Public Cloud Segment Dominance in the Finance Cloud Market

Among the three deployment models available within the Finance Cloud Market — public cloud, private cloud, and hybrid cloud — the public cloud segment commands the largest revenue share, accounting for the plurality of total market spend. This dominance is rooted in the segment's unmatched scalability economics, broad global availability zone coverage, and the maturation of financial-grade security controls offered by hyperscale cloud providers.

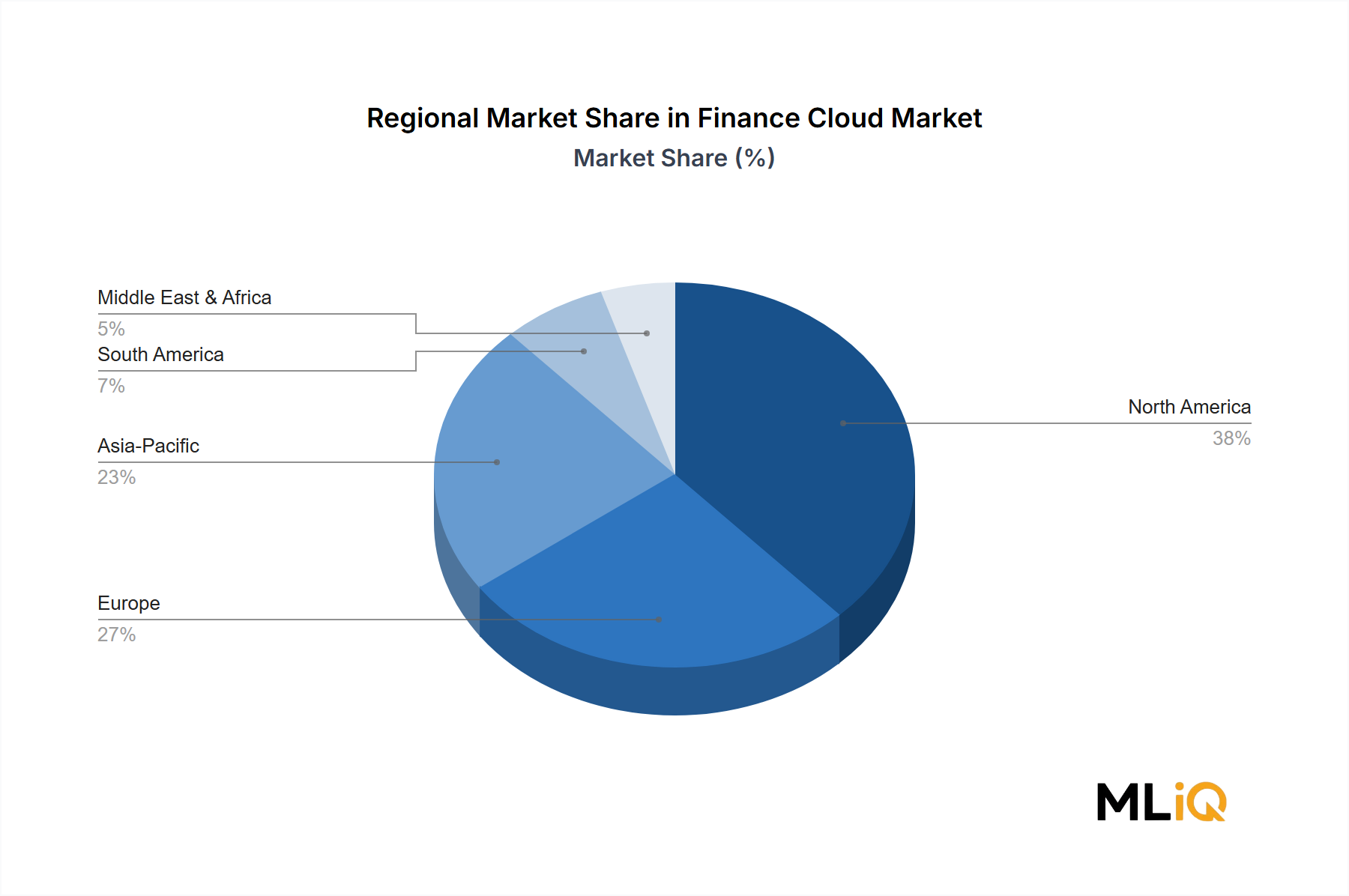

Public cloud deployments have historically been viewed with skepticism by financial institutions due to data sovereignty concerns, multi-tenancy risks, and regulatory uncertainty. However, the landscape has shifted materially over the past five years. Major regulators in North America, Europe, and Asia Pacific have published formal cloud guidance frameworks that legitimize public cloud adoption for workloads previously confined to on-premise infrastructure. This regulatory clarity has been a pivotal catalyst, enabling chief information officers and chief risk officers at tier-one banks to approve large-scale migrations to public cloud environments.

The economics of public cloud are particularly compelling for financial forecasting and financial reporting and analysis workloads, where burst compute capacity is essential during quarterly close cycles, stress testing exercises, and regulatory reporting deadlines. Public cloud providers offer elastic compute pricing that allows financial institutions to scale resources up during peak demand periods and scale down immediately thereafter, a capability that private on-premise infrastructure simply cannot replicate cost-effectively.

Key players driving activity within the public cloud segment include Amazon Web Services, Inc., Microsoft, and International Business Machines Corporation. Amazon Web Services, Inc. has built a dedicated financial services competency program that includes pre-validated compliance architectures for frameworks such as PCI-DSS, SOC 2, and ISO 27001, significantly reducing the time-to-compliance for financial institutions migrating workloads. Microsoft has leveraged its Azure for Financial Services initiative to deepen integrations with Dynamics 365 and Power BI, creating an end-to-end cloud environment that spans enterprise resource planning, customer relationship management, and business intelligence — all core application categories within the Finance Cloud Market segmentation.

The public cloud segment's revenue share is not merely holding steady; it is actively consolidating. As financial institutions complete initial cloud migrations for non-core workloads, they are progressively moving mission-critical applications — including core banking ledgers, real-time fraud detection engines, and algorithmic trading platforms — to public cloud environments. This workload graduation effect drives higher per-customer annual contract values for hyperscale vendors and increases switching costs, reinforcing the segment's structural dominance.

The Insurance Technology Market and the RegTech Market are closely linked to public cloud adoption, as insurers and compliance-focused financial institutions leverage public cloud's global scale to deploy AI-driven underwriting models and automated regulatory reporting systems respectively. The convergence of these verticals within public cloud environments is expected to further entrench the segment's leading position through 2033.

Private cloud retains relevance for institutions with specific data residency requirements or those operating in jurisdictions where public cloud usage for certain data classifications remains restricted. Hybrid cloud is the fastest-growing deployment model by CAGR, as institutions pursue a pragmatic middle path that preserves existing private infrastructure investments while selectively migrating high-value workloads to public cloud environments.