1. What are the major growth drivers for the Recycled Plastic Market market?

Factors such as are projected to boost the Recycled Plastic Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Recycled Plastic Market

Recycled Plastic Market+1 2315155523

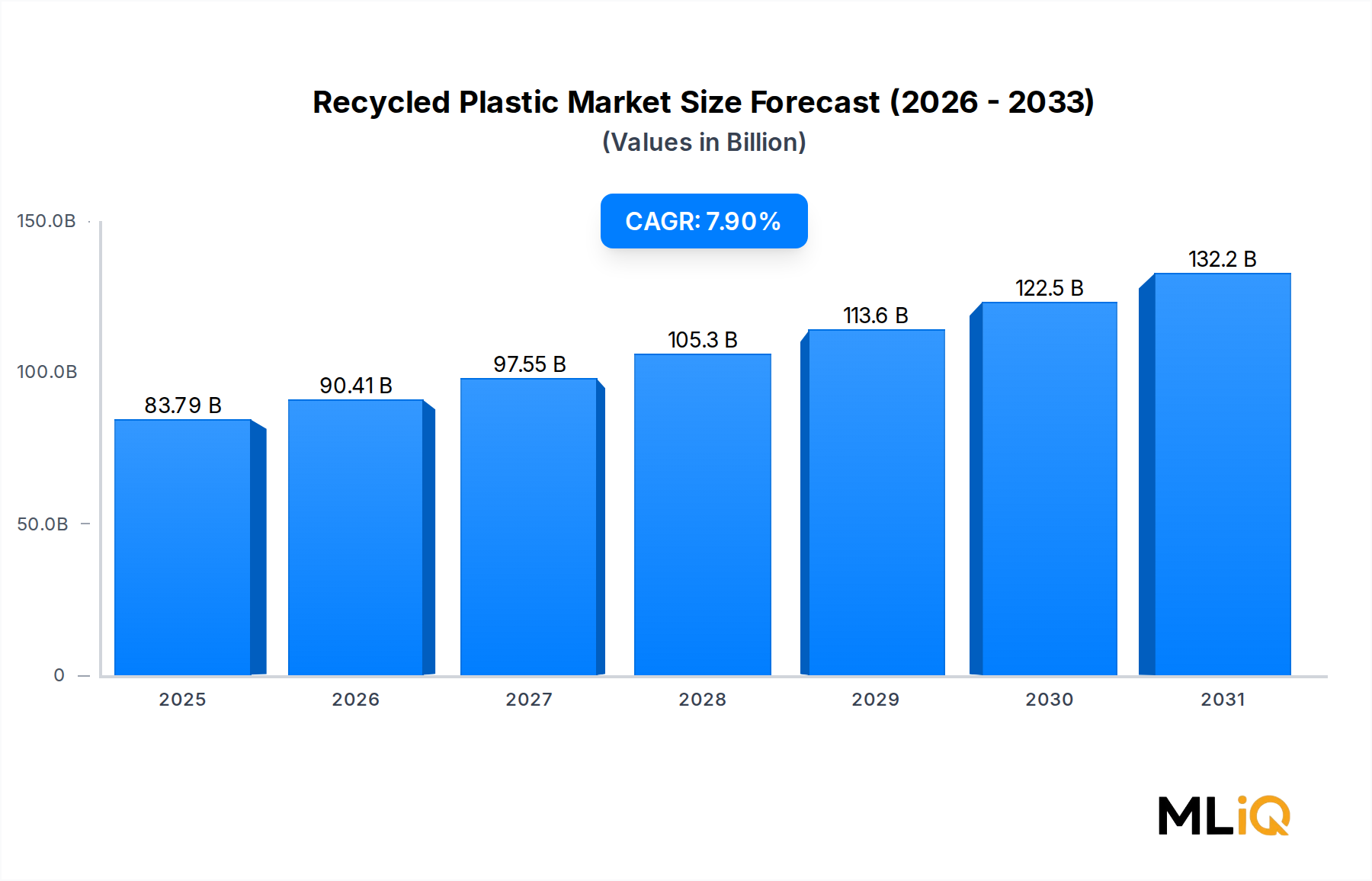

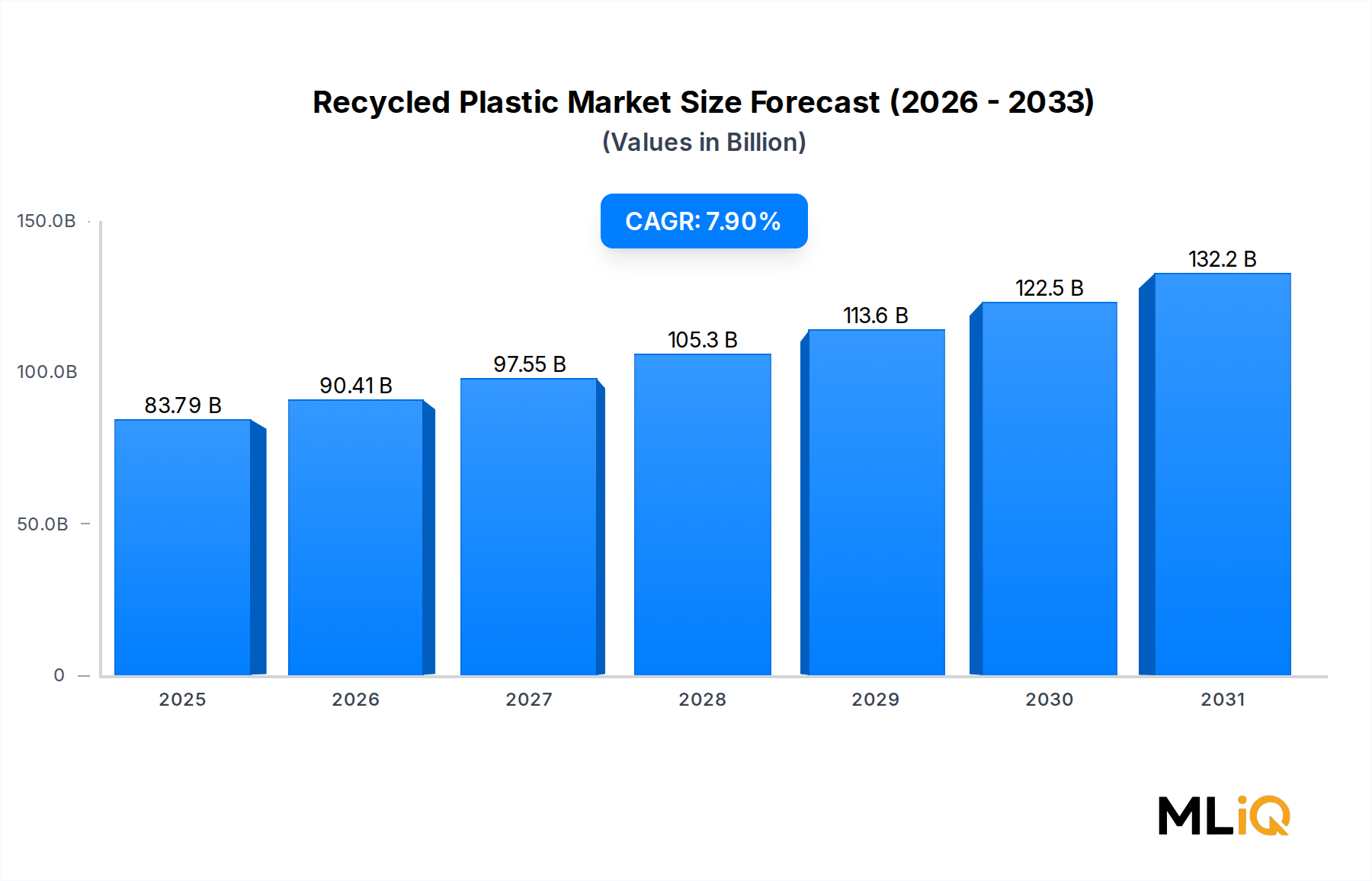

The global Recycled Plastic Market is poised for sustained, high-trajectory expansion over the forecast period 2025–2033, anchored by tightening regulatory frameworks, escalating corporate sustainability mandates, and a structurally shifting consumer preference toward circular material systems. The market was valued at $83.79 billion in the base year and is projected to grow at a compound annual growth rate (CAGR) of 7.9% through 2033, underscoring the accelerating transition from virgin polymer consumption toward closed-loop plastic utilization.

At its core, the market's momentum is driven by three converging macro forces. First, legislative pressure — particularly in the European Union through the Single-Use Plastics Directive and the revised Packaging and Packaging Waste Regulation — is mandating minimum recycled content thresholds across multiple product categories. Second, multinational brand owners in fast-moving consumer goods (FMCG) and retail sectors have publicly committed to integrating 25–50% recycled plastic content in their packaging by 2030, generating a structurally assured demand signal for premium-grade recycled feedstock. Third, improvements in mechanical and chemical recycling technologies are steadily closing the performance and cost gap between recycled and virgin polymers, enabling broader substitution across technically demanding applications.

From a material standpoint, Polyethylene Terephthalate (PET) dominates volume throughput, supported by mature collection infrastructure and robust end-market demand in food-grade packaging and textile fiber applications. High Density Polyethylene (HDPE) and Polypropylene (PP) follow closely, with growing adoption in building products, automotive components, and agricultural applications.

Geographically, Europe leads in regulatory sophistication and collection efficiency, while Asia Pacific — particularly China and India — represents the highest-growth vector given rapid urbanization, increasing plastic consumption, and nascent but fast-scaling formal recycling infrastructure. North America is undergoing a structural transition, with extended producer responsibility (EPR) legislation proliferating across U.S. states and Canada, reshaping investment flows into domestic processing capacity.

Looking forward, the interplay between chemical recycling scale-up, feedstock price volatility, and evolving end-market specifications will define competitive differentiation. Players investing in advanced sorting, decontamination, and quality certification capabilities will capture disproportionate margin share. By 2033, the market's absolute scale and the depth of recycled content integration across value chains are expected to position recycled plastics as a mainstream, not niche, industrial material category.

Polyethylene Terephthalate, universally recognized as PET, commands the largest single revenue share within the Recycled Plastic Market, and its structural dominance reflects decades of investment in collection, sorting, and reprocessing infrastructure. PET's recyclability profile is unmatched among commodity thermoplastics: it can be mechanically recycled into food-grade rPET with well-established decontamination protocols, a prerequisite for re-entry into beverage and food packaging applications — the most volume-intensive and margin-supportive end-use segments.

The dominance of recycled PET is reinforced by several mutually reinforcing dynamics. First, deposit return schemes (DRS) operating across Europe, parts of North America, and select Asia Pacific markets have driven PET bottle collection rates to 70–90% in leading jurisdictions such as Germany and Norway, ensuring a high-quality, consistent feedstock supply. Second, major carbonated soft drink and bottled water companies — including The Coca-Cola Company and PepsiCo — have pledged to incorporate 50% recycled content in primary packaging by 2030, creating legally and reputationally binding demand commitments. Third, the textile industry's appetite for recycled PET fiber (rPET fiber) provides a substantial and growing secondary demand channel, absorbing volumes that food-contact regulations might otherwise restrict.

The PET Resin Market is inextricably linked to recycled plastic economics: when virgin PET resin prices decline due to crude oil price drops or overcapacity in Asian production, the economics of recycled PET come under pressure, compressing processor margins. Conversely, crude oil price spikes or regional virgin resin supply disruptions enhance the competitiveness of rPET, stimulating investment in expanded recycling capacity. This cyclical dependency means that PET recyclers must manage both commodity exposure and regulatory tailwinds simultaneously.

Within the competitive landscape for recycled PET, Clear Path Recycling and Plastipak Holdings are notable for their integrated bottle-to-bottle and bottle-to-fiber recycling capabilities. KW Plastics, while more broadly focused on HDPE and PP, has also scaled PET processing operations. Jayplas in the United Kingdom operates significant PET sorting and pelletizing lines, supplying rPET to major UK and European brand owners.

The segment's share is consolidating rather than fragmenting: capital intensity in food-grade decontamination, the certification requirements imposed by regulatory bodies such as the U.S. FDA and EFSA, and the scale economics of continuous-process extrusion lines are raising barriers to entry and driving consolidation toward larger, vertically integrated processors. Smaller operators are increasingly exiting mechanical recycling in favor of feedstock aggregation roles, supplying sorted flake to centralized pelletizing facilities.

Looking at adjacent competitive pressures, chemical recycling — specifically glycolysis and methanolysis of PET — is beginning to challenge mechanical recycling for colored, contaminated, and multi-layer PET streams that mechanical processes cannot economically handle. While chemical recycling of PET remains at relatively small commercial scale, pilot investments by INEOS, Eastman, and Loop Industries signal that the competitive topology of the segment will evolve materially over the 2025–2033 period. PET's dominance in the Recycled Plastic Market is thus secure in the near term but subject to technology-driven restructuring over the medium horizon.

The Recycled Plastic Market is shaped by a tightly interlocked set of demand drivers and structural constraints, each traceable to specific regulatory, technological, and macroeconomic variables.

Primary Driver — Regulatory Mandated Recycled Content: The European Union's Packaging and Packaging Waste Regulation (PPWR) mandates 30% recycled content in contact-sensitive plastic packaging by 2030 and 65% recycled content across all plastic packaging by 2040. These binding targets create non-discretionary demand for certified recycled resin, effectively establishing a regulatory demand floor independent of virgin polymer price cycles. Similar EPR frameworks are being enacted across 45+ U.S. states as of 2024–2025, expanding the geographic scope of compliance-driven demand.

Secondary Driver — Corporate Sustainability Commitments: An estimated 85% of Fortune 500 consumer goods companies have published plastic packaging reduction or recycled content targets aligned with the Ellen MacArthur Foundation's Global Commitment framework. These commitments, while voluntary, carry reputational and investor risk-management weight, translating into long-term offtake agreements with recycled resin suppliers and supporting price premiums for food-grade rPET and rHDPE of 15–30% above mechanical-grade recycled polymer.

Tertiary Driver — Chemical Recycling Scale-Up: Capital investment in pyrolysis, gasification, and solvolysis technologies exceeded $2.5 billion globally between 2022 and 2024, with facilities coming online across Europe, North America, and Southeast Asia. Chemical recycling expands addressable feedstock — mixed, contaminated, and multi-layer plastics previously directed to energy recovery — materially increasing the total recoverable plastic pool.

Primary Constraint — Feedstock Quality and Availability: Despite rising collection rates, contamination levels in municipal solid waste (MSW) streams remain a persistent challenge, with contamination rates of 15–25% in co-mingled collection systems degrading output quality and increasing processing costs. Inadequate sorting infrastructure in developing markets limits the geographic expansion of quality feedstock sourcing.

Secondary Constraint — Virgin Polymer Price Competition: When Brent crude oil trades below $70/barrel, virgin polyolefin production economics improve materially, compressing the cost differential between virgin and recycled resins and reducing voluntary substitution incentives absent mandatory content requirements.

The competitive landscape of the Recycled Plastic Market is characterized by a blend of integrated resin producers, specialist recyclers, and waste management conglomerates, each occupying distinct positions across the value chain.

Jayplas: A UK-based plastics recycler specializing in post-consumer film, rigid plastics, and PET processing, supplying recycled pellets to major UK and European converters and packaging manufacturers.

B. Schoenberg & Co.: A long-established U.S. plastics regrind and recycling company with broad material coverage across polyolefins and engineering thermoplastics, serving industrial and commercial post-industrial waste streams.

KW Plastics: The world's largest recycler of HDPE and PP, operating high-volume mechanical recycling lines in Troy, Alabama, and supplying recycled resin to manufacturers across packaging, pipe, and automotive sectors globally.

Clear Path Recycling: A joint venture with significant food-grade rPET production capacity, operating bottle-to-bottle recycling lines that supply certified rPET to major beverage and food packaging converters across North America.

Plastipak Holdings: An integrated plastic packaging producer with an embedded recycling division, enabling closed-loop supply of rPET into its own packaging manufacturing operations and third-party customers.

Green Line Polymers: A specialty recycler focused on post-industrial and post-consumer polyolefin streams, offering custom blending and compounding of recycled resins to meet specific end-user performance specifications.

Ultra Poly Corporation: A U.S.-based recycler with a focus on polyethylene and polypropylene post-consumer and post-industrial streams, providing recycled pellets and regrind to film, molding, and pipe manufacturers.

Joes Plastics Inc.: A regional plastics recycling operator specializing in collection, sorting, and granulation of mixed plastic waste streams, serving regional converters and compounders as a feedstock aggregator.

Custom Polymers: A custom recycling and compounding company with capabilities in blending recycled resins with virgin materials and additives to meet specification-grade requirements for automotive, consumer goods, and construction applications.

Veolia: A global environmental services leader operating an extensive network of plastic sorting, washing, and reprocessing facilities across Europe, Asia, and the Americas, leveraging waste management infrastructure to secure large-volume feedstock access.

January 2024: The European Commission formally adopted the revised Packaging and Packaging Waste Regulation (PPWR), establishing legally binding recycled content mandates for plastic packaging across all EU member states, creating a regulatory demand foundation for the 2025–2040 period.

March 2024: KW Plastics announced a capacity expansion at its Troy, Alabama facility, increasing annual HDPE recycling throughput by 120,000 metric tons, one of the largest single-site capacity additions in North American plastic recycling history.

May 2024: Veolia completed the acquisition of a major European plastic sorting platform, consolidating feedstock access across France, Germany, and the Benelux region and integrating AI-powered optical sorting technology.

July 2024: The U.S. Environmental Protection Agency (EPA) released updated national recycling targets under the National Recycling Strategy, setting a 50% municipal solid waste recycling rate goal by 2030, with plastics identified as a priority material category.

September 2024: Plastipak Holdings announced a strategic partnership with a leading chemical recycling technology provider to integrate depolymerized PET feedstock into its food-grade resin supply chain, diversifying sourcing beyond mechanical recycled streams.

November 2024: Clear Path Recycling received FDA No Objection Letter renewal for its bottle-to-bottle rPET process, reaffirming food-contact compliance and enabling continued supply to major North American beverage companies.

February 2025: India's Ministry of Environment, Forest and Climate Change expanded Extended Producer Responsibility (EPR) obligations to cover all plastic packaging categories, mandating minimum recycled content integration across domestic supply chains from 2026 onward.

The Recycled Plastic Market exhibits pronounced regional heterogeneity, reflecting divergent regulatory environments, infrastructure maturity, and industrial demand profiles across geographies.

Europe represents the most mature regional market, accounting for an estimated 32–35% of global recycled plastic demand by value. The region benefits from the world's most comprehensive Extended Producer Responsibility frameworks, deposit return schemes achieving collection rates above 85% in Nordic and German markets, and mandatory recycled content legislation under the PPWR. Regional CAGR is estimated at 6.8% through 2033, reflecting maturity rather than deceleration — growth is quality-driven, with increasing investment in food-grade and advanced recycling capacity.

Asia Pacific is the fastest-growing region, projected at a CAGR of 9.4% through 2033, driven primarily by China's National Sword policy aftermath — which has redirected domestic attention toward building domestic recycling infrastructure — and India's rapidly expanding EPR framework. China alone is investing heavily in mechanical and chemical recycling capacity to reduce import dependency on virgin resin and meet domestic circular economy targets under its 14th Five-Year Plan. Southeast Asian markets including Indonesia, Vietnam, and the Philippines are also scaling collection and processing infrastructure under pressure from international brand owners and domestic regulatory tightening.

North America holds an estimated 28–30% global revenue share, with the United States representing the dominant contributor. The region is undergoing a structural regulatory transition, with EPR laws enacted in California, Maine, Oregon, and Colorado beginning to reshape collection infrastructure and investment incentives for domestic recycling capacity. Regional CAGR is estimated at 7.2%, broadly aligned with the global average, supported by capital deployment from both strategic players and private equity.

Middle East and Africa and South America represent smaller but emerging markets. Brazil leads Latin American plastic recycling, leveraging an established informal waste picker network that delivers high collection efficiency at low formal infrastructure cost. The region is projected at a CAGR of 8.1%. The Middle East and Africa region lags in collection infrastructure but is attracting pilot investments as part of national circular economy strategies in GCC countries, projecting a CAGR of 7.5% from a lower base.

Pricing dynamics in the Recycled Plastic Market are inherently complex, shaped by the dual influence of virgin polymer commodity cycles and the structural cost architecture of collection, sorting, and reprocessing operations. Unlike virgin plastics, which are priced with reference to naphtha cracking economics and olefin derivatives markets, recycled plastic pricing is determined by a layered interplay of feedstock acquisition costs, processing economics, and end-market specification premiums.

Food-grade rPET commands the highest price premium in the recycled resin market, typically trading at 15–30% above commodity-grade recycled PET flake and at a 10–20% premium versus virgin PET under crude oil price scenarios above $80/barrel. This premium is supported by the certification costs embedded in FDA and EFSA compliance, the capital intensity of Super Clean recycling lines, and structurally constrained supply relative to brand-owner demand.

For commodity-grade recycled polyolefins — rHDPE and rPP — pricing is more volatile and more directly correlated with virgin resin markets. When polyethylene or polypropylene spot prices decline sharply, as occurred during 2022–2023 amid global resin oversupply, recycled polyolefin processors faced margin compression as rPP and rHDPE prices tracked downward without a commensurate reduction in collection and sorting costs, which are largely fixed.

Value chain margin distribution is uneven. Feedstock aggregators and collectors operate on thin margins of 3–7% gross, while pelletizing and compounding operations targeting specification-grade output earn gross margins in the 12–20% range

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Recycled Plastic Market market expansion.

Key companies in the market include Jayplas, B. Schoenberg & Co., KW Plastics, Clear Path Recycling, Plastipak holdings, Green Line Polymers, Ultra Poly Corporation, Joes Plastics Inc., Custom Polymers, Veolia.

The market segments include Type, High Density Polyethylene, Polypropylene, End-use Industry.

The market size is estimated to be USD 83.79 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Recycled Plastic Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Recycled Plastic Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.