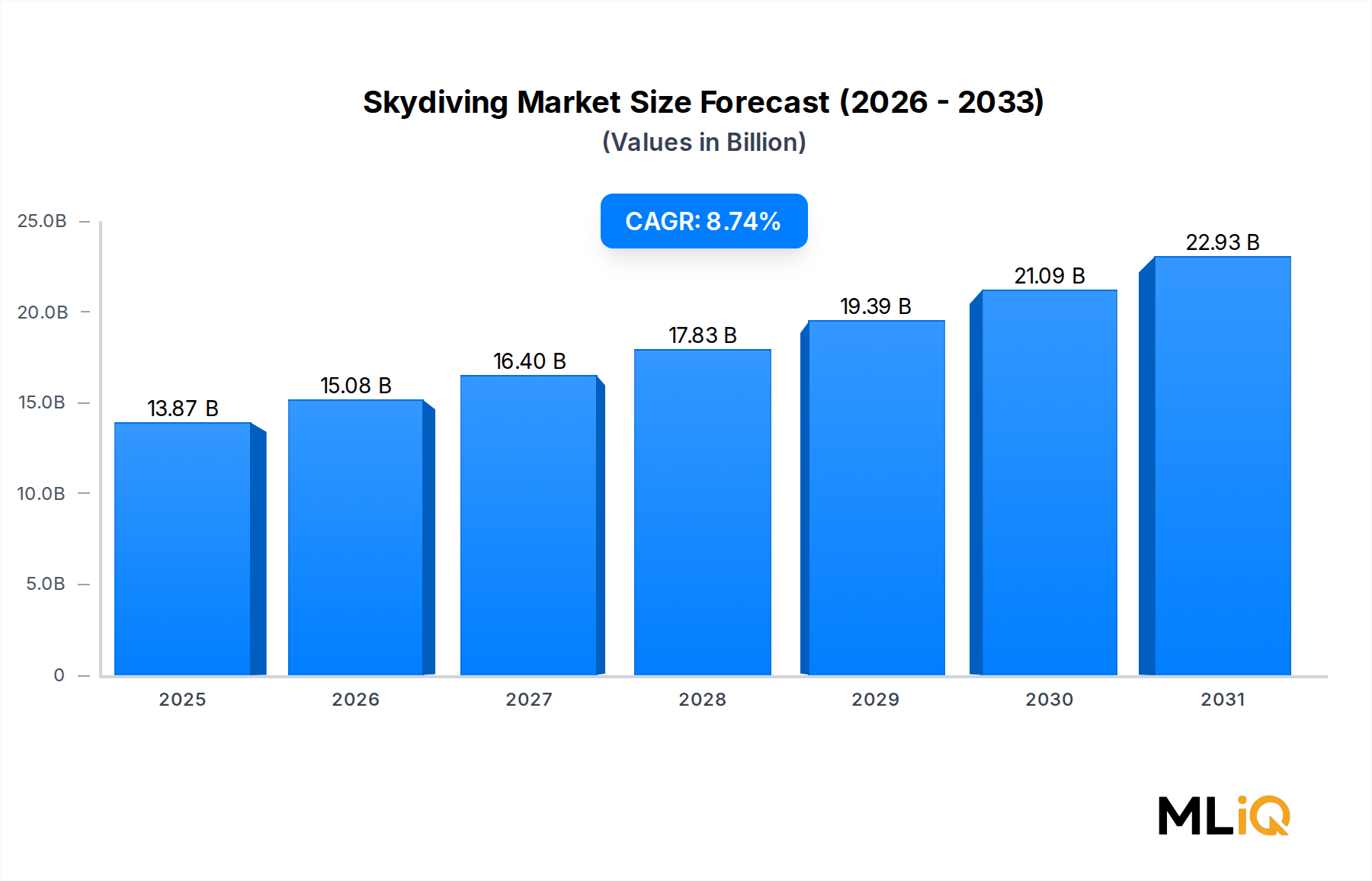

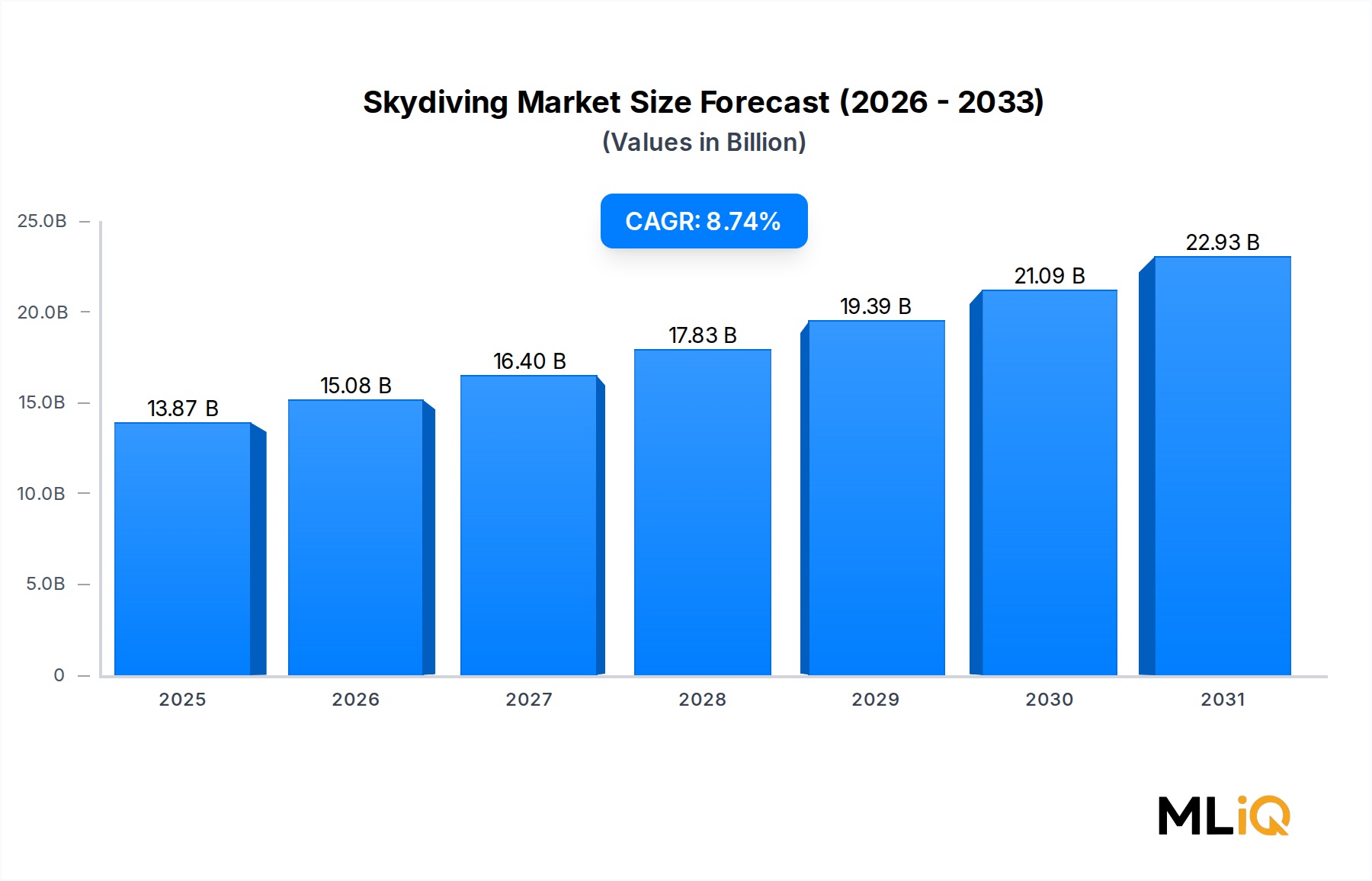

The global skydiving industry is entering a period of accelerated expansion, with the market valued at $13.87 billion in 2025 and projected to grow at a compound annual growth rate (CAGR) of 8.74% through 2033. This robust trajectory reflects a confluence of macro-level tailwinds including rising disposable incomes, the global proliferation of experiential tourism, and the increasing social-media-driven demand for bucket-list activities among younger demographics.

At its core, the skydiving market is benefiting from a structural shift in consumer spending away from material goods toward memorable, shareable experiences. Millennials and Generation Z — now the dominant consumer cohorts — are disproportionately represented among first-time jumpers and repeat participants, driving sustained demand across tandem, freefly, and canopy piloting disciplines. The normalization of extreme and adventure activities through platforms such as Instagram, YouTube, and TikTok has materially lowered the psychological barrier to participation, effectively expanding the addressable consumer base.

From a supply-side perspective, drop zone operators are increasingly investing in modern aircraft fleets, enhanced instructor certification programs, and digital booking infrastructure to meet surging demand. The integration of high-definition wearable cameras, GPS tracking, and automated altitude-awareness devices has significantly improved perceived safety, which remains the single largest deterrent for new participants. As safety records improve and are more transparently communicated, conversion rates from "interested" to "paying customer" continue to climb.

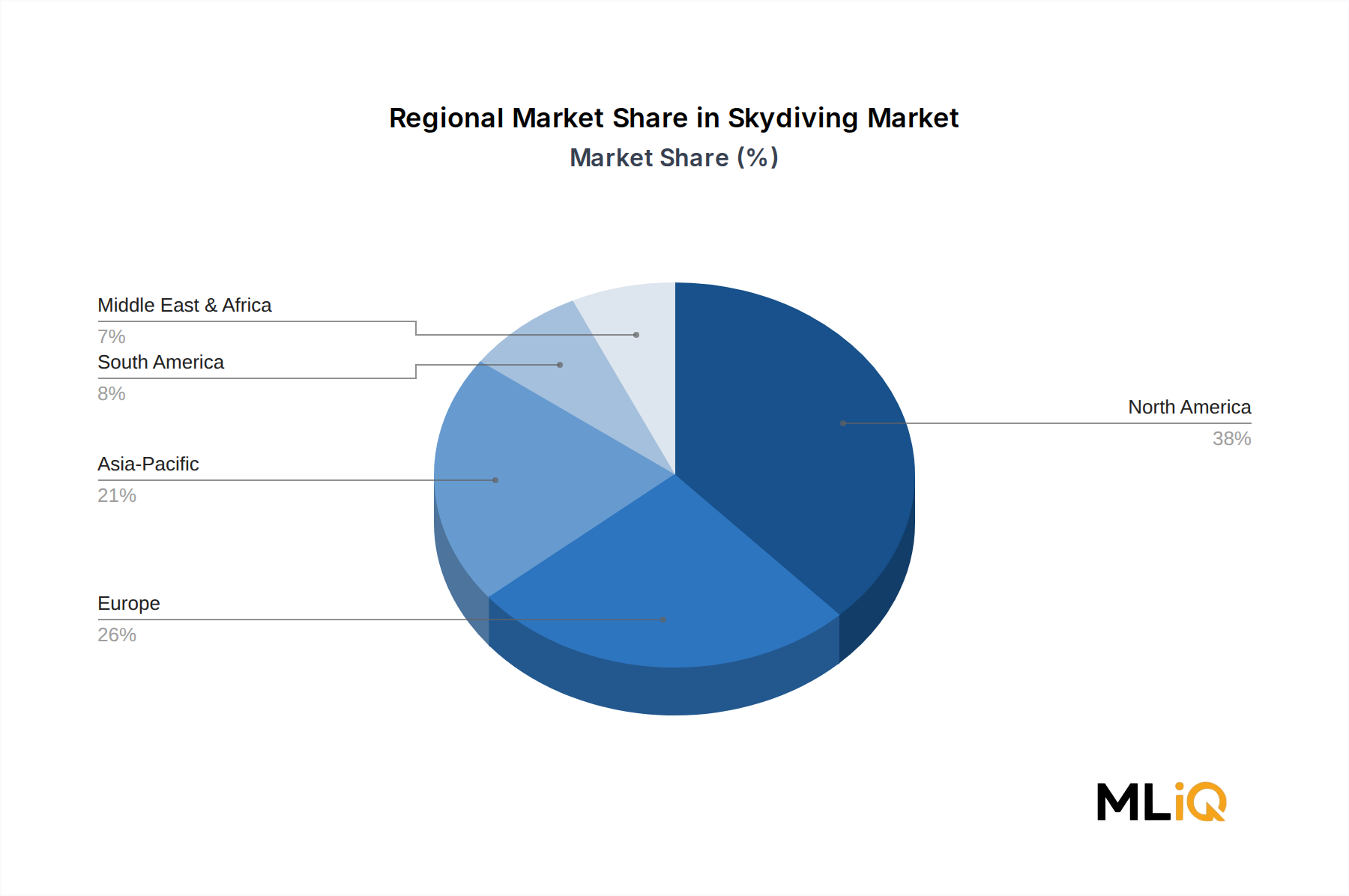

Geographically, North America remains the most mature market, anchored by a well-established network of FAA-regulated drop zones, while the Asia Pacific region is emerging as the fastest-growing geography, fueled by a burgeoning middle class in China, India, and Southeast Asia. Europe maintains a strong and stable base, particularly in the United Kingdom, Germany, and France, underpinned by deep sport parachuting traditions and strong regulatory oversight.

Looking ahead, the market is expected to surpass $27 billion by 2033, driven by the continued growth of tandem skydiving as an accessible entry point, rising corporate team-building expenditure on adventure activities, and expanding military and professional training applications. The proliferation of indoor skydiving as a feeder activity — introducing participants to freefall dynamics before their first outdoor jump — is also creating a measurable pipeline of new outdoor skydivers. Overall, the market's forward-looking outlook is strongly positive, with operators, equipment manufacturers, and tourism aggregators all positioned to capture substantial value over the forecast horizon.