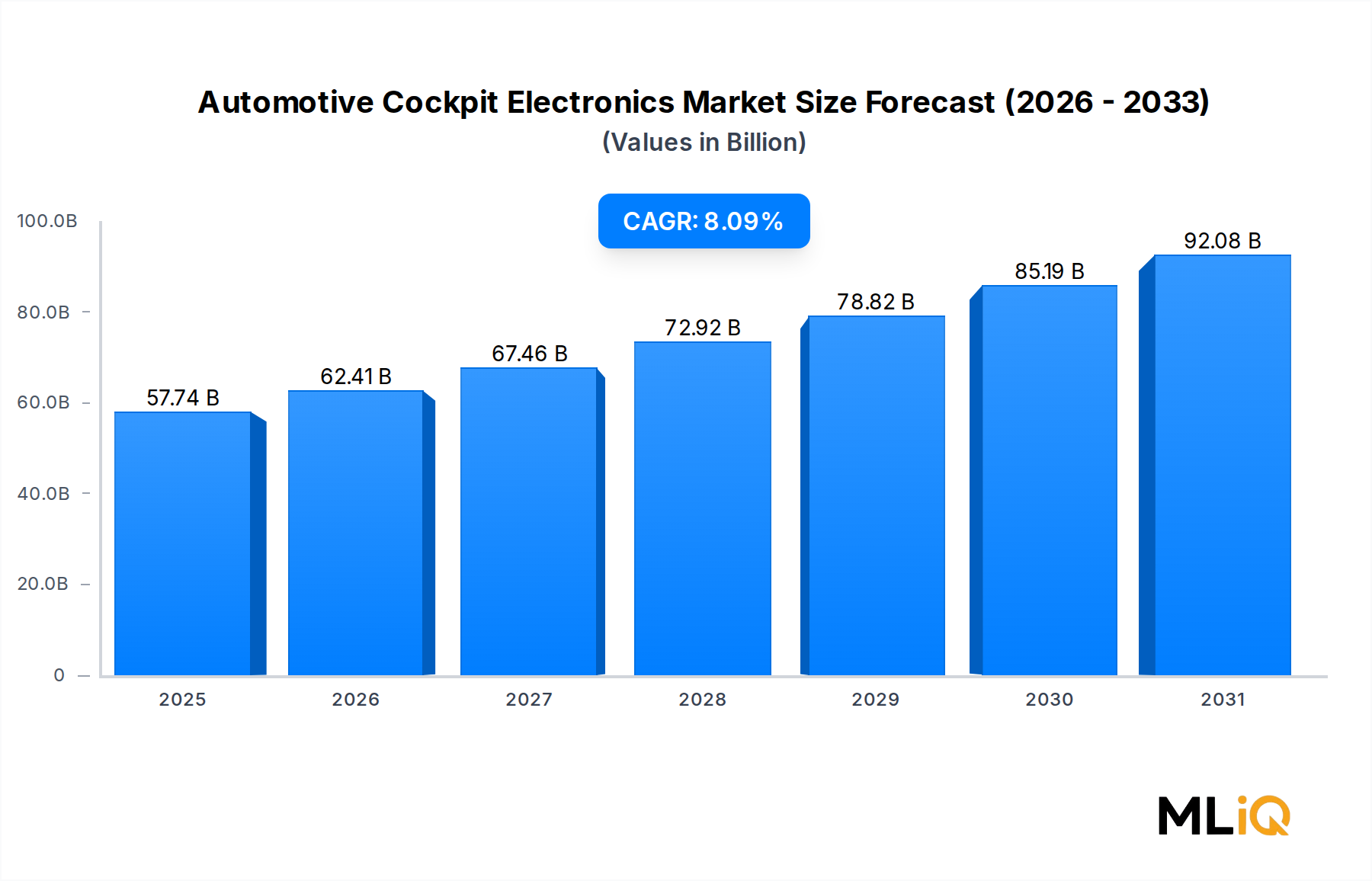

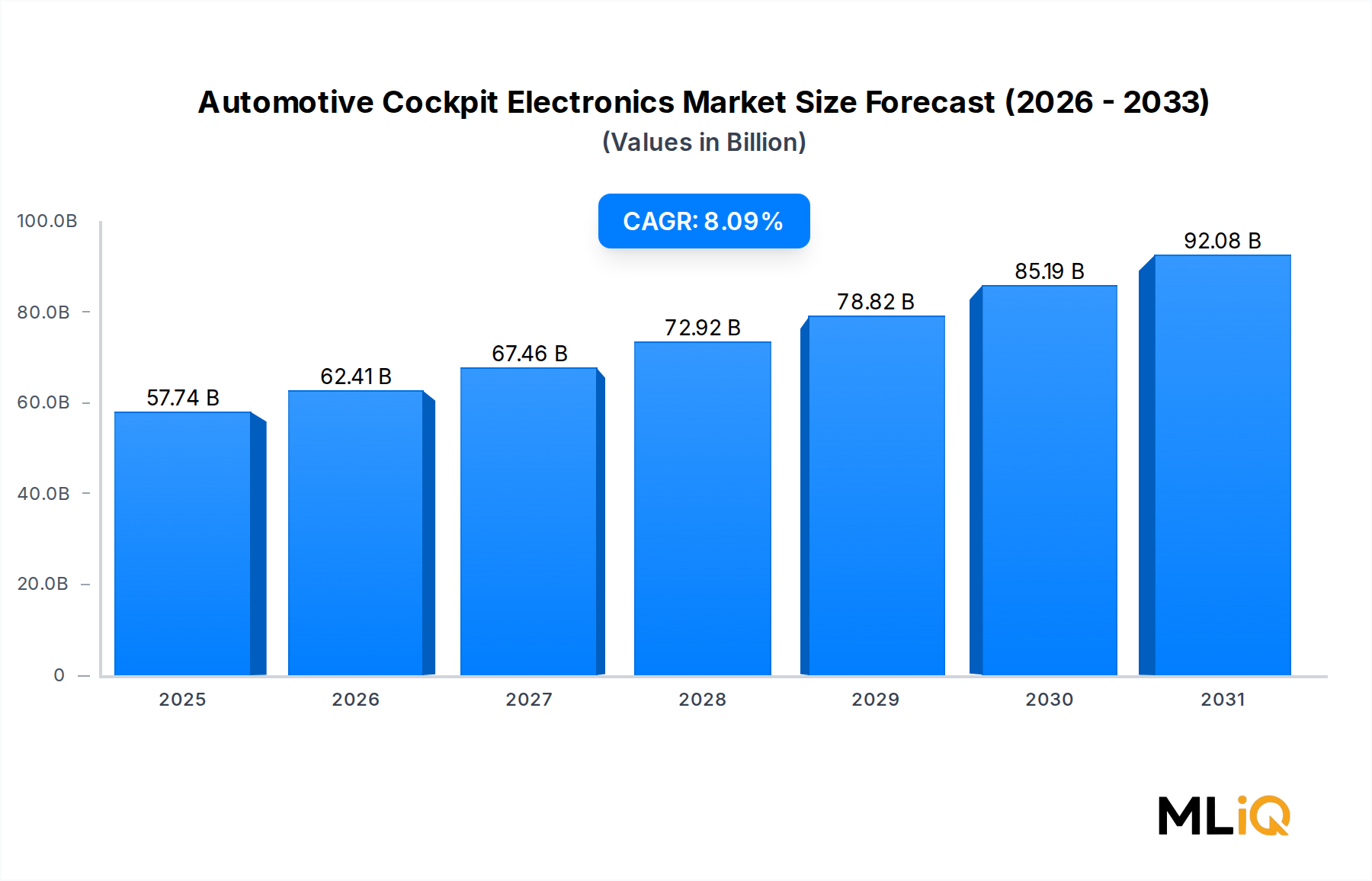

Head-Up Display Dominance in the Automotive Cockpit Electronics Market

Among all product sub-segments tracked within the Automotive Cockpit Electronics Market, the Head-up Display (HUD) category has emerged as the single largest revenue contributor on a unit-value-weighted basis, and its share is actively growing rather than consolidating at a plateau. The structural reasons for this dominance are multifaceted and mutually reinforcing.

From a safety-regulatory standpoint, HUD systems directly address distracted-driving legislation gaining traction across the European Union and several North American state jurisdictions. By projecting speed, navigation arrows, collision warnings, and lane-departure alerts into the driver's forward line of sight, HUD technology reduces eye-off-road time by an estimated 30–40% compared with traditional instrument clusters, a statistic that regulators and fleet safety managers find compelling. This safety narrative elevates HUD from an aspirational luxury feature to a near-mandatory safety technology in the eyes of regulatory bodies, ensuring that OEM procurement decisions increasingly favor broader HUD fitment across vehicle lines rather than restricting it to flagship trims.

Technologically, the segment is undergoing a rapid transition from conventional combiner-type HUD systems to full-windshield augmented-reality (AR) HUDs that overlay directional cues, pedestrian-detection highlights, and hazard zones directly onto the physical road scene. AR-HUD systems require substantially more sophisticated optical path design, waveguide engineering, and image-processing compute, all of which carry significantly higher average selling prices than first-generation combiner units. This premiumization of the HUD stack is the primary engine driving revenue share expansion within the broader cockpit electronics domain.

Key players driving segment leadership include Visteon Corporation, which has deployed its SmartCore cockpit domain controller architecture across multiple global OEM programs with integrated HUD output pipelines. Continental AG has likewise invested heavily in its AR-HUD roadmap, announcing series production programs with European OEMs for systems capable of projecting a virtual image plane at distances exceeding 10 meters. Nippon-Seiki Co. Ltd maintains a strong position in the Japanese domestic market and supplies HUD modules to several volume OEM platforms across Asia Pacific. Harman International, leveraging its parent company Samsung's display expertise, has developed software-defined HUD rendering engines that support real-time mapping data integration from HERE Technologies and TomTom.

The competitive dynamics within the HUD sub-segment are also being shaped by the entry of specialist optics firms and LiDAR-adjacent companies that possess deep competencies in photonics, micro-display fabrication, and waveguide coating. These entrants are challenging Tier 1 incumbents on image quality benchmarks and pushing HUD luminance levels toward 15,000 nits or more to ensure daytime readability without compromising driver comfort.

From a vehicle-type perspective, passenger cars currently account for the majority of HUD revenue, driven by premium and mid-premium segment adoption. However, commercial vehicle OEMs are accelerating HUD integration into long-haul truck cabins as fleet telematics data, route optimization overlays, and driver fatigue alerts become operationally indispensable for logistics operators managing total cost of ownership.

The Automotive Head-up Display Market is closely intertwined with the broader cockpit electronics ecosystem because HUD system performance is increasingly dependent on data fusion from cameras, radar, GPS, and high-definition maps — inputs that are managed by the same domain controller serving the digital instrument cluster and infotainment screen. This integration dependency creates a strong architectural lock-in effect that benefits suppliers capable of delivering full cockpit domain solutions rather than standalone HUD modules.