1. What are the major growth drivers for the Tire Reinforcement Materials Market market?

Factors such as Increasing Vehicle Usage Across the Globe; Other Drivers are projected to boost the Tire Reinforcement Materials Market market expansion.

+1 2315155523

Tire Reinforcement Materials Market

Tire Reinforcement Materials Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

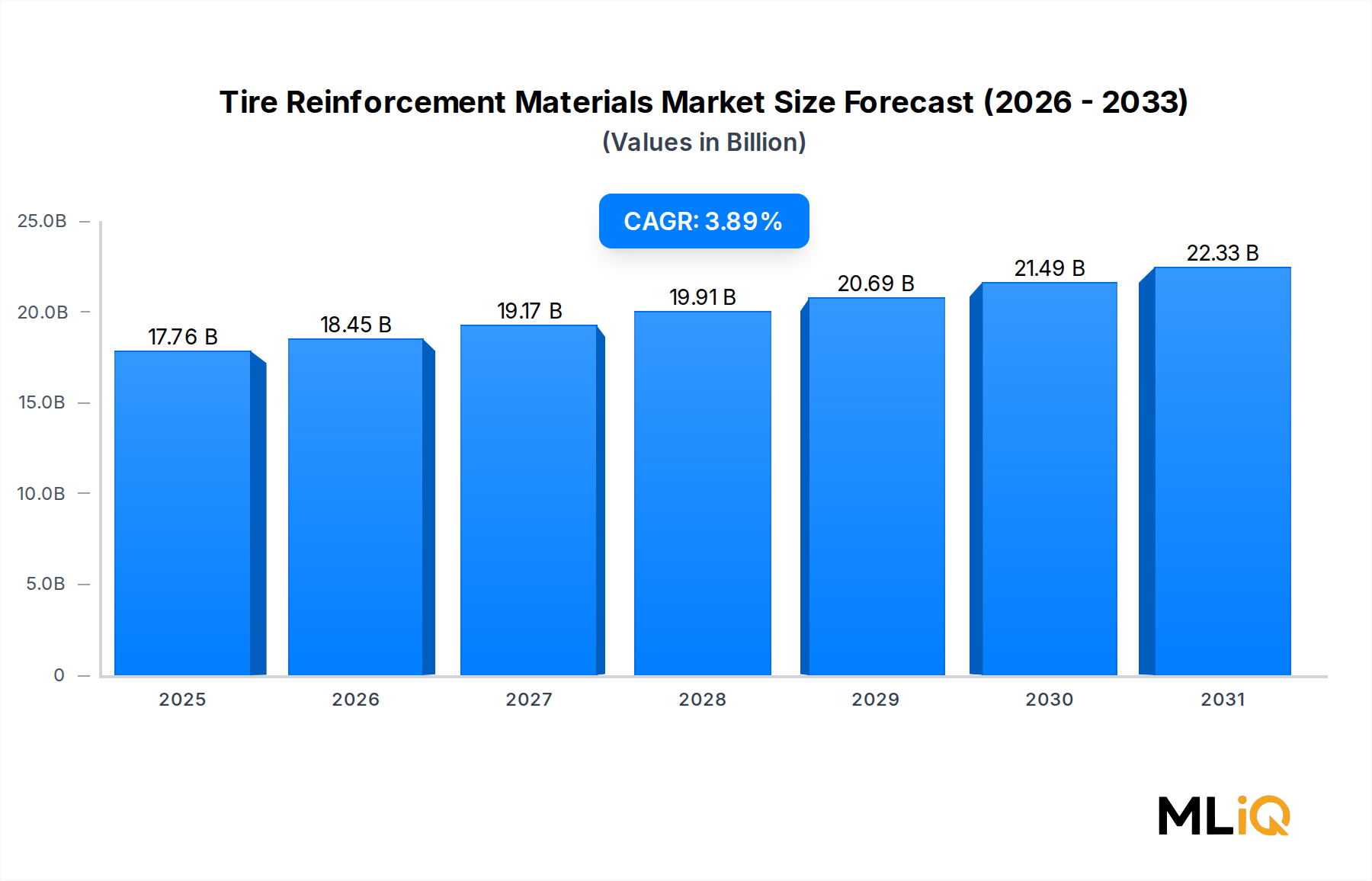

The global Tire Reinforcement Materials Market is valued at $17.76 billion and is projected to expand at a compound annual growth rate (CAGR) of 3.89% through the forecast period. This steady growth trajectory reflects the persistent and rising demand for high-performance, durable tires across passenger vehicles, commercial trucks, off-road equipment, and two-wheelers on a global scale.

The market's forward momentum is underpinned by several structural tailwinds. First, global vehicle production and fleet expansion continue to accelerate, particularly across emerging economies in Asia Pacific and Latin America. Second, tightening regulatory standards on vehicle safety, fuel efficiency, and load-bearing performance compel tire manufacturers to invest in superior reinforcement architectures. Third, the electrification of automotive fleets is introducing new load and torque profiles that demand enhanced structural integrity from tire carcasses, belt plies, and cap plies alike.

Reinforcement materials—including steel wire, polyester yarn, nylon cord, rayon, and aramid fiber—serve as the skeletal backbone of modern tires. Their selection is dictated by application requirements, cost constraints, and performance benchmarks such as tensile strength, fatigue resistance, heat dissipation, and adhesion to rubber matrices. Steel-based materials continue to command the largest revenue share, while high-modulus synthetic fibers are gaining ground in premium and specialty tire segments.

From a macroeconomic perspective, the recovery of global supply chains post-pandemic, stabilization of raw material costs, and resumed automotive manufacturing capacity utilization are collectively restoring market confidence. Infrastructure spending in developing nations is also boosting demand for heavy-duty commercial tires, thereby lifting consumption of steel tire cord and heavyweight nylon cord in belt and bead applications.

Looking ahead, the market is expected to see accelerating adoption of lightweight, high-tenacity synthetic materials as OEM tire brands and independent manufacturers seek to reduce rolling resistance and improve vehicle energy efficiency. Innovations in hybrid cord technologies—combining steel with aramid or polyester—are emerging as a key differentiator. The competitive intensity across material suppliers is high, with capacity expansions underway in China, India, and Southeast Asia, creating both pricing pressure and increased supply reliability.

Overall, the Tire Reinforcement Materials Market is transitioning from a commodity-oriented supply dynamic toward a value-added, performance-engineered ecosystem. Stakeholders who invest in material innovation, process optimization, and sustainability compliance are positioned to capture disproportionate market share over the next decade.

Among all product types within the Tire Reinforcement Materials Market, tire cord fabric stands out as the dominant segment by revenue contribution, accounting for the majority of market value and driving the overall trajectory of the market. Its supremacy stems from its universal application across virtually every tire construction layer—carcass ply, belt ply, and cap ply—making it indispensable to tire structural performance.

Tire cord fabric is a woven or knitted textile structure made from high-tenacity yarns—commonly polyester, nylon, rayon, or aramid—embedded within rubber matrices to provide dimensional stability, tensile strength, and fatigue resistance to the tire body. Unlike tire bead wire, which serves a more localized anchoring function at the rim interface, tire cord fabric distributes mechanical loads uniformly across the tire cross-section, making it central to ride comfort, handling precision, and structural integrity under dynamic operating conditions.

The Tire Cord Fabric Market has been identified in numerous published industry databases as a standalone, high-value market, reflecting its strategic importance and substantial trade volumes. Global demand for tire cord fabric is heavily concentrated in Asia Pacific, where both tire manufacturing hubs and yarn production facilities are co-located, enabling cost-efficient vertical integration. China alone accounts for a dominant share of global tire cord fabric output, supported by large-scale facilities operated by companies such as Jiangsu Xingda Steel Tire Cord Co., Ltd., Jiangsu Taiji Industry New Materials Co., Ltd., and Toray Hybrid Cord Inc.

Polyester-based tire cord fabric continues to grow in share within the passenger car tire segment due to its favorable combination of high modulus, dimensional stability under heat, and cost competitiveness relative to nylon. Nylon cord fabric, however, retains a stronghold in truck, bus, and off-the-road tire applications due to its superior impact resistance and flex fatigue performance at higher load ratings. Rayon cord fabric, though declining in absolute volume due to environmental concerns associated with viscose processing, remains critical for high-performance and motorsport tire applications where thermal stability at elevated temperatures is paramount.

Kordsa Teknik Tekstil AŞ and Kolon Industries Inc. are recognized as leading global suppliers of tire cord fabric, maintaining diversified product portfolios that span polyester, nylon, and hybrid cord systems. SRF Limited and Century Enka Limited are prominent players in the Indian subcontinent, benefiting from lower production costs and proximity to growing domestic tire manufacturing clusters. HYOSUNG and TOYOBO CO., LTD. leverage advanced melt-spinning and solution-spinning technologies to produce differentiated high-tenacity fiber products for premium tire cord applications.

The segment's dominance is expected to consolidate further as tire manufacturers shift toward radial tire architectures globally—even in markets like India and Africa that historically relied on bias-ply designs. Radial tires require greater quantities of high-quality cord fabric per unit, amplifying volume demand per tire produced. In parallel, the push for electric vehicle-compatible tires—which must accommodate heavier battery loads and deliver lower rolling resistance—is accelerating R&D investment into next-generation hybrid cord fabrics that blend the rigidity of aramid with the flexibility of polyester or nylon, reinforcing tire cord fabric's strategic centrality within the market.

The Tire Reinforcement Materials Market is governed by a defined set of demand accelerators and structural constraints that collectively determine its growth ceiling and floor.

Primary Driver — Vehicle Fleet Expansion and Rising Tire Replacement Rates: Global vehicle registrations exceeded 1.4 billion units as of recent counts, with the replacement tire market representing over 70% of total tire demand by volume. Each replacement event creates fresh demand for reinforcement materials embedded in new tires. In Asia Pacific, passenger vehicle CAGR is running above regional GDP growth, creating a structural uplift for tire inputs including steel cord and synthetic fiber cord.

Secondary Driver — Shift to Radial Tire Architecture: Radial tires consume approximately 15–25% more cord fabric per unit than equivalent bias-ply tires due to their multi-ply belt architecture and cap ply construction requirements. As radial penetration rises in commercial vehicle segments across India, Southeast Asia, and Africa, aggregate cord fabric consumption grows disproportionately relative to tire unit volumes. This structural shift is a key volume amplifier for the reinforcement materials supply chain.

Tertiary Driver — Electric Vehicle Tire Requirements: EV tires require reinforcement systems capable of handling torque spikes, higher static loads from battery packs, and reduced noise transmission—conditions that push tire developers toward high-modulus materials such as aramid and hybrid steel-synthetic cord constructions. This creates a premium-segment pull for advanced reinforcement solutions.

Primary Constraint — Environmental Regulatory Pressure on Manufacturing: Tire reinforcement manufacturing—particularly rayon cord production via the viscose process—generates significant volumes of carbon disulfide and hydrogen sulfide, both regulated air pollutants. Compliance with European REACH regulations and equivalent environmental standards in China and India is increasing operating costs for producers, compressing margins and in some cases forcing facility closures. The Steel Tire Cord Market similarly faces elevated environmental compliance costs associated with acid pickling, zinc coating, and wastewater treatment in wire drawing operations.

Secondary Constraint — Raw Material Price Volatility: Tire cord fabrics are downstream of petrochemical feedstocks (for polyester and nylon) and iron ore and coal (for steel cord). Price swings in these upstream commodities—amplified by geopolitical disruptions and energy market instability—create margin compression and demand uncertainty across the reinforcement materials value chain.

The competitive landscape of the Tire Reinforcement Materials Market is characterized by a mix of vertically integrated conglomerates, specialized fiber and wire producers, and regional champions across Asia, Europe, and the Americas.

Bekaert: A global leader in steel wire transformation and coatings, Bekaert commands a dominant position in the steel tire cord segment, supplying advanced high-carbon steel cord systems to major tire OEMs worldwide with a focus on ultra-high-tensile and mega-tensile product grades.

Century Enka Limited: A leading Indian manufacturer of nylon tire cord yarn and fabric, Century Enka serves domestic and export markets with a focus on nylon-6-based products for truck, bus, and two-wheeler tire applications.

CORDENKA GmbH & Co. KG: A specialist in high-tenacity rayon (viscose) tire cord yarn, CORDENKA is the primary global supplier for motorsport and high-performance tire applications requiring superior thermal stability and dimensional precision.

Dupont: A material science innovator with a foundational role in aramid fiber technology through its Kevlar brand, Dupont supplies high-modulus reinforcement fibers used in high-performance and EV-segment tire cord constructions.

FORMOSA TAFFETA CO., LTD.: A diversified Taiwanese textile and materials manufacturer supplying polyester tire cord fabric to tire producers across Asia, leveraging integrated polyester yarn production capabilities.

Glanzstoff Industries: A European producer of high-tenacity rayon and polyester tire cord yarn, Glanzstoff serves premium European tire manufacturers with specialty cord products emphasizing process consistency and adhesion performance.

HYOSUNG: A South Korean industrial materials leader, HYOSUNG is a major global producer of nylon and polyester tire cord yarn and fabric, with large-scale production assets in Korea, Vietnam, and Brazil.

Jiangsu Taiji Industry New Materials Co., Ltd.: A China-based producer of aramid fiber and hybrid cord systems, increasingly supplying domestic tire manufacturers targeting EV and high-performance segments.

Jiangsu Xingda Steel Tire Cord Co., Ltd.: One of China's largest steel tire cord manufacturers, Xingda supplies both domestic and international tire OEMs with a broad portfolio spanning standard, high-tensile, and ultra-high-tensile steel cord.

Kolon Industries Inc.: A South Korean conglomerate with a strong specialty fiber division producing para-aramid (Heracron) and polyester tire cord for global tire OEM supply chains.

Kordsa Teknik Tekstil AŞ: A Turkish technical textiles powerhouse and subsidiary of Sabancı Holding, Kordsa is a global top-three tire cord fabric supplier with production facilities across Turkey, the United States, Brazil, Indonesia, and Thailand.

Michelin: Operating as a vertically integrated tire manufacturer that conducts internal reinforcement materials R&D, Michelin influences material standards globally and sources advanced cord constructions from both internal and external suppliers.

SRF Limited: An Indian specialty chemicals and technical textiles company, SRF is a leading domestic supplier of nylon and polyester tire cord fabric with growing export market presence.

Teijin Ltd.: A Japanese materials company with high-performance fiber competencies in aramid (Twaron licensed) and polyester cord systems for performance tire and industrial applications.

Toray Hybrid Cord Inc.: A joint venture producing hybrid cord systems that combine the properties of carbon fiber, aramid, or nylon with conventional tire cord matrices, targeting ultra-lightweight and EV-optimized tire architectures.

TOYOBO CO., LTD.: A Japanese chemical and fiber company producing high-modulus polyester and Vectran fiber systems with applications in specialty tire reinforcement for motorsport and industrial tires.

March 2024: Bekaert announced a multi-year capacity expansion program for its ultra-high-tensile (UHT) steel tire cord lines at its facilities in Belgium and China, targeting growing OEM demand from electric vehicle tire platforms requiring lighter but stronger bead and belt reinforcement.

January 2024: Kordsa Teknik Tekstil AŞ disclosed a strategic partnership with a leading European EV tire manufacturer to co-develop next-generation hybrid nylon-aramid cap ply constructions designed to reduce rolling resistance by up to 8% while maintaining structural integrity at elevated torque loads.

October 2023: HYOSUNG expanded its polyester tire cord fabric production capacity at its Vietnam facility by 30,000 metric tons per annum, citing surging demand from Southeast Asian tire manufacturing clusters and regional OEM supply chain localization initiatives.

July 2023: Dupont launched an enhanced grade of Kevlar aramid fiber specifically engineered for tire belt ply reinforcement, offering improved rubber adhesion chemistry and reduced processing temperatures during tire building.

April 2023: SRF Limited commissioned a new nylon-6 tire cord fabric production line at its Manesar, India, facility with an annual capacity of 12,000 metric tons, responding to domestic tire industry growth and import substitution policy incentives.

February 2023: Kolon Industries Inc. announced regulatory approval from a major European tire OEM for its Heracron para-aramid fiber in cap ply applications, marking the product's first qualification in the European passenger car OEM segment.

November 2022: CORDENKA GmbH & Co. KG completed a sustainability-focused capital investment to reduce carbon disulfide emissions at its Obernburg, Germany, rayon cord production facility by 40%, in compliance with revised EU industrial emissions directive thresholds.

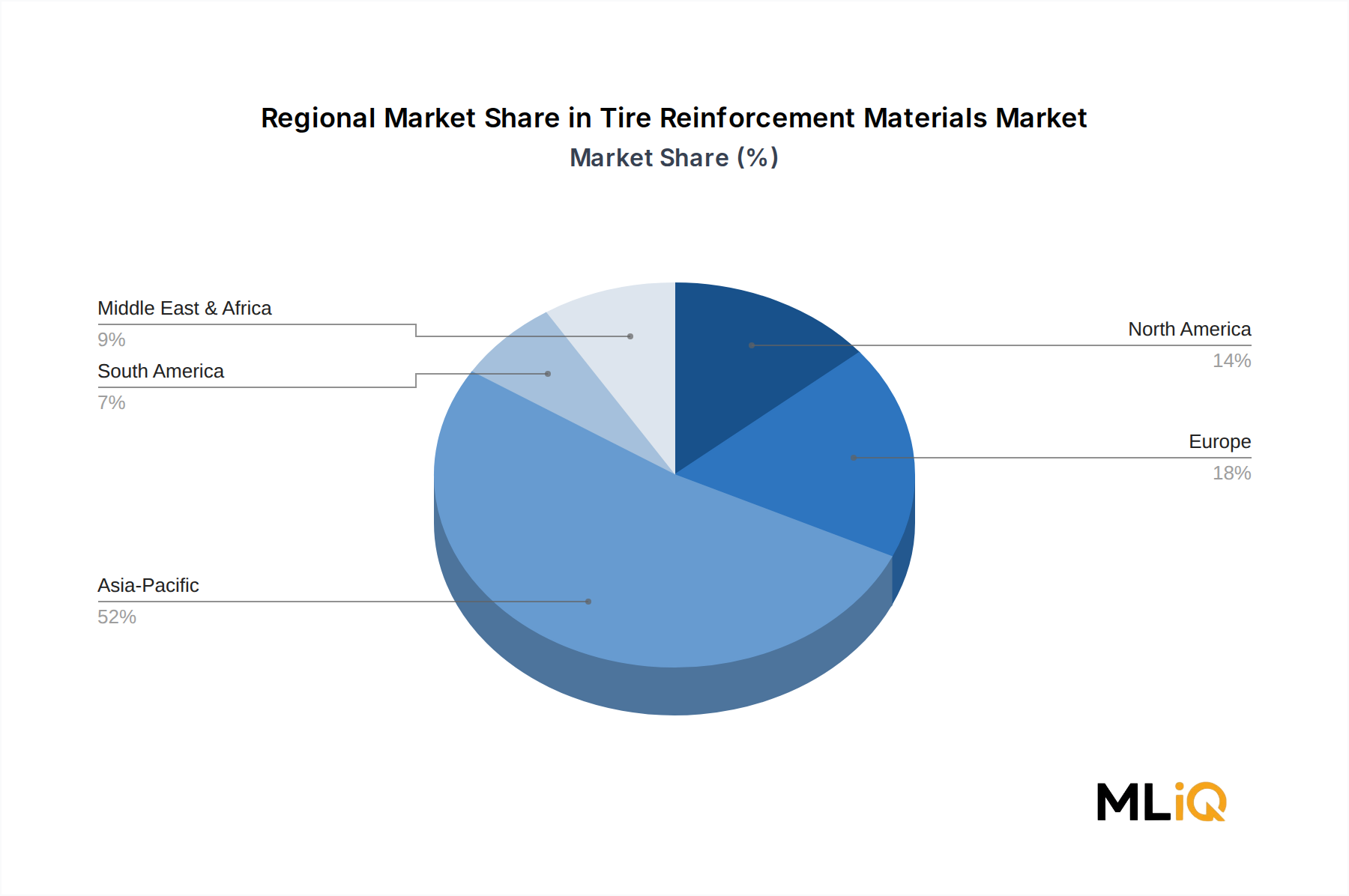

The Tire Reinforcement Materials Market exhibits distinct regional dynamics shaped by tire manufacturing concentration, vehicle fleet demographics, and raw material availability.

Asia Pacific — Dominant Region: Asia Pacific represents the largest regional share of the global Tire Reinforcement Materials Market, accounting for an estimated 55–60% of total market value. China alone is the world's largest tire producer and consumer, housing hundreds of tire manufacturing facilities that collectively consume vast volumes of steel cord, polyester cord fabric, and nylon cord annually. India is the fastest-growing sub-region, with domestic tire demand growing at a CAGR exceeding 6%, driven by rising two-wheeler penetration, commercial vehicle fleet expansion, and government infrastructure investment. Japan and South Korea serve as technology-exporting hubs, home to advanced cord producers such as HYOSUNG, Kolon Industries, TOYOBO CO., LTD., and Teijin Ltd. The ASEAN bloc—particularly Vietnam, Thailand, and Indonesia—is emerging as an important production hub for tire cord fabric, attracting foreign direct investment from Korean and Taiwanese cord fabric producers.

Europe — Mature but Innovation-Intensive: Europe represents approximately 15–18% of global market revenue, characterized by premium tire demand from high-displacement passenger vehicles and stringent EU vehicle safety and labeling regulations. Regional producers such as Bekaert, CORDENKA GmbH & Co. KG, Glanzstoff Industries, and Kordsa's European operations compete on quality, sustainability certifications, and application engineering rather than on price. Growth is modest at a projected CAGR of 2.5–3.0%, but premiumization and EV tire development are sustaining value growth.

North America — Stable Replacement-Driven Demand: North America accounts for roughly 12–14% of market revenue, with demand primarily driven by the large replacement tire market. The United States hosts both domestic tire manufacturers and international OEM plants that source reinforcement materials from global supply chains. CAGR for the region is estimated at 2.8–3.2%.

Middle East & Africa and South America — Emerging Growth Pockets: Both regions are at earlier stages of market development but are exhibiting above-average growth rates of 4.0–5.0% CAGR driven by infrastructure development, vehicle fleet expansion, and rising domestic tire production capacity. Brazil is South America's anchor market, hosting Kordsa and HYOSUNG production operations. Turkey, classified within the Middle East & Africa region in this dataset, is a significant tire cord producer and exporter via Kord

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.89% from 2020-2034 |

| Segmentation |

|

Factors such as Increasing Vehicle Usage Across the Globe; Other Drivers are projected to boost the Tire Reinforcement Materials Market market expansion.

Key companies in the market include Bekaert, Century Enka Limited, CORDENKA GmbH & Co KG, Dupont, FORMOSA TAFFETA CO LTD, Glanzstoff Industries, HYOSUNG, Jiangsu Taiji Industry New Materials Co Ltd, Jiangsu Xingda Steel Tire Cord Co Ltd, Kolon Industries Inc, Kordsa Teknik Tekstil AŞ, Michelin, SRF Limited, Teijin Ltd, Toray Hybrid Cord Inc, TOYOBO CO LTD*List Not Exhaustive.

The market segments include Material, Technology, Type, Application.

The market size is estimated to be USD 17.76 billion as of 2022.

Increasing Vehicle Usage Across the Globe; Other Drivers.

Tire Cord Fabric to Dominate the Market.

Environmental Issues in Manufacturing of Tires; Other Restraints.

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Tire Reinforcement Materials Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Tire Reinforcement Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.