Heavy Commercial Vehicle Dominance in the Retread Tire Market

Among all vehicle type segments analyzed within the retread tire market, heavy commercial vehicles (HCVs) represent by far the largest revenue-generating category. This dominance is not incidental—it is structurally embedded in the economics, logistics, and regulatory context that surround HCV fleet operations globally.

Heavy commercial vehicles, including Class 7 and Class 8 trucks, articulated lorries, intercity coaches, and mining dump trucks, operate under tire cost dynamics that are fundamentally different from passenger vehicles. A single long-haul tractor-trailer unit may consume 18 or more tires at a time, with each tire requiring replacement after approximately 100,000–150,000 miles of service life under standard conditions. At average market prices for premium new tires, fleet procurement costs per vehicle are substantial. Retreading offers fleet managers a proven mechanism to extend casing utility across two or more retread cycles, dramatically reducing per-mile tire expenditure.

The financial calculus is particularly compelling in markets with high per-kilometer freight rates and volatile fuel prices. In North America, where the trucking industry annually consumes tens of millions of tires, the share of retreads in total commercial tire consumption consistently exceeds 40% in certain categories. Major truckload carriers—including subsidiaries of global logistics conglomerates—have institutionalized retreading programs within their maintenance and procurement protocols.

Section width and rim size segmentation within the HCV category further illustrates this dominance. Tires with section widths greater than 230 mm and rim sizes in the 19–21 inch and above-21-inch brackets are disproportionately represented in HCV fleets and also command the highest retread margins, given the higher base cost of the original casings. The investment in maintaining and retreading wide-base single tires—a growing configuration in North American and European long-haul applications—has created a specialized premium sub-segment within the broader HCV retreading market.

The dominance of HCVs is also reinforced by the maturity and density of the commercial retreading supply chain. Unlike the fragmented and informal retreading networks that service passenger car tires in certain developing markets, HCV retreading is served by a well-developed ecosystem of authorized retreaders, casing brokers, and OEM-affiliated programs. Companies such as Bridgestone Corporation, Michelin (through its TreadWear and Bandag networks), and Goodyear Tire and Rubber Co. have established franchise retreading models that standardize compound application, tread pattern matching, and quality certification specifically for the HCV segment.

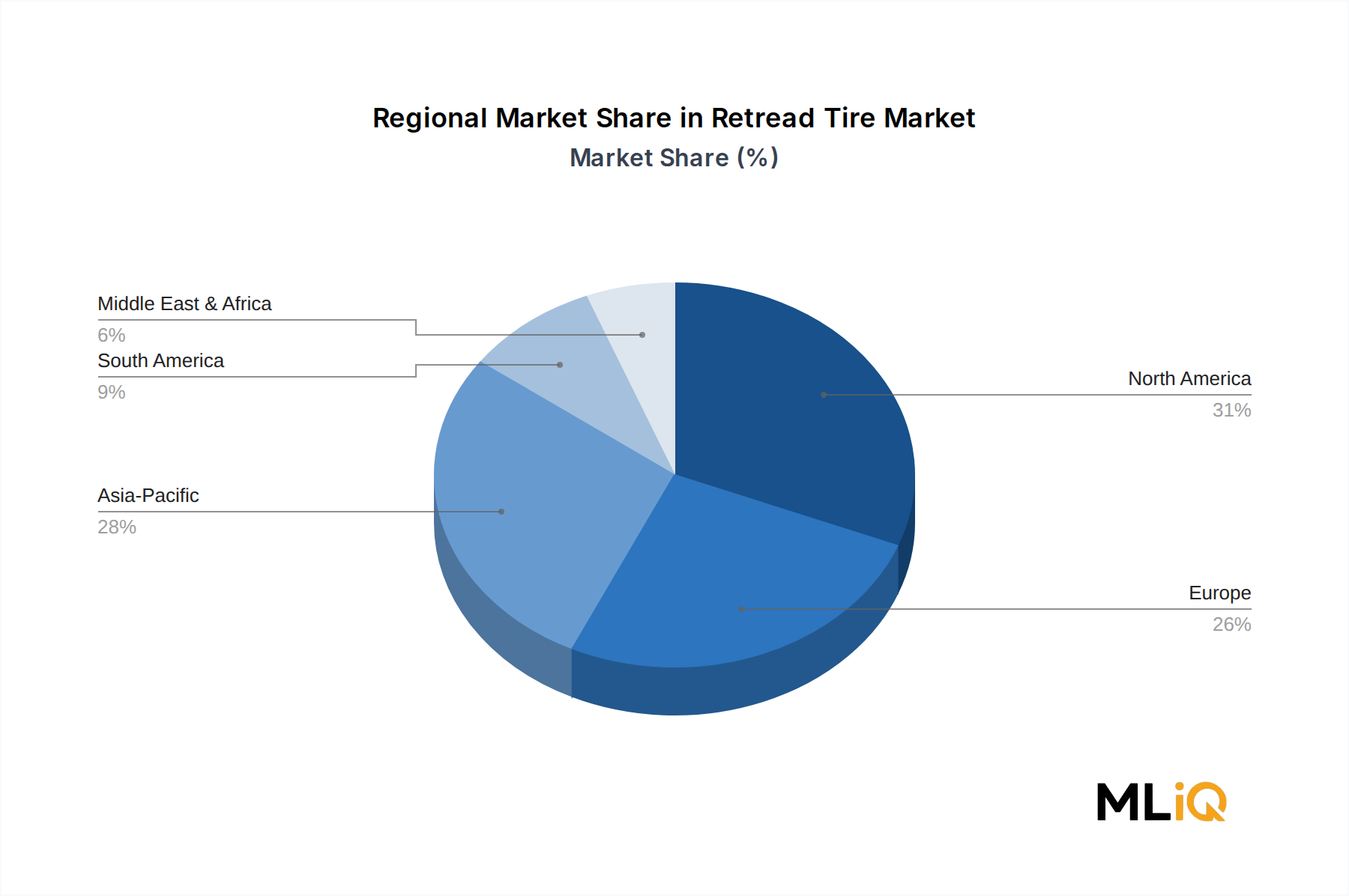

From a geographic dimension, the HCV sub-segment is strongest in North America, Western Europe, and rapidly growing in South and Southeast Asia, where infrastructure development is driving commercial freight activity. In markets like India and Brazil, the informal retreading sector serves a significant portion of HCV demand, though formalization trends are gradually bringing these volumes into reportable market channels.

The HCV segment's share is not merely consolidating—it is incrementally growing as fleet sizes expand and as sustainability-focused procurement mandates from large shippers and logistics buyers begin to specify or prefer retreaded content in fleet tire inventories. This regulatory and corporate governance push is expected to ensure that HCV retreading maintains its dominant position through the forecast period, even as adjacent segments such as light commercial vehicles begin to attract increased attention from retreaders looking to diversify their customer bases.