Battery Electric Truck Segment Dominance in the Electric Truck Market

Within the Electric Truck Market's propulsion segmentation—which spans Battery Electric Trucks, Hybrid Electric Trucks, and Plug-In Hybrid Electric Truck and Fuel Cell Electric Truck configurations—the Battery Electric Truck (BET) sub-segment commands the dominant revenue share and is consolidating its leadership position as technology maturity accelerates and infrastructure investment scales.

Battery Electric Trucks derive their market dominance from several structurally reinforcing factors. First, declining lithium-ion battery pack costs have dramatically reduced the acquisition price premium over diesel counterparts in the light- and medium-duty segments, making the BET value proposition increasingly straightforward for urban fleet managers. Second, the operational simplicity of battery-electric drivetrains—characterized by fewer moving parts, reduced maintenance intervals, and elimination of complex exhaust after-treatment systems—delivers measurable lifecycle cost advantages that resonate strongly with logistics operators focused on total fleet cost management.

Third, the maturing charging infrastructure ecosystem—particularly depot charging solutions deployed at distribution centers, warehouses, and logistics hubs—has substantially reduced range anxiety for predictable, route-based commercial applications. Operators running fixed daily routes with known energy consumption profiles can deploy BETs with high confidence in operational reliability. This structural alignment between BET capability and fleet operating patterns in urban and regional logistics contexts is a principal reason the sub-segment commands disproportionate market share.

From a vehicle-type perspective, Light Duty Electric Trucks have historically led BET adoption given their shorter required range, higher duty-cycle regularity, and greater alignment with current battery energy density. However, the Medium Duty and Heavy-Duty Electric Truck categories are emerging as the next high-growth frontier. OEMs including AB Volvo, Daimler AG, Paccar Inc., and BYD Compay Ltd. have launched or announced production-ready heavy-duty BET platforms with ranges exceeding 300 miles on a single charge, directly addressing the persistent range constraint that has historically constrained heavy-duty adoption.

AB Volvo's FL Electric and FH Electric platforms represent the European vanguard of heavy-duty BET commercialization, while BYD Compay Ltd. leverages vertically integrated battery manufacturing to price its BET products aggressively across Asian and increasingly Western markets. Daimler AG, through its Freightliner eCascadia and Mercedes-Benz eActros product lines, is targeting the North American and European long-haul corridors respectively. Paccar Inc., through its Kenworth T680E and Peterbilt 579EV, has established a credible North American heavy-duty BET portfolio backed by dealer network support infrastructure.

The BET sub-segment's revenue share is not merely holding steady—it is actively expanding. Hybrid and plug-in hybrid configurations, while retaining relevance as transitional technologies for operators with range requirements exceeding current pure-electric capabilities, are progressively being displaced in short- and medium-haul applications as BET range extends. The competitive pressure on hybrid configurations from advancing BET technology mirrors the broader pattern observed in the Battery Electric Vehicle Market, where hybridization has served as a bridge technology rather than a long-term equilibrium state.

Investment flows further reinforce BET dominance. Venture capital, private equity, and corporate R&D spending are disproportionately directed at battery technology, BET-specific chassis development, and high-power charging systems rather than hybrid drivetrain refinement. This capital allocation dynamic will sustain BET's structural advantage across the forecast horizon, with the sub-segment projected to represent over 60% of total Electric Truck Market revenues by 2028.

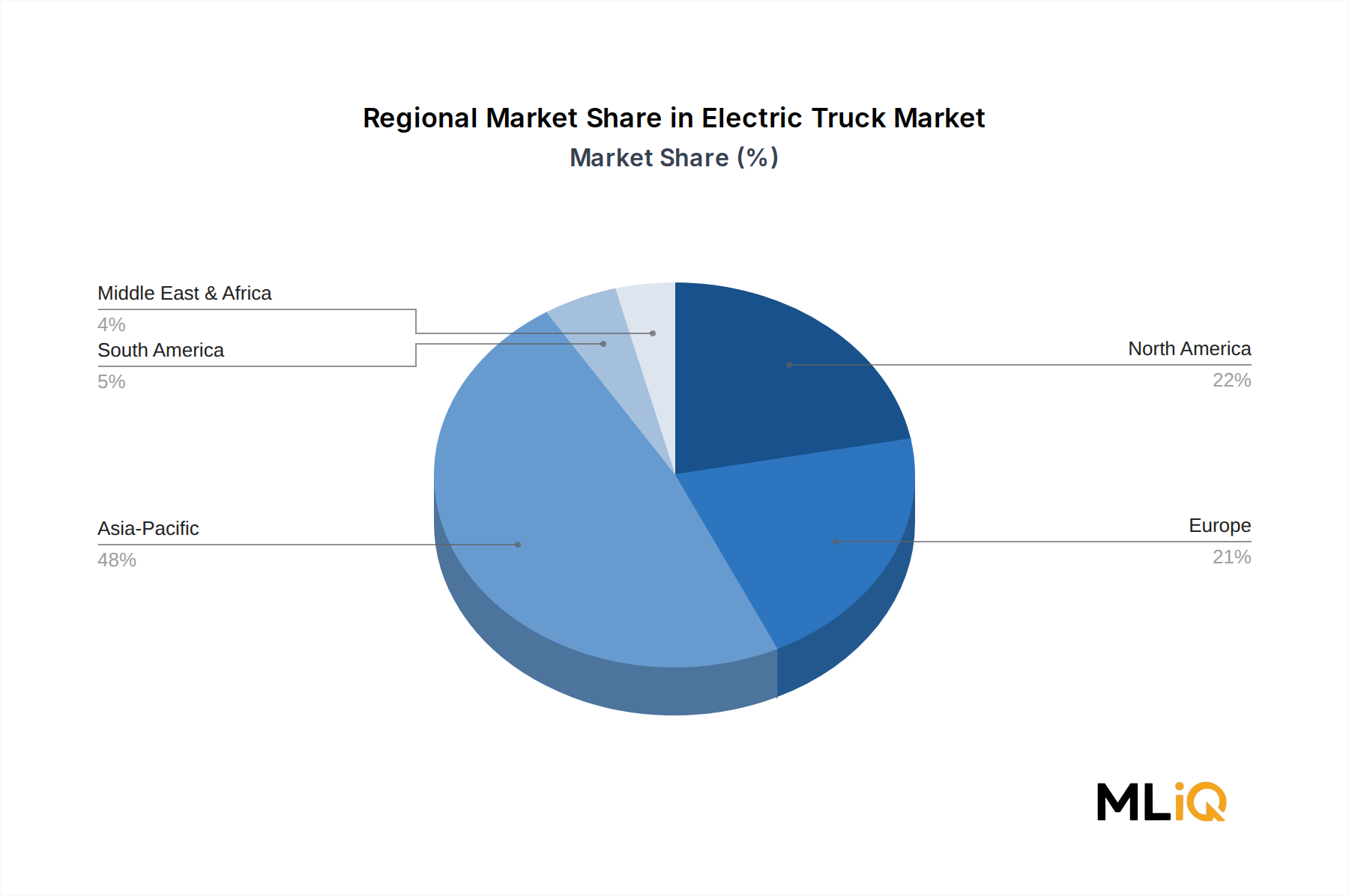

Geographically, China leads BET truck deployments in absolute volume terms, benefiting from a vertically integrated domestic supply chain, aggressive policy support, and the market presence of BYD Compay Ltd., Dongfeng Motor Company, and Geely Automobiles Holdings Limited. Europe follows as the second-largest BET truck market, driven by CO2 fleet standards and urban low-emission zone requirements. North America is the fastest-growing regional BET truck market on a percentage basis, propelled by the Inflation Reduction Act incentive architecture and major fleet operator procurement commitments.