Smooth Peanut Butter Segment Dominance in the Peanut Butter Market

Within the Peanut Butter Market, product form remains the most commercially decisive segmentation axis. The smooth peanut butter sub-segment commands the largest share of global revenues, consistently outperforming the crunchy variant across nearly all geographies. Industry estimates suggest smooth peanut butter accounts for approximately 55–60% of total market value, a position reinforced by its universal appeal across age groups, culinary applications, and retail formats.

The dominance of smooth peanut butter is grounded in several structural factors. First, texture preferences among children — who represent a major consumption cohort — skew heavily toward smooth varieties, making it the default household purchase for families. Market research consistently indicates that households with children aged 4–14 are the highest-volume buyers of smooth peanut butter, purchasing on average 20–30% more units annually than non-family households.

Second, smooth peanut butter is disproportionately favored in foodservice, bakery, and industrial applications. When used as an ingredient in sauces, confectionery fillings, smoothies, protein shakes, and baked goods, smooth varieties offer superior mixing consistency and a more homogenous texture. This makes the sub-segment deeply embedded in the supply chains of the Bakery Ingredients Market and the Confectionery Market, both of which represent high-volume, recurring demand pools. For instance, peanut butter is a core input in chocolate-peanut butter cups, sandwich cookies, protein bars, and Asian-style satay sauces, all of which rely on the uniformity of smooth formulations.

Third, smooth peanut butter benefits from its alignment with low-sodium and low-sugar reformulation trends. Manufacturers have found it technically easier to reduce salt and sugar content while maintaining palatable texture in smooth varieties compared to crunchy formats, where the granular peanut pieces can accentuate off-flavors when additives are removed.

Key players driving growth within the smooth segment include Hormel Foods Corporation, which markets the Skippy brand globally and has invested significantly in smooth variant innovations including natural and no-stir formulations. The J.M. Smucker Company, through its Jif brand, maintains the highest market share in the United States for smooth peanut butter and has leveraged its supply chain scale to offer competitive pricing across retail tiers. Unilever's Calvé brand dominates the smooth segment across several European markets, particularly the Netherlands and Germany, where peanut butter consumption per capita has grown significantly over the past decade.

The smooth segment's market share appears to be consolidating rather than declining, as private-label retailers have primarily entered the smooth sub-segment rather than crunchy, further crowding the competitive space and pressuring margins for mid-tier branded players. However, premiumization is creating a bifurcated dynamic: at the value end, private-label smooth peanut butter is gaining shelf space, while at the premium end, artisanal and organic smooth varieties are capturing share from conventional branded products.

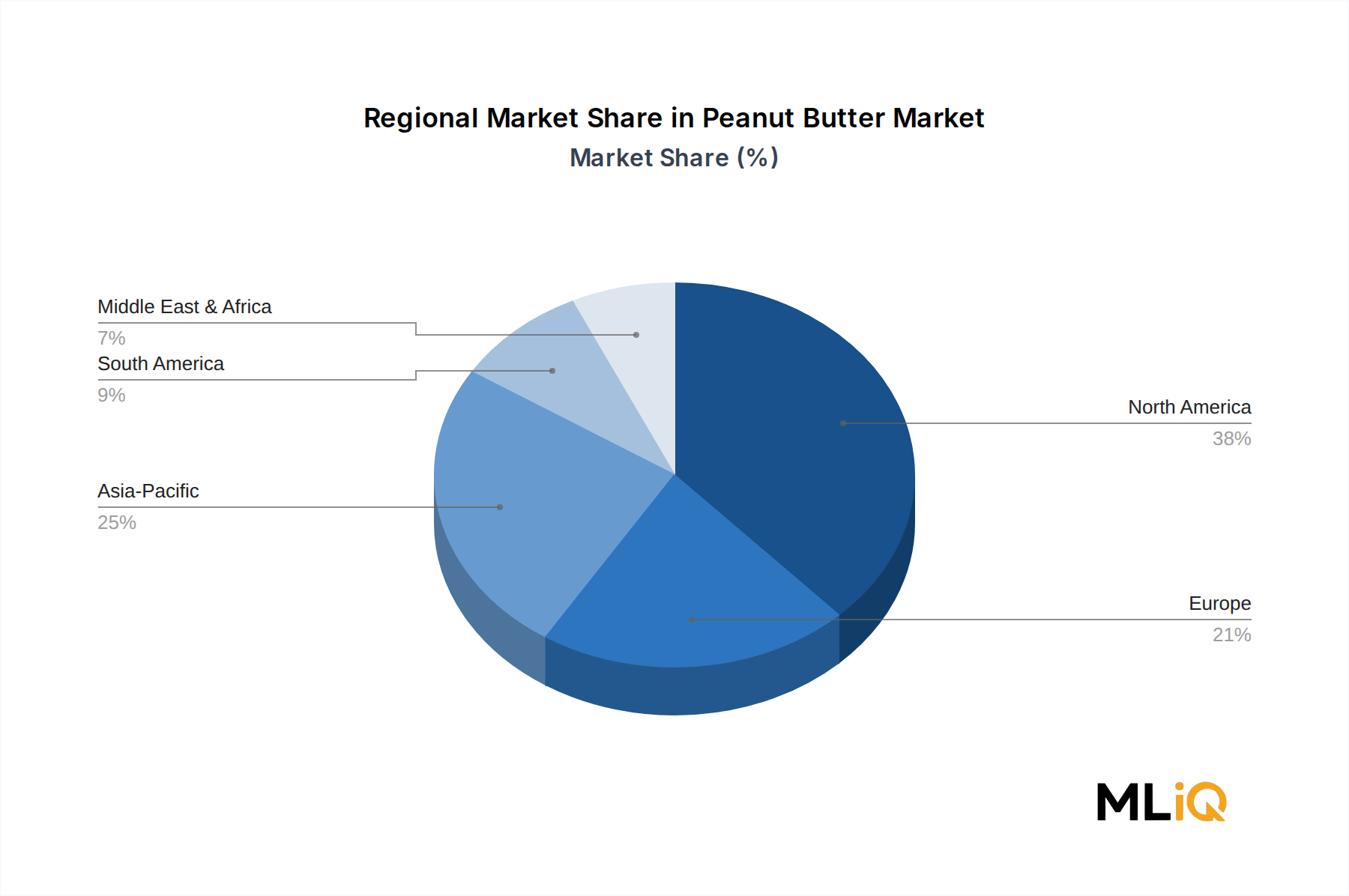

Growth within the smooth sub-segment is expected to be particularly strong in Asia Pacific, where first-time peanut butter consumers — especially in China, India, and ASEAN markets — tend to begin with smooth varieties before potentially migrating to crunchy or specialty formats. This consumer adoption curve provides a sustained demand pipeline for the smooth sub-segment well into the 2030s.