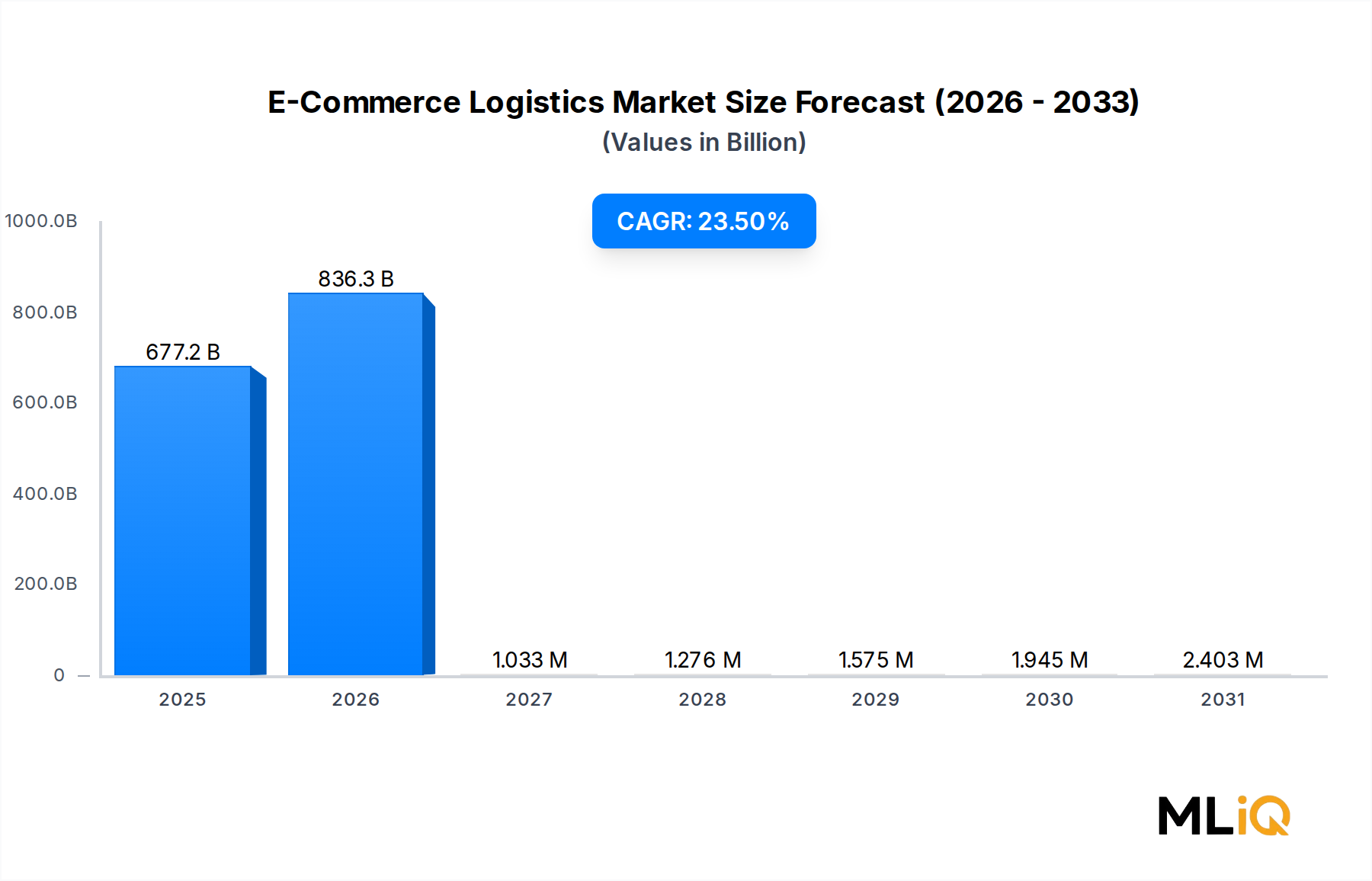

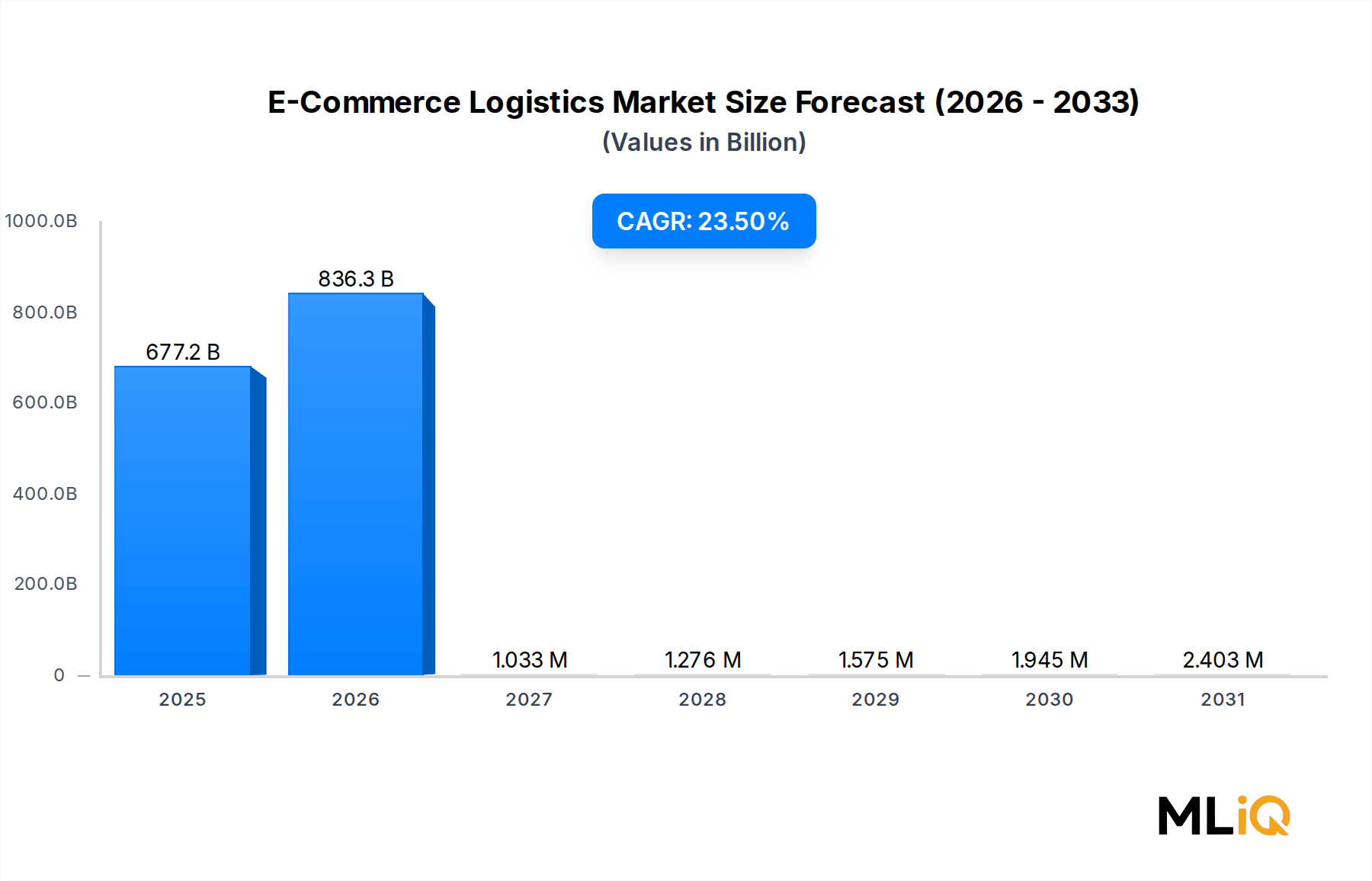

Transportation services constitute the dominant segment within the E-Commerce Logistics Market, commanding the largest share of total market revenue by a substantial margin. This dominance is attributable to the foundational role transportation plays in fulfilling every e-commerce transaction — from first-mile pickup at a seller or manufacturer's facility, through mid-mile linehaul operations, to last-mile delivery at the consumer's doorstep. No e-commerce order can be completed without a transportation layer, making this segment structurally indispensable regardless of category, geography, or price point.

Within the transportation segment, last-mile delivery accounts for the most significant cost and complexity burden. Industry estimates consistently indicate that last-mile operations can represent between 40% and 55% of total end-to-end shipping costs, a figure that has driven relentless innovation in route optimization, delivery density planning, and alternative delivery models. The widespread adoption of crowd-sourced delivery networks, autonomous delivery vehicles, and smart locker solutions reflects the industry's effort to reduce per-unit costs while meeting rising consumer expectations for same-day and next-day fulfillment.

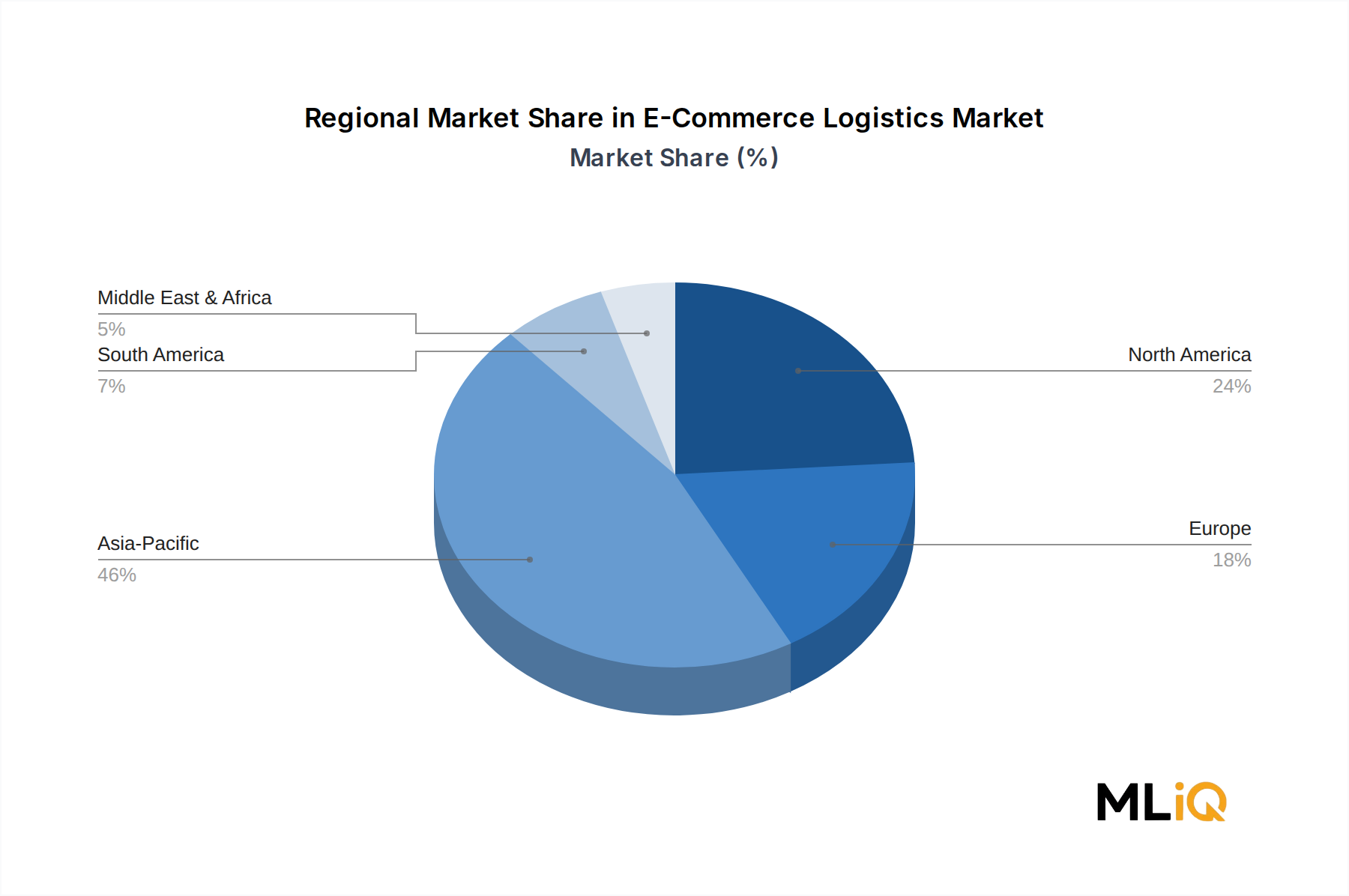

Domestic transportation services account for the majority of volume within the segment, driven by the sheer scale of national e-commerce ecosystems in the United States, China, Germany, India, and Japan. However, international transportation — encompassing air freight, ocean freight, and cross-border parcel services — is growing at a faster relative rate as cross-border e-commerce platforms expand their global reach. The Freight Forwarding Market is a direct beneficiary of this cross-border expansion, as sellers and platforms increasingly require specialized trade compliance, customs brokerage, and international routing expertise.

Key players dominating the transportation segment include United Parcel Service, Inc., FedEx Corporation, DHL International GmbH, and Amazon, all of which have made substantial capital investments in proprietary delivery networks, air cargo fleets, and fulfillment center infrastructure. Amazon in particular has disrupted traditional parcel dynamics by internalizing a growing share of its own delivery volume through Amazon Logistics, fundamentally altering the competitive calculus for third-party carriers.

The segment is also witnessing growing differentiation based on service tier. Standard ground delivery, premium express, and ultra-fast same-day or instant-delivery services are increasingly treated as distinct product lines with separate pricing models, SLA frameworks, and technology investments. This tiered structure allows logistics providers to capture value across the consumer urgency spectrum, though it also increases operational complexity and demands sophisticated Transportation Management System Market solutions for load planning, dynamic pricing, and exception management.

Consolidation dynamics are actively reshaping the competitive topology. Regional carriers with dense coverage in specific metro areas or countries are being acquired by global integrators seeking to plug geographic gaps in their last-mile networks. Meanwhile, asset-light logistics orchestrators and freight brokers are deploying carrier management platforms that aggregate capacity from hundreds of third-party providers, offering shippers flexibility without the capital burden of owning assets. The Parcel Delivery Market feeds directly into these dynamics, as the rapid growth of small-parcel volumes from direct-to-consumer channels continues to strain carrier networks and create premium pricing power for those with reliable urban density coverage.

Looking ahead, transportation's share of total e-commerce logistics revenue is expected to remain dominant through 2033, though its growth rate may moderate slightly relative to warehousing and value-added services as automated fulfillment reduces the number of individual shipment touchpoints required. Companies investing in electric delivery fleets, autonomous vehicles, and AI-driven dispatch optimization will be best positioned to sustain margins as per-unit delivery costs remain under structural pressure.