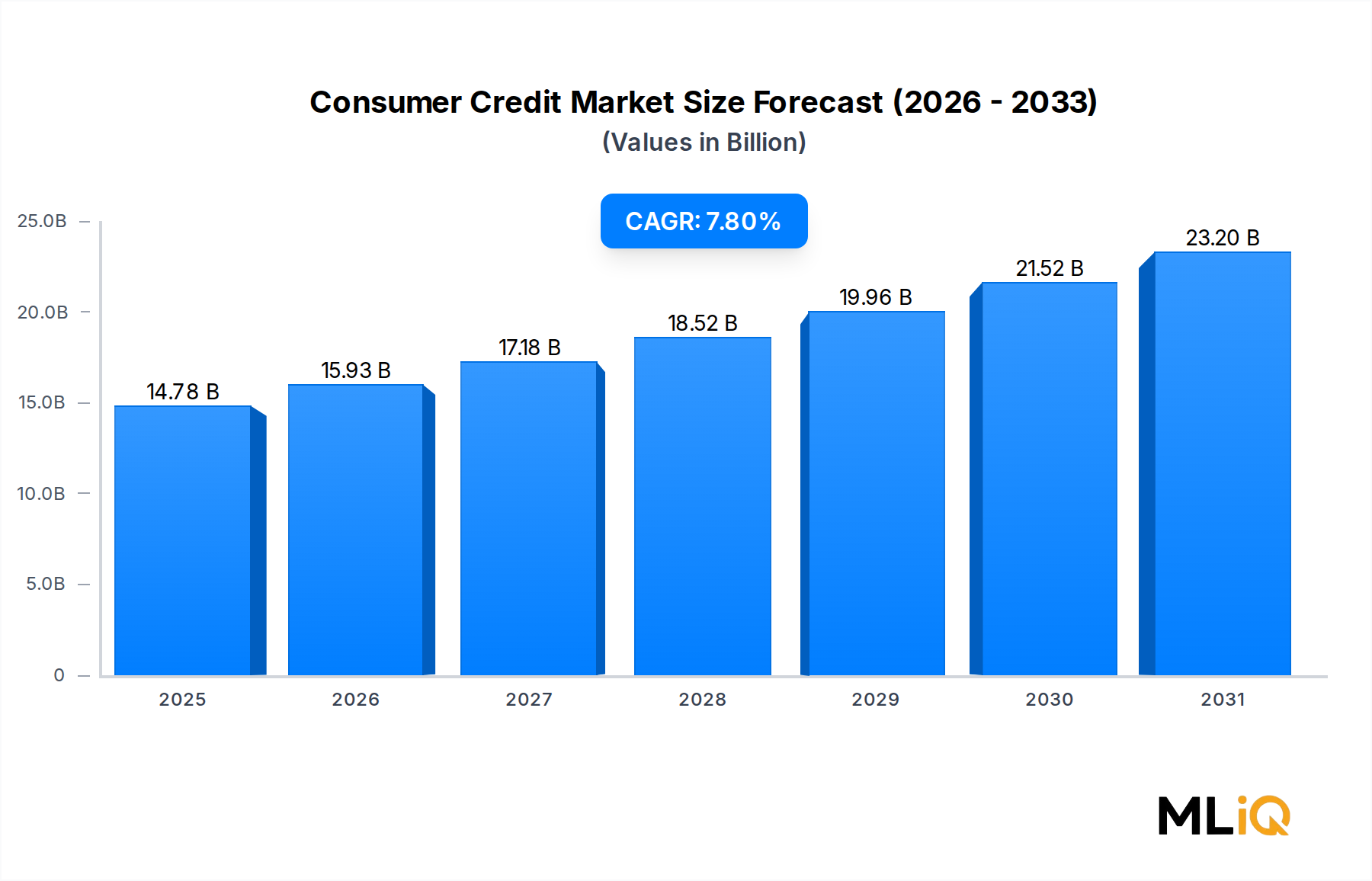

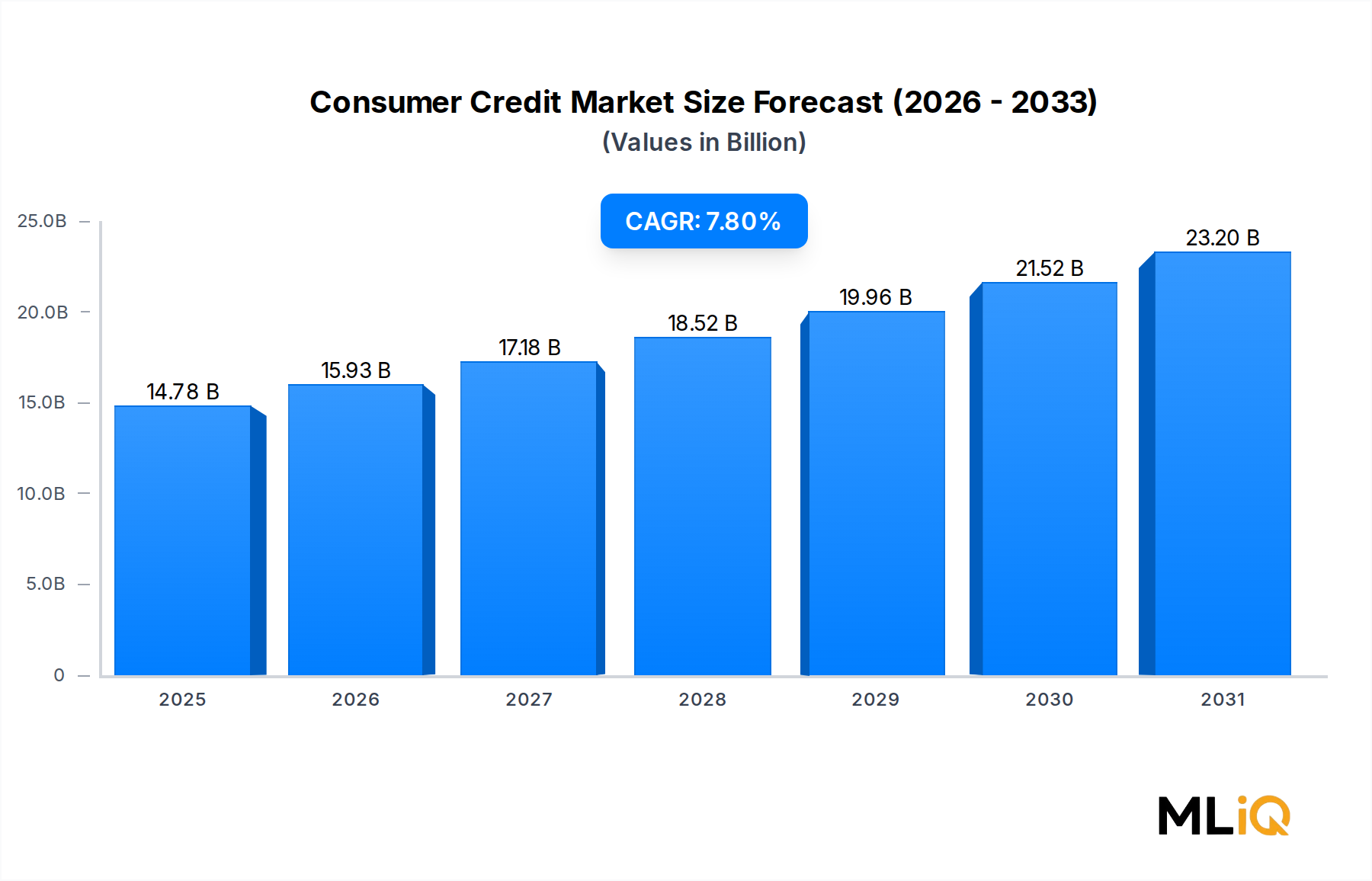

Revolving Credit Dominance in the Consumer Credit Market

Within the segmentation of the Consumer Credit Market by credit type, revolving credits represent the single largest revenue-generating sub-segment. Revolving credit instruments — most prominently credit cards but also home equity lines of credit and other open-end facilities — are characterized by their flexibility, repeat usability without reapplication, and the ability for borrowers to carry balances across billing cycles. These structural attributes make them both commercially attractive to issuers and operationally convenient for consumers, which collectively explain their dominant market share.

From a revenue perspective, revolving credit generates income across multiple streams: net interest income on outstanding balances, interchange fees on transactions, annual fees, and penalty charges. This multi-vector revenue architecture gives issuers significantly higher lifetime value per account compared to closed-end, non-revolving instruments. As a result, large financial institutions — including JPMorgan Chase & Co, Bank of America Corporation, Citigroup, and Barclays Bank Plc — have historically allocated disproportionate capital and marketing resources toward revolving credit portfolios.

The dominance of revolving credit is further reinforced by network effects embedded in the Credit Card Market. The global acceptance infrastructure of card networks, loyalty and rewards ecosystems, and the deep integration of cards into e-commerce and contactless payment environments create powerful switching costs for consumers. These dynamics sustain high retention rates and recurring utilization, which translate into durable revenue streams for issuers.

However, the segment's dominance is evolving rather than static. Several structural forces are reshaping the competitive intensity within revolving credit. First, the rise of the Buy Now Pay Later Market has introduced a substitute credit mechanism for point-of-sale financing, particularly in retail and e-commerce contexts. While BNPL products are technically non-revolving, they siphon transaction volume and spending share away from credit cards, especially among millennials and Gen Z borrowers.

Second, regulatory scrutiny around revolving credit pricing — particularly interchange fee caps in Europe and interest rate disclosure requirements in North America — is compressing revenue per account. The European Union's Consumer Credit Directive revisions and the U.S. Consumer Financial Protection Bureau's (CFPB) ongoing oversight have introduced compliance obligations that increase operational costs for revolving credit issuers.

Despite these pressures, revolving credit is not losing its structural primacy. The segment benefits from an unmatched combination of consumer familiarity, institutional infrastructure, and regulatory clarity relative to newer entrants. Issuers are responding to competitive and regulatory pressures by investing in AI-driven limit management, real-time fraud detection, and personalized rewards optimization — all aimed at deepening engagement and defending utilization rates.

The integration of revolving credit products into the broader Digital Banking Market ecosystem is also a key consolidation driver. Major banks are embedding credit card management within unified digital banking apps, using behavioral analytics to proactively offer credit limit adjustments, balance transfer options, and spending insights. This creates a stickier, more data-rich relationship that reinforces the revolving credit segment's strategic centrality within issuer portfolios.

Looking at the issuer landscape, banks remain the dominant originators of revolving credit globally, accounting for the majority of outstanding balances. NBFCs and fintech lenders are more active in personal and installment lending (non-revolving), leaving the revolving segment as a banking-sector stronghold. This pattern is expected to persist through 2033, with the revolving credit sub-segment retaining its position as the largest contributor to total Consumer Credit Market revenues.