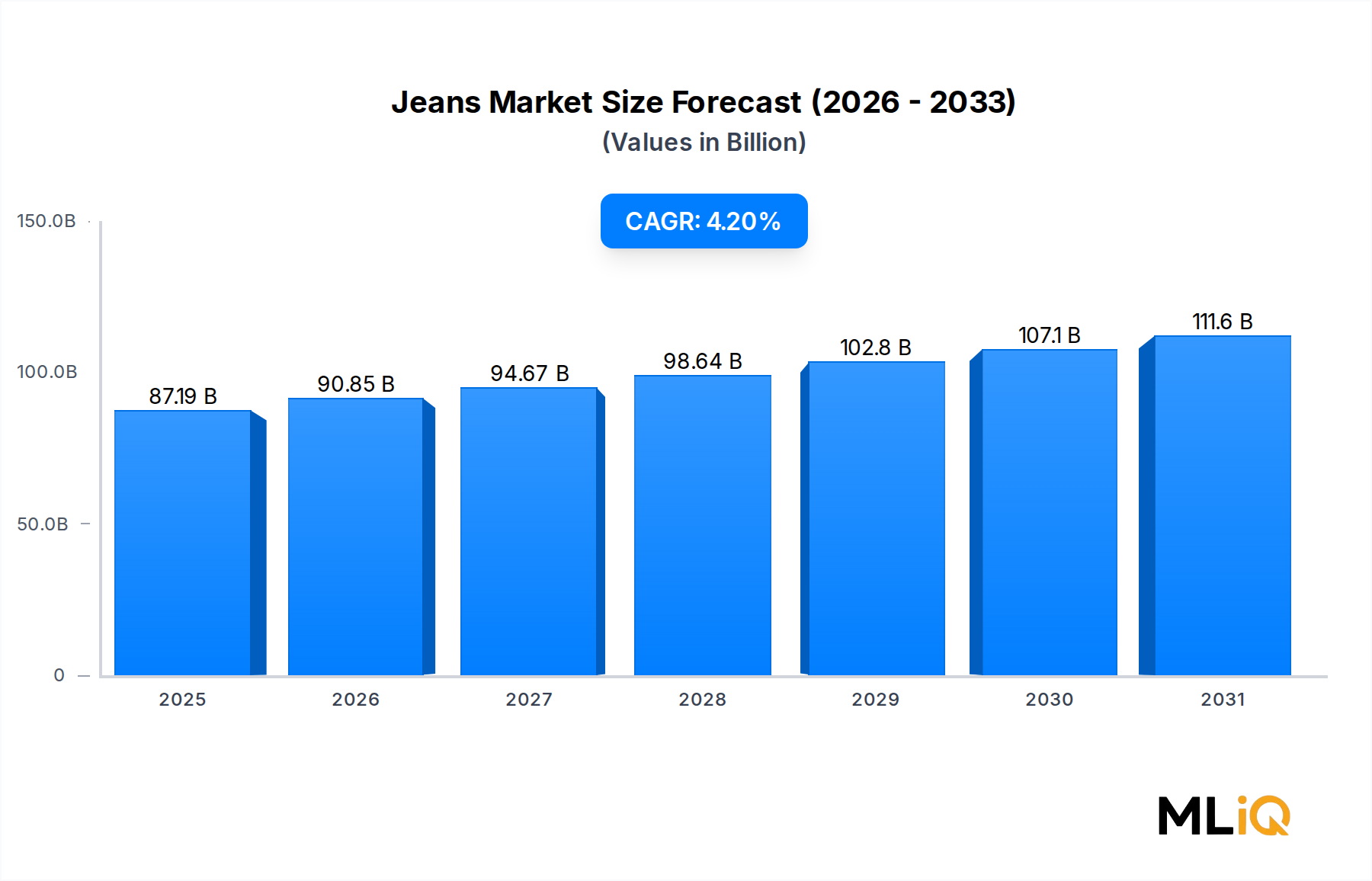

The Jeans Market is propelled by several quantifiable demand drivers while contending with material structural and input-cost constraints that require strategic navigation.

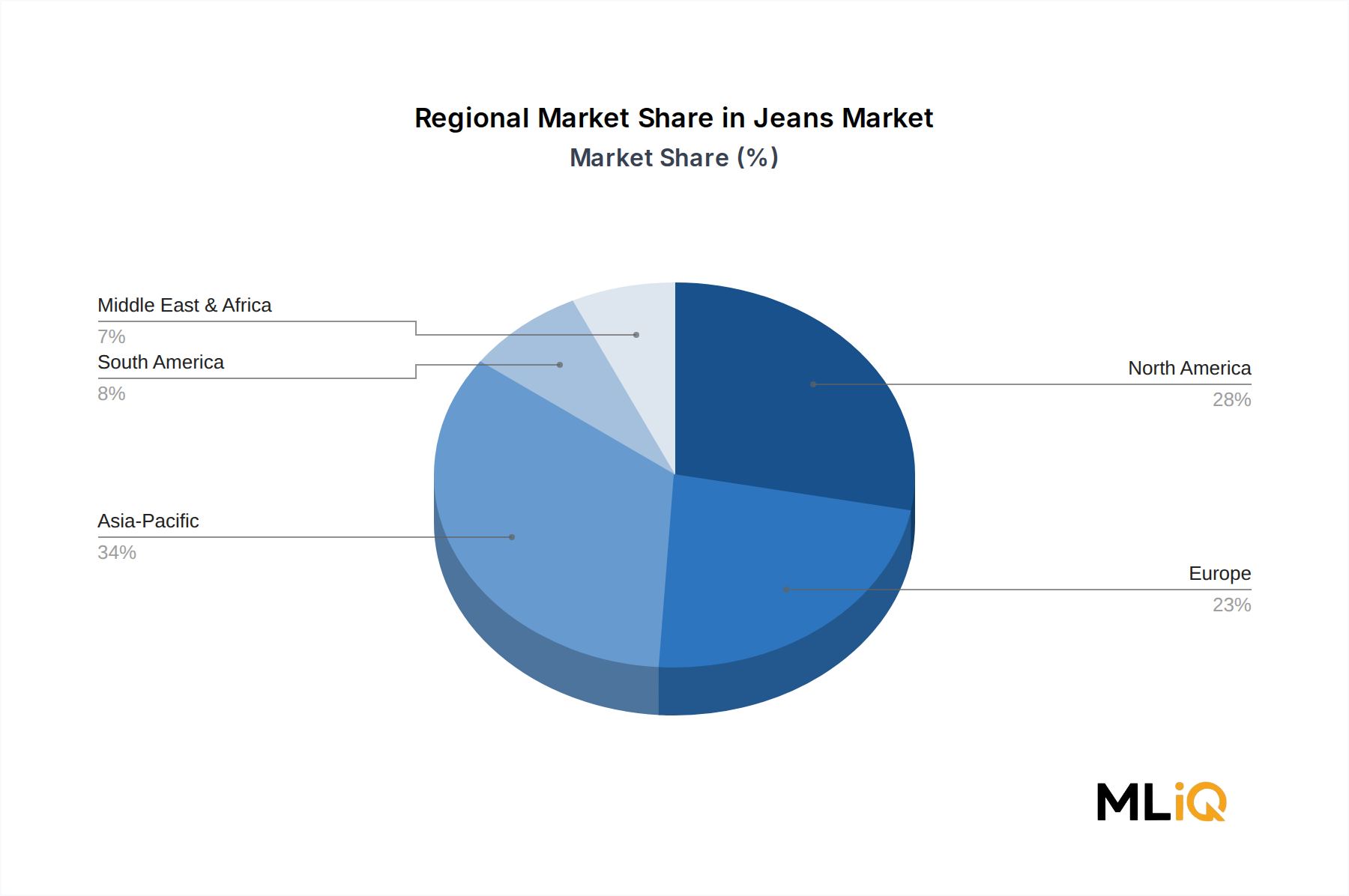

On the demand side, the expansion of the global middle class represents the most durable structural tailwind. According to Brookings Institution estimates, Asia Pacific is expected to account for over 60% of the global middle class by 2030, with China and India contributing the largest incremental consumer cohorts. These demographics exhibit strong brand aspiration and rising denim penetration rates, particularly in urban centers where Western fashion influence is most concentrated.

The shift toward online retail has been transformative. E-commerce now accounts for approximately 30–35% of total apparel sales in developed markets, with denim brands reporting online channel growth rates nearly double those of physical retail. Brands with robust direct-to-consumer digital infrastructure — including Levi Strauss & Co and G-Star RAW — have captured disproportionate share of this channel migration.

Product innovation in performance denim is a secondary but accelerating driver. The integration of elastane, recycled polyester, and moisture-management technologies has expanded denim's functional envelope, drawing consumers from the Athleisure Wear Market who previously prioritized performance fabrics exclusively. This cross-category migration is measurable in unit volume growth for stretch denim SKUs, which have grown at approximately 6–7% annually in the past three years.

On the constraint side, raw material cost inflation is the primary headwind. Cotton prices have exhibited significant volatility, with benchmark futures oscillating between $0.70 and $1.10 per pound in the 2022–2025 period. This volatility directly compresses gross margins for manufacturers without vertically integrated sourcing. Synthetic input costs, including polyester and elastane, have tracked petrochemical price cycles, adding another layer of cost unpredictability.

Labor cost inflation in key manufacturing geographies — Bangladesh, Pakistan, and Vietnam — is eroding the cost arbitrage that historically underpinned fast fashion denim economics. Factory wage increases of 8–15% annually in some geographies are forcing supply chain restructuring decisions.

Consumer attention fragmentation presents a softer but structurally meaningful restraint. With fashion cycle compression driven by social media, inventory obsolescence risk has increased, requiring more agile inventory management and higher markdown provisioning.