rates, and optimize throughput in the face of tightening margins and increasingly complex global supply chains.

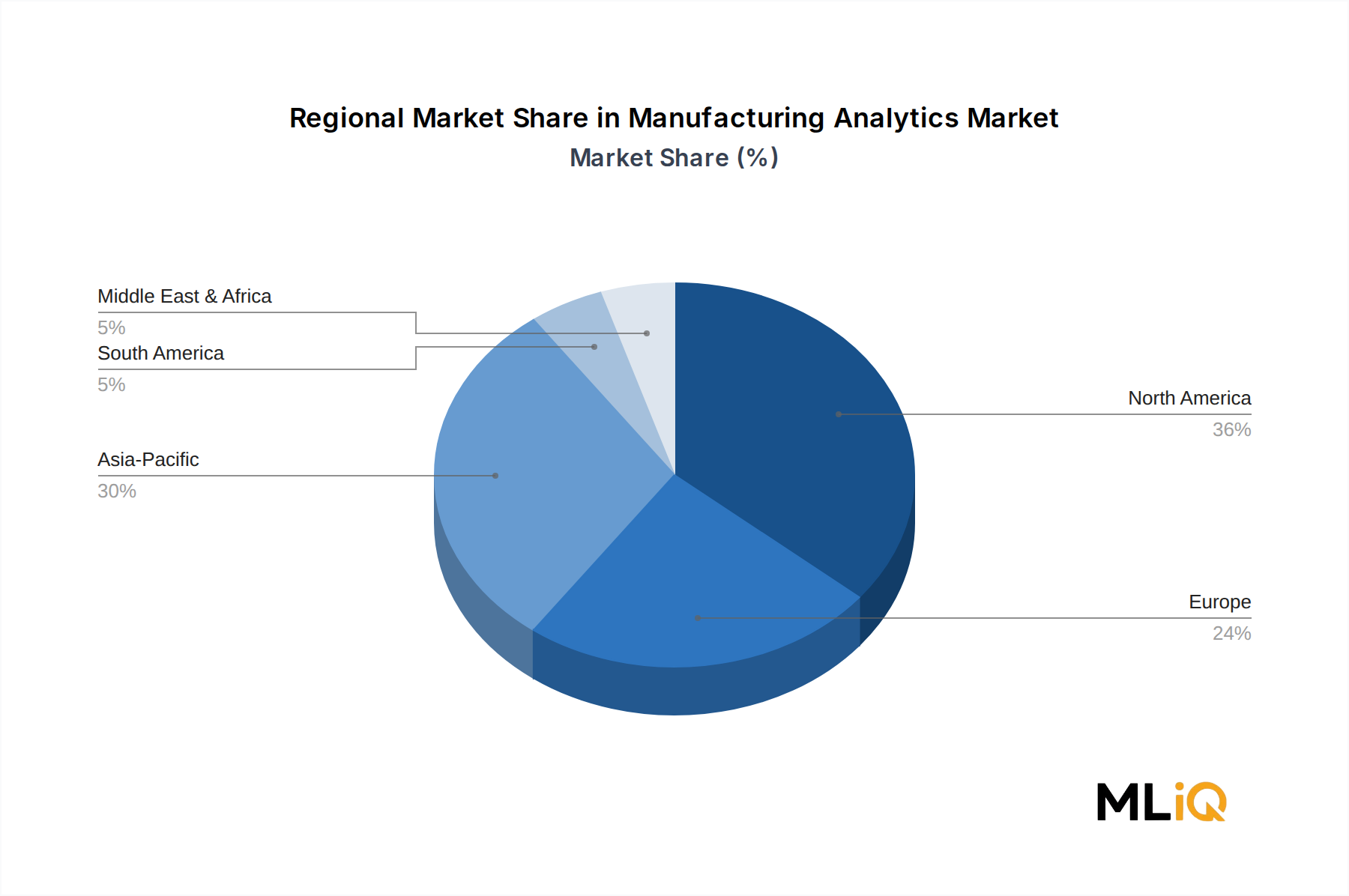

Macro-level tailwinds further reinforce this demand trajectory. Government-backed Industry 4.0 initiatives across Germany, Japan, China, and the United States are directing billions of dollars toward smart manufacturing infrastructure. The post-pandemic reconfiguration of supply chains has accelerated capital deployment into digital resilience tools, with analytics platforms serving as a critical decision-support layer. Rising labor costs in traditional manufacturing hubs are also compelling operators to extract greater productivity from existing assets rather than expanding headcount.

From a segmentation standpoint, software and service components dominate revenue generation, while cloud deployment models are gaining ground over on-premise installations owing to their scalability, lower upfront capital requirements, and faster time-to-value. Application-wise, predictive maintenance commands the largest share, followed closely by supply chain optimization and inventory management, each addressing a distinct pain point in the manufacturing value chain.

The competitive ecosystem is densely populated, featuring global technology conglomerates alongside specialized analytics vendors. Companies such as SAP SE, Oracle Corporation, International Business Machines Corporation, and General Electric are leveraging their installed base advantages, while pure-play analytics providers like Alteryx, Inc. and SAS Institute Inc. compete on depth of statistical modeling and ease of integration.

Looking forward, the intersection of artificial intelligence, the Industrial IoT Market, and cloud scalability is expected to unlock new monetization avenues, including outcome-based pricing models and analytics-as-a-service offerings. By the end of the forecast horizon, the Manufacturing Analytics Market is poised to transition from a competitive differentiator to a baseline operational requirement across virtually every industrial vertical.