Dominant Segment Analysis: Apparel and Fashion in the Wool Industry Market

The apparel and fashion segment constitutes the largest revenue-generating category within the Wool Industry Market, commanding an estimated 58–62% of total market revenue during the current assessment period. This dominance is rooted in wool's unparalleled combination of tactile comfort, thermal performance, and aesthetic versatility—attributes that translate directly into premium pricing power across menswear, womenswear, and activewear categories.

Within the apparel segment, Merino Wool Market products have emerged as the most dynamically expanding sub-category, driven by their application in base layers, athleisure, travel wear, and fine suiting. Merino wool's fineness—typically ranging between 15.5 and 24 microns—renders it non-itchy against the skin, enabling direct-to-skin applications that broader-count wools cannot achieve. This has facilitated significant market penetration in the performance outdoor and travel apparel segments, where brands such as Icebreaker, Smartwool (a subsidiary of VF Corporation), and Allbirds have successfully positioned merino as a technically superior natural fiber.

The suiting and formal wear sub-segment, historically the anchor of wool apparel demand, has undergone structural recalibration in the post-pandemic operating environment. While remote work normalization initially compressed demand for tailored wool suits, a post-2022 rebound in corporate travel, in-person business events, and luxury occasion dressing has reinvigorated this channel. Bespoke and made-to-measure tailors across London's Savile Row, Milan's fashion district, and emerging luxury retail corridors in Shanghai and Dubai have reported accelerated order volumes, reflecting the enduring aspiration value of wool tailoring.

Knitted wool garments—including sweaters, cardigans, and wool-blend jerseys—represent a third critical sub-segment, with demand closely correlated to seasonal retail cycles in temperate markets. The increasing popularity of capsule wardrobe concepts and investment dressing has bolstered consumer willingness to pay a premium for high-quality knitted wool pieces, further reinforcing segment revenue resilience.

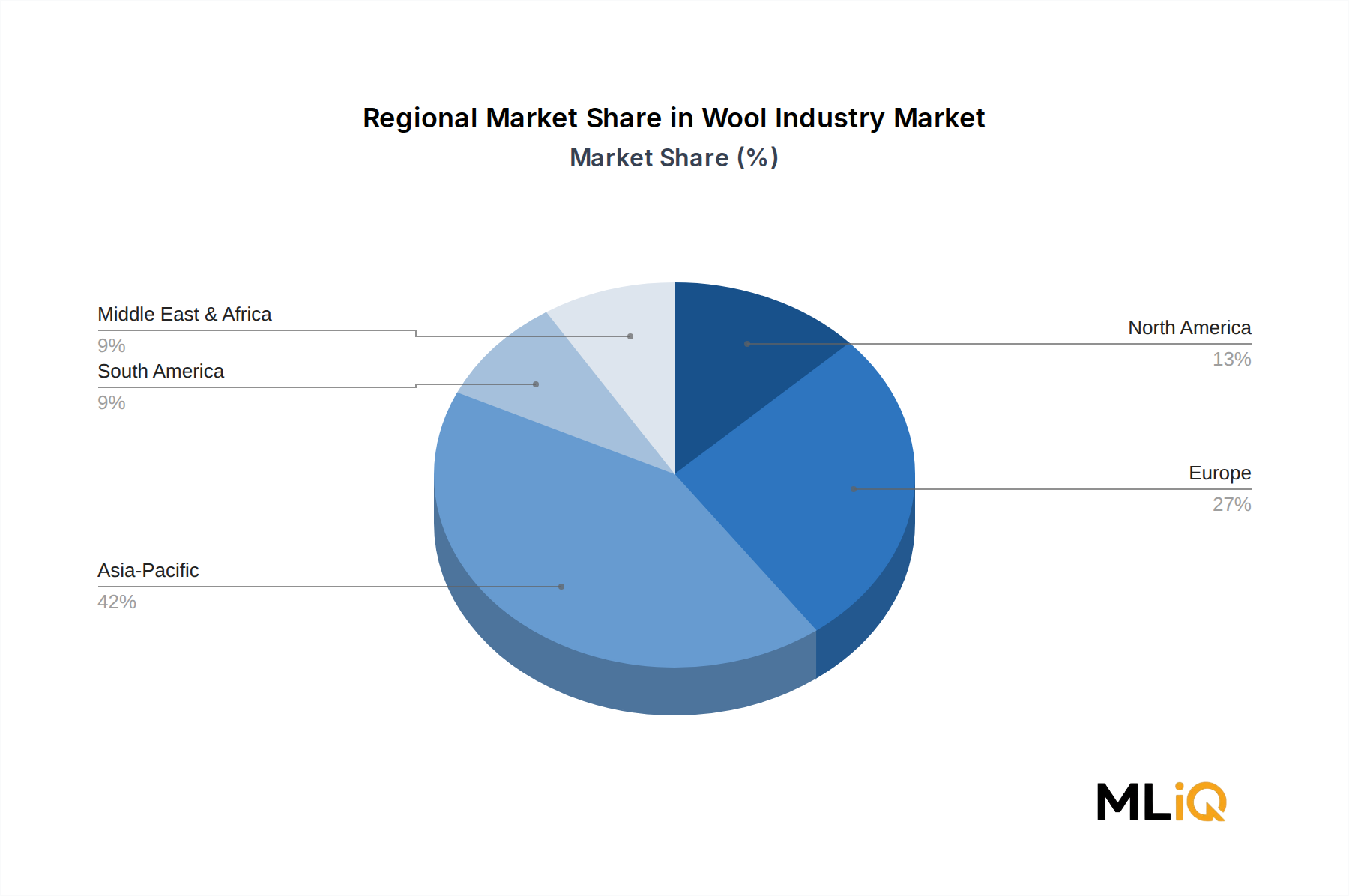

From a geographic lens within the apparel segment, Europe accounts for the largest share of wool apparel consumption by value, reflecting both the region's deep fashion heritage and its stringent environmental preferences favoring natural over synthetic fibers. Italy, the United Kingdom, France, and Germany collectively anchor European wool apparel demand, supported by a robust domestic luxury and fast-premium fashion infrastructure.

In Asia Pacific, China's transition from a purely volume-driven manufacturing economy to a consumption-driven one has created a rapidly expanding domestic market for premium wool apparel. Chinese middle-class consumers are increasingly brand-aware and sustainability-conscious, creating receptive conditions for wool apparel brands that communicate provenance, certification, and craftsmanship narratives effectively.

Competitive dynamics within the dominant apparel segment are shaped by a mix of global luxury conglomerates (LVMH, Kering, Ermenegildo Zegna Group), mid-market performance brands, and vertically integrated wool-to-garment manufacturers. The segment's concentration is moderate, with the top 10 apparel companies by wool consumption accounting for approximately 30–35% of segment-level demand. The remainder is fragmented across thousands of independent designers, regional brands, and private-label retailers, creating a structurally competitive and innovation-rich environment.