1. What are the major growth drivers for the Printing Inks Market market?

Factors such as are projected to boost the Printing Inks Market market expansion.

Printing Inks Market

Printing Inks Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

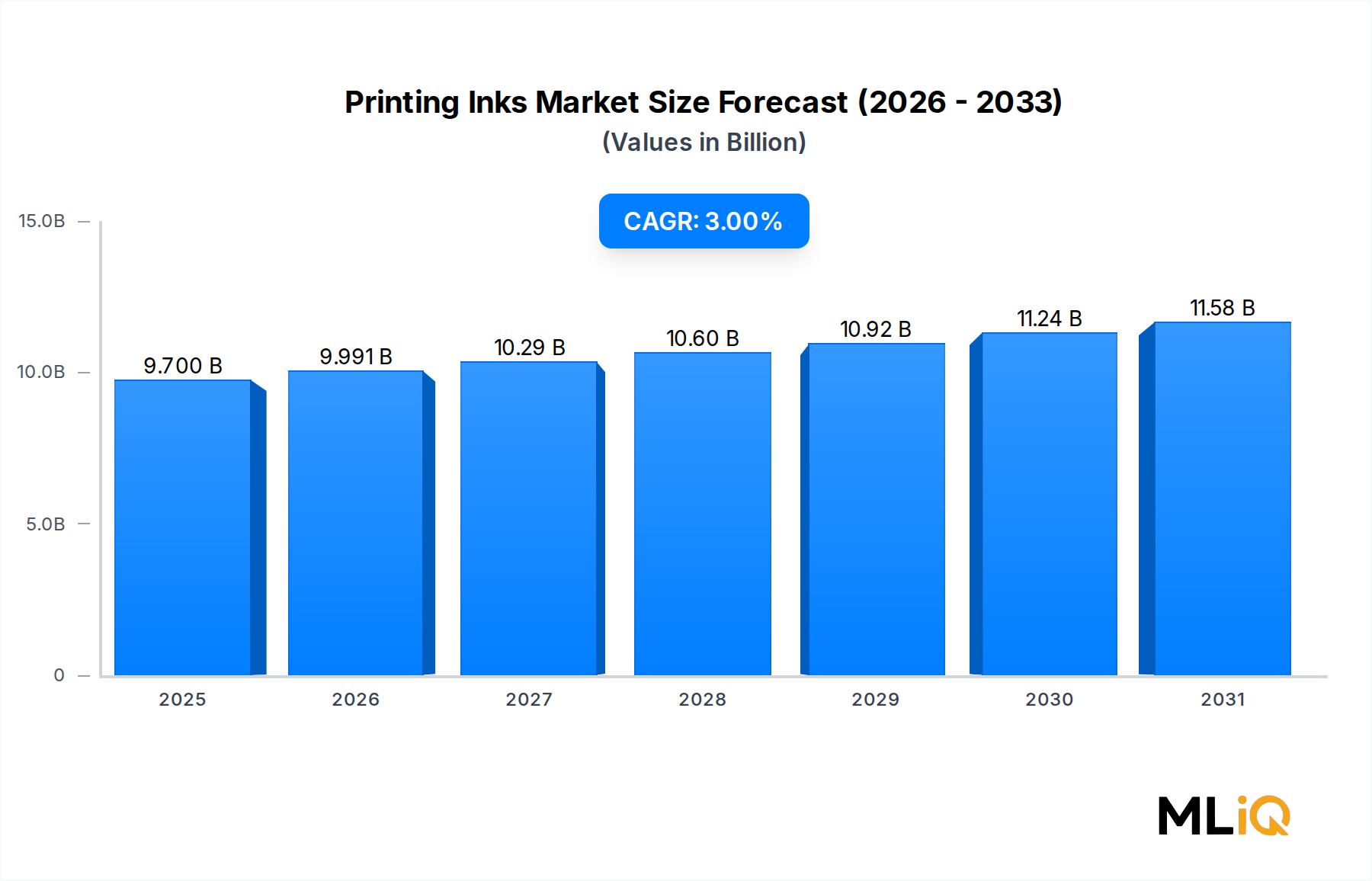

The global Printing Inks Market is valued at $9.7 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 3% through 2033, reflecting steady, sustained demand across packaging, publication, and commercial printing segments. This trajectory places the market on course to surpass $12.3 billion by 2033, underpinned by technological innovation, evolving regulatory frameworks, and shifting end-user priorities.

Several macro tailwinds are reinforcing this growth path. The global rise in e-commerce and consumer goods packaging continues to create persistent demand for high-performance inks capable of meeting both aesthetic and functional specifications. Brand differentiation requirements are pushing brand owners toward premium ink formulations that offer superior color accuracy, faster drying times, and enhanced substrate adhesion. Meanwhile, the proliferation of digital print platforms is reshaping ink consumption patterns, with water-based and UV-cured formulations gaining traction at the expense of traditional solvent-based systems.

Regulatory momentum around volatile organic compound (VOC) emissions is serving as both a driver and a disruptor. Stricter environmental norms across North America and Europe are accelerating the shift toward low-migration, bio-based, and energy-curable ink technologies. This regulatory-driven product substitution is creating incremental revenue opportunities for innovators while compressing margins for incumbents reliant on legacy solvent-based portfolios.

From a demand standpoint, packaging remains the dominant application segment, accounting for the largest share of total ink consumption globally. The surge in flexible packaging for food, pharmaceuticals, and personal care products is a primary catalyst, as brand owners and converters demand inks that comply with food-contact safety regulations without compromising print quality or production throughput.

Asia Pacific leads the market in absolute volume terms, driven by China and India's expanding manufacturing bases and rising domestic consumption. North America and Europe, while more mature, continue to generate strong revenue contributions through premiumization and the adoption of advanced digital and UV-cure ink technologies.

Key demand drivers include expansion in the fast-moving consumer goods (FMCG) sector, growth in pharmaceutical packaging requiring tamper-evident and traceable print solutions, and increasing penetration of digital textile printing. Constraints include raw material price volatility, particularly for pigments, resins, and specialty solvents, as well as margin pressure from consolidation among large printing conglomerates.

Looking ahead, the market's forward-looking outlook is constructive. Investment in sustainable ink chemistry, coupled with the digitization of commercial printing workflows, is expected to sustain above-GDP growth rates across multiple sub-segments. Companies with diversified portfolios spanning water-based, UV-cured, and digital ink platforms are best positioned to capture disproportionate share in the coming cycle.

The packaging application segment represents the single largest revenue-generating category within the Printing Inks Market, commanding an estimated 55–60% of total global market value in 2025. This dominance is structural rather than cyclical, rooted in the indispensable role of printed packaging across virtually every consumer-facing industry vertical, from food and beverage to pharmaceuticals, personal care, and household chemicals.

The primacy of packaging as an end-use driver stems from several reinforcing dynamics. First, the global transition from rigid to flexible packaging formats has intensified ink consumption per unit of substrate, as flexible materials such as polyethylene, polypropylene, and polyester films require specialized ink chemistries with specific adhesion, flexibility, and barrier properties. Flexographic and gravure printing processes dominate the flexible packaging segment, each demanding distinct ink viscosity profiles and solvent systems.

Second, food safety regulation has elevated the technical bar for packaging inks. Directives such as the Swiss Ordinance and the EU Regulation No. 10/2011 impose strict limits on low-molecular-weight substances that can migrate from packaging into food contact materials. This regulatory environment has accelerated demand for low-migration UV-cured and water-based ink formulations, often at a premium price point, benefiting suppliers with robust regulatory affairs capabilities.

Third, the shift toward shorter print runs and more frequent packaging redesigns — driven by SKU proliferation and regional market customization — is increasing the per-unit cost tolerance for high-quality inks, as packaging converters prioritize color consistency and press uptime over unit ink cost.

Within the packaging segment, flexographic printing holds a particularly strong position for mid-to-high volume runs on flexible substrates and corrugated board. The Flexographic Inks Market has seen significant investment in water-based and UV-flexo formulations, with suppliers developing low-viscosity, fast-drying systems compatible with high-speed press configurations running at speeds exceeding 500 meters per minute.

Gravure inks remain critical for long-run, high-fidelity packaging applications such as confectionery wrappers, snack bags, and pharmaceutical blister packs, where consistent color density and fine detail reproduction are non-negotiable. Meanwhile, the Digital Inks Market is making measured inroads in packaging through inkjet-based systems for short runs, versioning, and personalized packaging, particularly in luxury goods and pharmaceutical serialization.

Key players capturing share within the packaging ink sub-segment include Sun Chemical Corporation, Flint Group, Sakata INX Corporation, and Huber Group. Sun Chemical, in particular, has invested heavily in low-migration packaging ink platforms and launched dedicated product lines compliant with major food-contact regulatory frameworks. Flint Group has pursued a strategy of geographic expansion paired with formulation innovation, targeting growth markets in Asia Pacific and Latin America.

The packaging segment's share is not merely holding steady — it is consolidating further. As e-commerce logistics demand more robust corrugated board printing and as pharmaceutical track-and-trace mandates expand globally, the structural tailwinds underpinning packaging's dominance are expected to intensify through 2033. This makes the packaging application the most critical growth engine for ink manufacturers seeking to defend or expand market position.

The Printing Inks Market is shaped by a constellation of demand drivers and structural constraints that collectively define its 3% CAGR trajectory through 2033.

Driver 1: Packaging Volume Growth. Global flexible packaging demand is projected to grow at approximately 4–5% annually through the forecast period, directly translating into increased ink consumption. The food and beverage sector alone accounts for over 40% of flexible packaging end-use, creating a persistent and recession-resistant baseload of demand for packaging inks.

Driver 2: Regulatory-Driven Product Premiumization. VOC emission regulations in the European Union and North American EPA frameworks are mandating the phase-out of high-solvent ink formulations across multiple application categories. This substitution dynamic is generating incremental revenue for water-based and UV-cured ink suppliers, whose products command a 15–25% price premium over conventional solvent-based equivalents. The UV-Cured Inks Market, in particular, is benefiting from this regulatory tailwind across both packaging and commercial print segments.

Driver 3: Digital Printing Adoption. The commercial printing sector's migration toward digital workflows is expanding the addressable market for digital ink formulations. Inkjet ink consumption in commercial and industrial applications is growing at approximately 6–8% annually, outpacing the broader market's CAGR.

Driver 4: Pharmaceutical Packaging Expansion. Global pharmaceutical packaging expenditure is rising on the back of aging populations, biologic drug proliferation, and serialization mandates. This is creating demand for specialty inks with anti-counterfeiting, tamper-evidence, and machine-readable properties.

Constraint 1: Raw Material Price Volatility. Key ink inputs — including organic pigments, hydrocarbon resins, and specialty solvents — are subject to significant price swings tied to petrochemical feedstock markets. Titanium dioxide and phthalocyanine pigment costs have experienced 10–20% intra-year price fluctuations in recent years, compressing ink manufacturer margins and complicating long-term contract pricing.

Constraint 2: Print Volume Decline in Publication. The secular decline in newspaper and magazine circulation has reduced lithographic ink consumption for publication end-uses by an estimated 3–4% annually. This structural headwind offsets volume gains in packaging and digital segments at the aggregate market level.

Constraint 3: Consolidation Among Print Buyers. Ongoing consolidation among large commercial printing groups and packaging converters is increasing buyer bargaining power, putting downward pressure on ink pricing and squeezing supplier margins.

The Printing Inks Market is moderately consolidated, with a small number of multinational ink manufacturers controlling a significant share of global revenue alongside a fragmented tier of regional and specialty suppliers. The following profiles capture the competitive positioning of leading participants:

Sun Chemical Corporation: One of the world's largest producers of printing inks and pigments, Sun Chemical operates across all major ink technologies including offset, flexographic, gravure, and digital. Its low-migration packaging ink platform and investments in sustainable chemistry position it as a regulatory compliance leader.

Flint Group: A globally diversified ink and printing consumables manufacturer, Flint Group serves packaging, publication, and commercial print markets. The company has pursued aggressive geographic expansion into Asia Pacific and Latin America while investing in water-based and UV-flexo formulations.

Sakata INX Corporation: A Japanese-headquartered multinational with a strong presence in Asia Pacific, Sakata INX is known for its high-performance gravure and flexographic inks for flexible packaging. The company has expanded production capacity in India and Southeast Asia to serve growing regional demand.

Huber Group: A European specialist with deep expertise in offset and packaging inks, Huber Group has differentiated through its renewable raw material programs and bio-based ink initiatives, targeting customers with strong ESG procurement criteria.

TOYO Ink Group: A major Japanese ink manufacturer with global operations, TOYO Ink is active across packaging, industrial, and digital ink segments. The group has made strategic acquisitions to expand its specialty ink capabilities in North America and Europe.

ALTANA AG: Operating through its ECKART and BYK subsidiaries, ALTANA AG supplies specialty effect pigments, additives, and coating materials used extensively in high-value printing applications. Its focus on innovation and premium performance differentiates it in the specialty segment.

Wikoff Color Corporation: A North American ink manufacturer focused on the packaging and publication sectors, Wikoff Color is known for its custom color matching capabilities and responsive technical service model serving regional converters.

T&K TOKA Corporation: A Japanese ink manufacturer specializing in offset and UV inks, T&K TOKA has a strong domestic base and is expanding its sustainable ink product lines in response to regulatory and customer sustainability requirements.

Zeller+Gmelin GmbH & Co. KG: A German specialty ink manufacturer with a reputation for high-quality sheet-fed offset and publication inks, Zeller+Gmelin serves European printing houses and has developed a dedicated portfolio of mineral oil-free and vegetable oil-based formulations.

January 2025: Sun Chemical Corporation announced the commercial launch of its SunLam lamination ink series, specifically engineered for solvent-free flexible packaging applications compliant with EU food contact migration limits.

March 2025: Flint Group unveiled a new water-based flexographic ink platform targeting the corrugated board segment, designed to deliver high-opacity print quality at press speeds exceeding 400 meters per minute, reducing drying energy consumption by an estimated 20%.

May 2025: Sakata INX Corporation broke ground on a new ink manufacturing facility in Pune, India, with an annual production capacity of 15,000 metric tons, targeting the fast-growing South Asian packaging market.

July 2025: Huber Group published its inaugural Sustainability Report detailing progress toward a 50% reduction in carbon emissions intensity by 2030, anchored by its bio-based offset ink line manufactured using renewable plant-derived feedstocks.

September 2025: ALTANA AG completed the acquisition of a specialty effect pigment producer in Germany, expanding its portfolio of metallic and pearlescent pigment solutions for premium packaging and security printing applications.

November 2025: The European Printing Ink Association (EuPIA) released updated guidelines on mineral oil aromatic hydrocarbons (MOAH) restrictions in food-contact packaging inks, prompting multiple ink manufacturers to accelerate reformulation programs ahead of anticipated legislative deadlines.

February 2026: TOYO Ink Group announced a joint development agreement with a leading digital press manufacturer to co-develop high-speed inkjet inks optimized for single-pass production systems targeting the corrugated packaging segment.

The Printing Inks Market exhibits meaningful regional variation in growth rates, market maturity, and demand drivers, reflecting differences in manufacturing activity, regulatory environments, and consumer market development.

Asia Pacific: The dominant regional market by volume and the fastest-growing by value, Asia Pacific accounts for an estimated 40–45% of global ink consumption in 2025. China is the single largest national market, driven by its massive packaging manufacturing base, export-oriented production, and rapidly expanding domestic consumer goods sector. India is the fastest-growing major economy within the region, with packaging ink demand expanding at approximately 6–7% annually on the back of FMCG sector growth and pharmaceutical manufacturing expansion. Japan and South Korea remain technology-intensive markets with strong demand for high-performance and specialty inks.

North America: A mature but innovation-active market, North America generates approximately 22–25% of global revenue. The United States dominates the regional landscape, with demand weighted toward packaging and digital commercial print applications. The transition to sustainable ink formulations is particularly advanced in North America, driven by retailer sustainability mandates and EPA regulatory pressure. Regional CAGR is estimated at 2.5–3% through 2033.

Europe: Europe accounts for approximately 20–23% of global market value and is characterized by stringent regulatory oversight, high sustainability standards, and a mature printing industry. Germany, the United Kingdom, France, and Italy are the largest national markets. The EU's emphasis on circular economy principles and chemical safety is accelerating the adoption of water-based, UV-cured, and mineral oil-free ink systems. Regional CAGR is estimated at 2–2.5%, reflecting both regulatory-driven premiumization and structural volume headwinds in publication printing.

Middle East & Africa: A smaller but incrementally growing market, the region benefits from expanding packaging industries in the GCC and South Africa, as well as rising consumer goods penetration. Regional CAGR is estimated at 4–5%, though from a low absolute base.

South America: Brazil and Argentina anchor South American demand, with the packaging sector serving as the primary growth engine. Economic volatility creates demand uncertainty, but structural growth in food processing and pharmaceutical packaging supports a regional CAGR of approximately 3–4%.

The Printing Inks Market serves a diverse end-user base spanning packaging converters, commercial printers, publication printers, and specialty industrial print operators. Each segment exhibits distinct purchasing criteria, price sensitivities, and procurement channel preferences.

Packaging converters constitute the largest and most strategically important customer segment. These buyers prioritize technical performance — including color gamut, adhesion, lamination bond strength, and regulatory compliance — over unit cost alone. Procurement decisions are frequently influenced by brand owner specifications, as large FMCG and pharmaceutical companies mandate approved supplier lists and specific ink performance parameters. Price sensitivity is moderate to low for specialty and compliant formulations, but competitive bidding is common for commodity ink volumes. Procurement channels are predominantly direct supplier relationships with preferred ink manufacturers, supplemented by distributor networks for spot volumes.

Commercial printers represent the second-largest customer segment, covering sheet-fed offset, digital, and wide-format applications. These buyers are more price-sensitive than packaging converters, as they operate in a highly competitive, margin-pressured printing services market. Purchasing decisions increasingly reflect total cost of ownership considerations — including ink yield, press uptime, and color consistency — rather than list price alone. The shift toward digital printing platforms is altering procurement behavior, with buyers placing smaller, more frequent orders for digital

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Printing Inks Market market expansion.

Key companies in the market include Wikoff Color Corporation, T&K TOKA Corporation, Flint Group, Sakata INX Corporation, Huber Group, Sun Chemical Corporation, Zeller+Gmelin GmbH & Co. KG, ALTANA AG, and TOYO Ink Group..

The market segments include Printing Process, Application, Product Type.

The market size is estimated to be USD 9.7 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Printing Inks Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Printing Inks Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.