1. What are the major growth drivers for the Polysorbate Market market?

Factors such as are projected to boost the Polysorbate Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

Polysorbate Market

Polysorbate Market

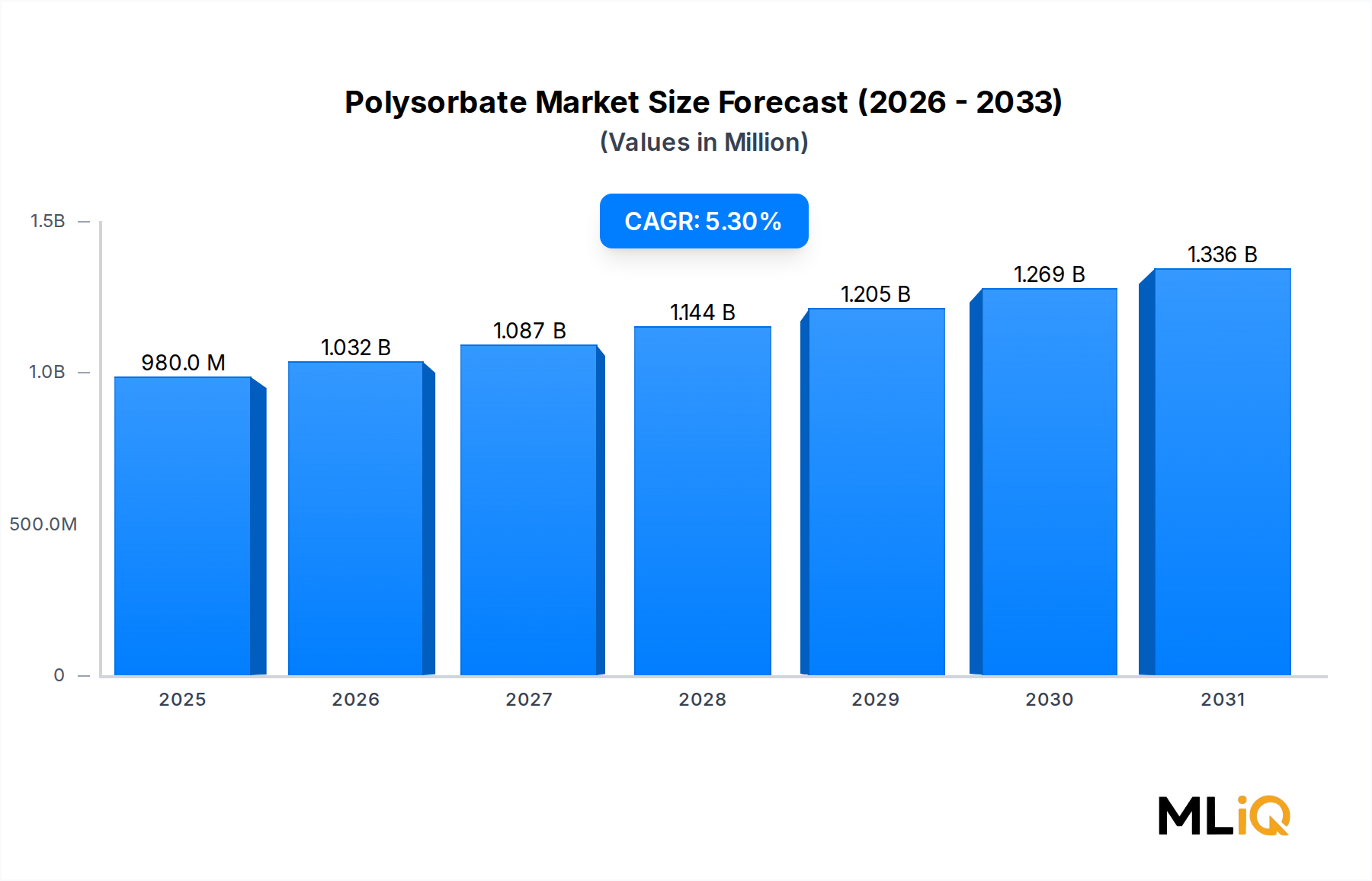

The global Polysorbate Market is valued at $0.98 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 5.3% through 2025–2033, reflecting sustained and diversified demand across pharmaceuticals, food processing, and personal care manufacturing. This trajectory positions the market to surpass $1.5 billion by 2033, underpinned by a confluence of regulatory approvals, formulation science advancements, and expanding emerging-market consumption.

Polysorbates — nonionic surfactants and emulsifiers derived primarily from polyethoxylated sorbitan esterified with fatty acids — occupy a critical functional role across multiple industries. Their amphiphilic molecular architecture enables oil-in-water emulsification, solubilization, wetting, and dispersion across a wide pH and temperature range, making them essentially irreplaceable in numerous commercial formulations. The four dominant commercial grades — Polysorbate 20, 40, 60, and 80 — each serve differentiated application niches, ensuring the market benefits from diversified demand channels rather than concentration risk in a single segment.

Key demand drivers include the global pharmaceutical industry's accelerating biologics and vaccine pipeline, where Polysorbate 80 serves as a critical stabilizer in parenteral formulations. The post-pandemic surge in vaccine manufacturing capacity has created a structural uplift in polysorbate procurement contracts globally. Simultaneously, the processed food industry's ongoing requirement for clean-label-compatible emulsification solutions continues to drive Polysorbate 60 and 20 consumption in baked goods, dairy alternatives, and confectionery.

Macro tailwinds reinforcing this growth include rising per capita incomes in Asia Pacific economies (particularly China and India), which are accelerating the consumption of packaged foods and premium personal care products — both of which are heavy polysorbate consumers. Additionally, the global biosimilars market expansion is indirectly amplifying polysorbate demand, as biosimilar formulators require GMP-grade Polysorbate 80 in quantities comparable to reference biologics.

From a supply-side perspective, the market benefits from a relatively established global manufacturing base, with major chemical conglomerates investing in capacity expansions and quality certifications to serve pharmaceutical-grade demand. However, supply chain vulnerabilities related to ethylene oxide and fatty acid feedstocks introduce moderate pricing volatility.

Looking ahead to 2033, the Polysorbate Market is expected to increasingly bifurcate between commodity-grade applications (food and industrial) and high-purity pharmaceutical-grade segments commanding premium pricing. Investments in bio-based and synthetic production routes, coupled with tightening regulatory standards for elemental impurities and particle contamination, will reshape competitive dynamics and create barriers to entry for lower-tier producers.

Among all grades and application segments, pharmaceutical-grade Polysorbate 80 stands as the single largest revenue-generating sub-segment within the Polysorbate Market. Its dominance stems from structural factors rooted in formulation science, regulatory precedent, and the explosive growth of biologic drug manufacturing worldwide.

Polysorbate 80 (also designated Tween 80) is characterized by oleic acid esterification at the sorbitan moiety, yielding a hydrophilic-lipophilic balance (HLB) of approximately 15, which is ideally suited for oil-in-water emulsification and protein stabilization in aqueous parenteral formulations. Its ability to inhibit protein aggregation, prevent surface adsorption of therapeutic proteins to container closures, and maintain drug potency under freeze-thaw stress cycles makes it the emulsifier of choice for monoclonal antibodies (mAbs), biosimilars, vaccines, and recombinant protein formulations.

The global biologics market — which exceeded $400 billion in 2024 and is growing at a CAGR exceeding 8% — directly feeds pharmaceutical polysorbate demand. Every approved mAb formulation assessed by the FDA and EMA in the past decade has incorporated polysorbate (predominantly PS80) as a stabilizing excipient. This regulatory precedent creates significant switching inertia: formulators are reluctant to alter excipient selection mid-development due to the extensive stability and comparability testing required by regulatory authorities.

The COVID-19 vaccine manufacturing wave of 2021–2023 demonstrated the acute scalability of polysorbate demand. Lipid nanoparticle (LNP)-based mRNA vaccines, including those developed by Moderna and BioNTech/Pfizer, incorporated polysorbate 80 in their formulations, triggering a significant demand spike that temporarily outpaced global production capacity. This episode has prompted leading pharmaceutical companies to establish long-term supply agreements with polysorbate producers, institutionalizing demand stability.

Key players competing for pharmaceutical-grade PS80 supply contracts include BASF SE, Croda International plc, Evonik Industries AG, and Merck KGaA — all of whom maintain dedicated GMP-compliant production lines with extensive certificates of analysis, pharmacopeial compliance (USP, EP, JP), and established drug master file (DMF) portfolios with major regulatory agencies. Croda International plc, in particular, has positioned its Excipients division as a premium supplier, emphasizing ultra-low peroxide specifications and reduced 1,4-dioxane content to address evolving safety concerns highlighted in recent FDA draft guidances.

Lanxess and Evonik Industries AG have similarly invested in expanding pharmaceutical excipient production, recognizing the higher-margin profile relative to food or industrial-grade polysorbate. Evonik's TEGO brand polysorbate line is widely referenced in pharmaceutical development documentation globally.

The pharmaceutical segment's share within the total Polysorbate Market is estimated to be consolidating rather than merely growing — meaning that the pharmaceutical end-use is capturing an increasing proportion of total polysorbate revenues even as absolute volumes in food and cosmetics also expand. This is driven by the significant price premium commanded by pharmaceutical-grade material (typically 3–5x the cost of food-grade equivalents) due to stricter specification requirements, batch traceability, and regulatory documentation burdens.

Future growth in this segment will be driven by the global biosimilars pipeline, estimated to include over 300 candidates in advanced clinical stages as of 2024, each of which will require validated polysorbate supply chains upon commercialization.

Several precisely quantifiable forces are currently shaping the growth profile and competitive dynamics of the Polysorbate Market.

Driver 1 — Biologics and Vaccine Manufacturing Expansion: The global biologics market surpassed $400 billion in 2024, with mAbs constituting roughly 50% of biologics revenues. Since virtually all parenteral biologic formulations incorporate Polysorbate 80 as a stabilizer — typically at concentrations of 0.01%–0.1% w/v — every incremental biologic approval directly translates into sustained polysorbate procurement. The FDA approved 55 novel drugs in 2023, a significant proportion of which were biologics requiring polysorbate in their registered formulations.

Driver 2 — Food Processing Industry Expansion: Global processed food revenues are projected to grow from approximately $3.8 trillion in 2024 to over $5.2 trillion by 2033. Polysorbate 60 and 20 are extensively used in baked goods, dairy emulsification, and confectionery stabilization. Regulatory approvals such as GRAS status in the United States and E-number designations in the EU (E432–E436) provide strong market access assurance.

Driver 3 — Personal Care Premiumization: Rising middle-class expenditure in Asia Pacific is fueling premium skincare and haircare product demand. Polysorbate 20, widely used as a solubilizer in toners, facial cleansers, and fragrance formulations, is benefiting from this trend. The Asia Pacific personal care market alone is projected to grow at a CAGR of 7.1% through 2030.

Constraint 1 — Polysorbate Degradation and Safety Scrutiny: Studies published between 2020 and 2024 identified polysorbate degradation products (including fatty acid peroxides and oxidation byproducts) as potential triggers of hypersensitivity reactions in biologic drug recipients. The FDA issued a draft guidance in 2023 recommending tighter specification controls on polysorbate 80 peroxide content, introducing additional compliance costs for suppliers.

Constraint 2 — Feedstock Price Volatility: Polysorbate production depends on ethylene oxide and fatty acid feedstocks (particularly oleic acid and lauric acid). Ethylene oxide prices exhibited 20–30% volatility in 2022–2023 due to petrochemical market disruptions, directly compressing polysorbate producer margins and introducing pricing instability in downstream supply contracts.

The Polysorbate Market features a moderately consolidated competitive landscape dominated by multinational specialty chemical corporations alongside a competitive fringe of regional producers, particularly in Asia.

BASF SE: One of the world's largest chemical companies, BASF produces polysorbates under its portfolio of emulsifiers and surfactants, serving food, pharmaceutical, and personal care applications with GMP-compliant and food-grade product lines backed by extensive global regulatory documentation.

Croda International plc: A premium specialty chemical supplier with a dedicated pharmaceutical excipients division, Croda competes on ultra-low impurity polysorbate 80 specifications and maintains drug master files across major regulatory jurisdictions, positioning the company as a preferred supplier for biologic drug manufacturers.

EVONIK INDUSTRIES AG: Operates the TEGO brand polysorbate product line, supplying pharmaceutical, food, and cosmetics markets; Evonik leverages its integrated surfactant manufacturing capabilities and R&D investment in excipient innovation to maintain a strong position in high-specification markets.

Lanxess: A diversified specialty chemical company with a materials and additives portfolio that includes polysorbate emulsifiers targeting food and industrial applications; Lanxess focuses on cost-competitive production and broad geographic distribution capabilities.

Merck KGaA: A global life science and specialty chemical company supplying laboratory and manufacturing-scale polysorbate under its MilliporeSigma brand, primarily targeting pharmaceutical process development and quality control applications.

Otto Chemie Pvt. Ltd.: An Indian specialty chemical distributor and manufacturer supplying polysorbate grades to domestic and export markets, competing primarily on price competitiveness and regional supply chain responsiveness.

TCI America: A fine chemical supplier offering research-grade polysorbate products for laboratory and small-scale pharmaceutical development applications, competing in the specialty reagent segment.

Mohini Organics Pvt. Ltd.: An Indian manufacturer of surfactants and emulsifiers, including polysorbate grades, serving domestic food processing and personal care sectors with regionally competitive pricing.

VENUS ETHOXYETHERS PVT.LTD.: An Indian producer specializing in ethoxylated products including polysorbates, serving regional markets across South Asia and the Middle East.

Estelle Chemicals Pvt. Ltd.: A Mumbai-based specialty chemical company producing polysorbate emulsifiers for food, pharmaceutical, and industrial applications.

Niram Chemicals: A regional Indian supplier of polysorbate and related emulsifier products serving domestic food and personal care industries.

Matangi Industries: An Indian specialty chemical manufacturer offering polysorbate products targeting the domestic food processing and agrochemical markets.

Alfa Aesar: A Thermo Fisher Scientific company supplying high-purity polysorbate reagents for research and pharmaceutical process chemistry applications.

Guangdong Huana Chemistry Co., Ltd.: A Chinese manufacturer of polysorbate and related emulsifiers, competing aggressively on pricing in Asia Pacific and export markets.

Aceto Corp.: A US-based specialty chemical distribution and supply company with polysorbate in its pharmaceutical raw materials portfolio.

January 2023: The US Food and Drug Administration published a draft guidance document recommending updated specification limits for polysorbate 80 peroxide content in parenteral drug formulations, prompting major suppliers including Croda and Evonik to accelerate development of low-oxidation polysorbate variants.

March 2023: BASF SE announced expanded production capacity for pharmaceutical-grade emulsifiers at its European manufacturing sites, partially driven by sustained post-pandemic biologic drug manufacturing demand and long-term supply agreement commitments with major vaccine producers.

June 2023: Croda International plc received updated drug master file (DMF) acceptance from the FDA for its next-generation low-peroxide Polysorbate 80 product, enabling pharmaceutical customers to reference the new specification in regulatory submissions without additional testing burden.

October 2023: The European Food Safety Authority (EFSA) completed a re-evaluation of polysorbate emulsifiers (E432–E436), reconfirming their safety at approved use levels in food applications and providing regulatory continuity for European food manufacturers.

February 2024: Guangdong Huana Chemistry Co., Ltd. announced capacity expansion at its Guangdong facility, targeting increased polysorbate output to serve growing demand in Southeast Asian food processing and personal care markets.

April 2024: Evonik Industries AG published research findings on polysorbate 80 stabilization mechanisms in mRNA lipid nanoparticle formulations, reinforcing the technical case for continued PS80 adoption in next-generation vaccine and gene therapy delivery systems.

November 2024: Industry consortium discussions under the International Pharmaceutical Excipients Council (IPEC) advanced a framework for harmonized global polysorbate quality specifications, aimed at reducing supplier audit duplication and streamlining pharmaceutical supply chain qualification.

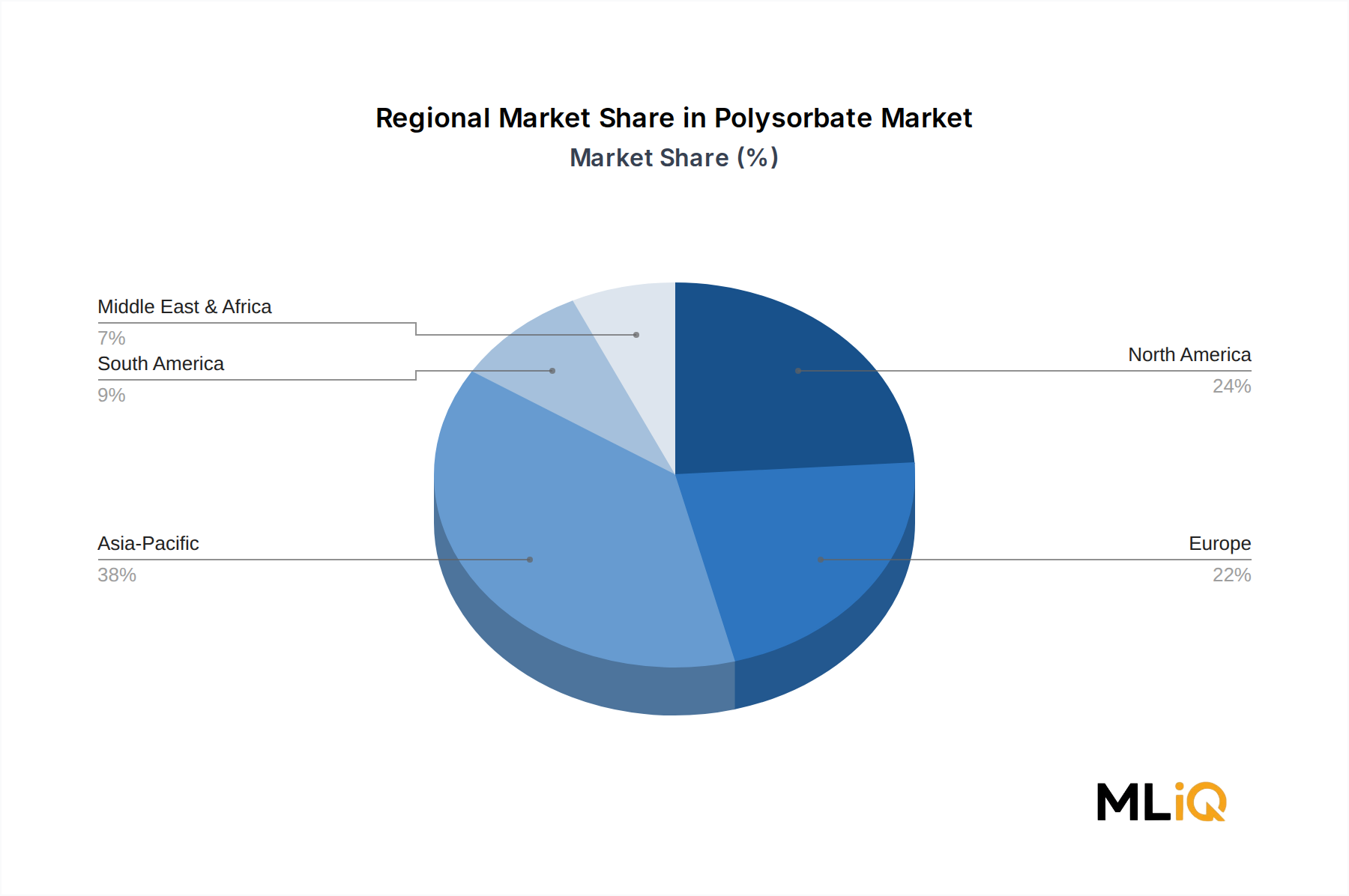

The Polysorbate Market exhibits distinct regional demand patterns driven by local industry structures, regulatory environments, and economic development trajectories.

Asia Pacific — Fastest-Growing Region: Asia Pacific represents the fastest-growing regional market, with a projected CAGR of approximately 6.8% through 2033. China and India are the primary growth engines. China's domestic pharmaceutical manufacturing expansion — driven by biosimilar development and domestic vaccine production — is generating substantial polysorbate 80 demand. India's growing processed food sector and rapidly expanding cosmetics industry are fueling polysorbate 20 and 60 consumption. The ASEAN region contributes incremental demand from expanding food manufacturing and personal care sectors. China also hosts a significant production base, with manufacturers such as Guangdong Huana Chemistry Co., Ltd. serving both domestic demand and cost-sensitive export markets.

North America — Mature, Premium-Oriented Market: North America accounts for an estimated 28–30% of global polysorbate revenues, with the United States as the dominant contributor. The region's demand profile skews heavily toward pharmaceutical-grade polysorbate 80, driven by the concentration of biologic drug manufacturers and contract development and manufacturing organizations (CDMOs). The mature food processing industry maintains stable but slower-growth polysorbate consumption. The United States market is characterized by stringent FDA specifications, creating quality barriers that favor established global suppliers over low-cost regional producers. CAGR for the North America region is estimated at 4.1% through 2033.

Europe — Regulatory Stringency Driving Premium Demand: Europe represents approximately 25% of global revenues, with Germany, France, and the United Kingdom as key markets. The European pharmaceutical industry's commitment to biologic drug development and biosimilar manufacturing (supported by EMA biosimilar pathway clarity) sustains pharmaceutical-grade polysorbate demand. EFSA's ongoing re-evaluation process provides regulatory stability for food-grade applications. European CAGR is estimated at 4.5% through 2033, reflecting stable industrial demand and modest food sector growth.

Middle East & Africa — Emerging Consumption Growth: This region represents a smaller but accelerating

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Factors such as are projected to boost the Polysorbate Market market expansion.

Key companies in the market include Otto Chemie Pvt. Ltd., TCI America, Mohini Organics Pvt. Ltd., VENUS ETHOXYETHERS PVT.LTD., Estelle Chemicals Pvt. Ltd., Lanxess, EVONIK INDUSTRIES AG, Croda International plc, Niram Chemicals, Matangi Industries, Alfa Aesar, BASF SE, Merck KGaA, Guangdong Huana Chemistry Co., Ltd., Aceto Corp..

The market segments include Source, Grade, End-use.

The market size is estimated to be USD 0.98 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Polysorbate Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Polysorbate Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.