Software Segment Dominance in the Bitcoin Payments Market

Within the component segmentation of the Bitcoin Payments Market—spanning Hardware, Software, and Services—the Software sub-segment commands the largest revenue share and is exhibiting the most rapid expansion trajectory. This dominance is attributable to several structural and commercial factors that collectively entrench software solutions as the foundational layer of Bitcoin payment infrastructure.

Software-based Bitcoin payment solutions encompass payment gateway platforms, wallet applications, merchant integration SDKs, compliance and KYC/AML tooling, reconciliation engines, and analytics dashboards. Unlike hardware terminals or professional services engagements, software solutions offer near-zero marginal replication costs, enabling providers to scale across geographies and merchant categories without proportionate capital expenditure. This economic architecture drives superior gross margins, typically ranging from 65% to 80% for SaaS-model Bitcoin payment platforms, compared with 30–45% margins characteristic of hardware-centric deployments.

The proliferation of API-first architecture has further entrenched software's dominance. Merchants—from boutique e-commerce operators to multinational retail chains—increasingly demand plug-and-play integration modules compatible with platforms such as Shopify, WooCommerce, Magento, and Salesforce Commerce Cloud. Software vendors that deliver pre-certified plugins and white-label checkout flows dramatically reduce implementation friction, compressing merchant onboarding timelines from weeks to hours.

Key players shaping the software segment include Bitpay, which offers a comprehensive merchant suite supporting Bitcoin and Bitcoin Lightning payments with real-time fiat conversion; OpenNode, which has positioned its Lightning Network-native gateway as the enterprise-grade solution for high-frequency transaction environments; Coinpayments, whose multi-currency software infrastructure supports over 2,000 digital assets including Bitcoin, serving more than 100,000 merchant accounts globally; and Circle, whose programmable payment APIs bridge Bitcoin settlement with stablecoin liquidity rails, serving institutional treasury clients.

The software segment's share is not merely large—it is consolidating. Venture capital allocation toward Bitcoin payment software reached record levels between 2021 and 2024, with platform-layer companies attracting a disproportionate share of Series B and Series C rounds relative to hardware manufacturers or pure-play service providers. This funding dynamic is accelerating product roadmap velocity, enabling software vendors to embed compliance automation, machine learning-based fraud scoring, and real-time analytics that were previously accessible only to tier-one financial institutions.

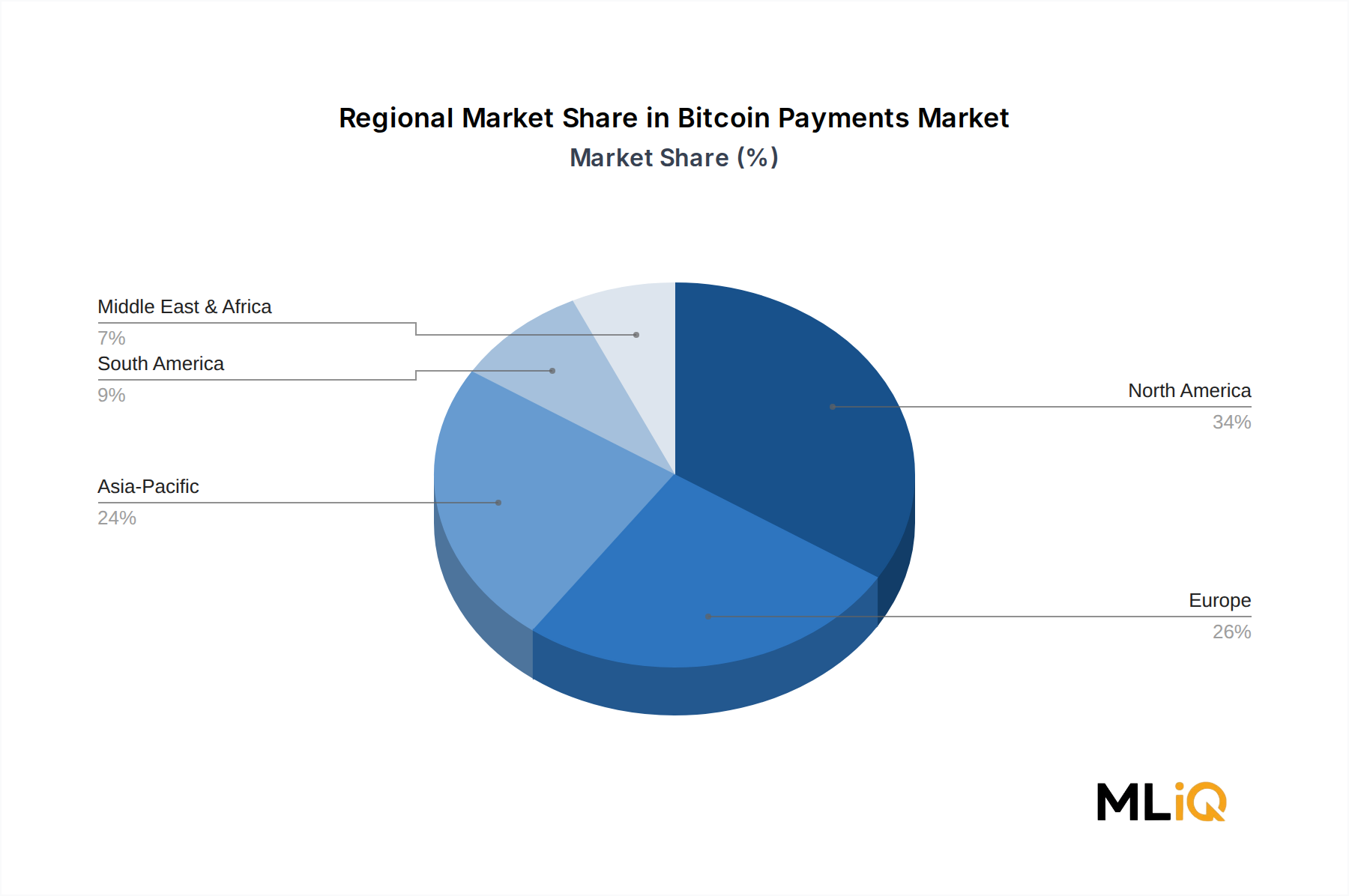

From a regional software adoption standpoint, North America and Western Europe represent the most mature deployment bases, with enterprise software contracts increasingly structured as multi-year SaaS agreements with volume-based pricing tiers. Conversely, Asia-Pacific and Africa represent high-growth greenfield opportunities where mobile-first software architectures—optimized for low-bandwidth environments and feature phone compatibility—are unlocking merchant segments previously excluded from digital payment infrastructure.

The competitive moat for software leaders is deepening through network effects: as more merchants integrate a given platform, the aggregate transaction data generated enables increasingly sophisticated risk models, chargeback prevention algorithms, and dynamic routing optimizations—capabilities that reinforce switching costs and elevate barriers to competitive displacement.