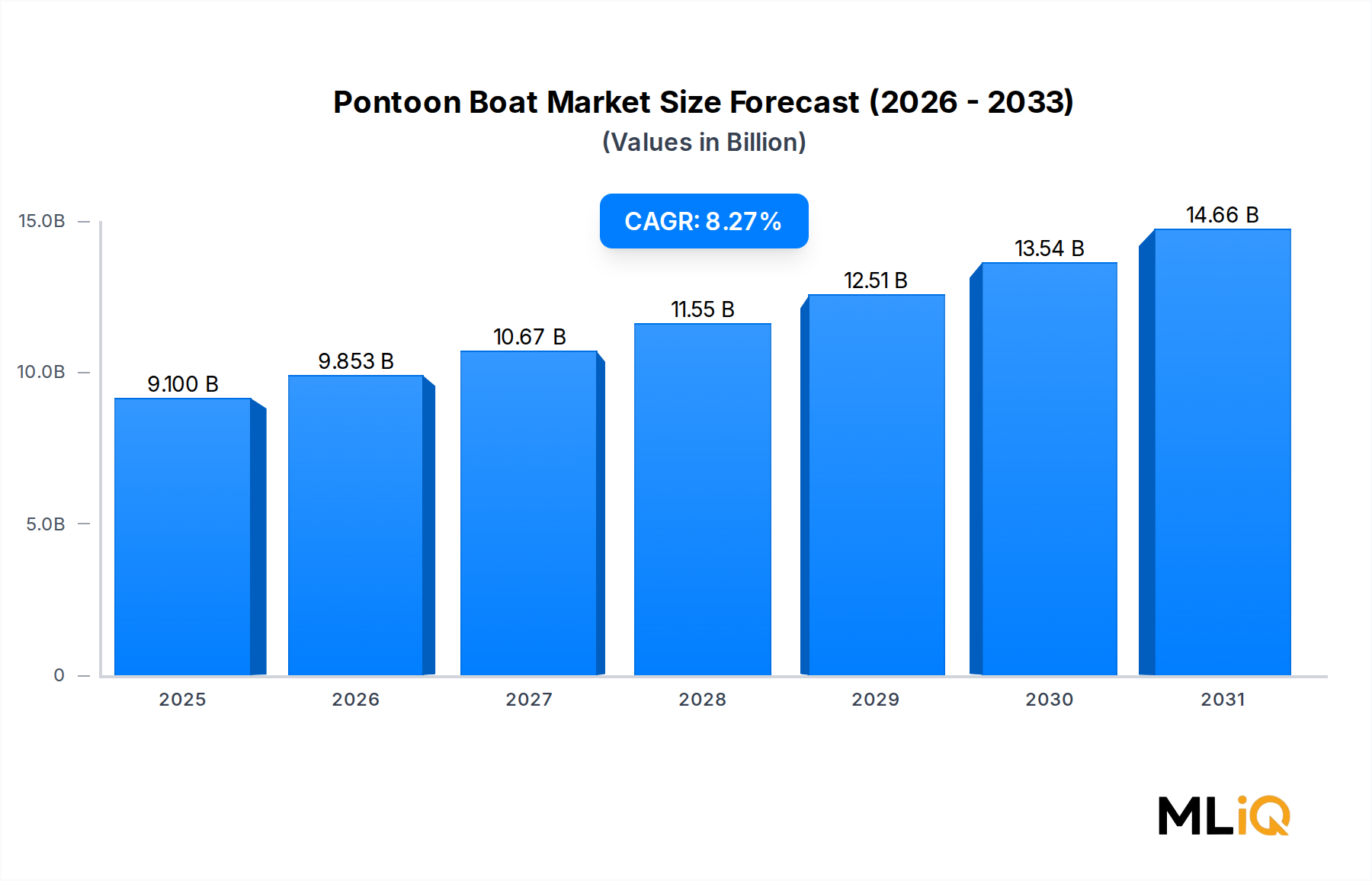

Recreational Segment Dominance in the Pontoon Boat Market

The recreational application segment unequivocally anchors the Pontoon Boat Market, accounting for an estimated 58–62% of total global revenue in 2025. This dominance is structural rather than cyclical, rooted in the fundamental positioning of pontoon boats as versatile, family-friendly watercraft optimized for calm inland waters, lakes, and slow-moving rivers. Unlike center-console fishing boats or high-performance runabouts, pontoon platforms offer a broad deck, customizable seating configurations, and an accessible boarding experience that appeals to multi-generational user groups — from young families to retirees.

The recreational segment's strength is amplified by several reinforcing dynamics. Waterfront and lake-adjacent property markets remain robust across the United States, Canada, and parts of Northern Europe, and homeowners with water access are statistically far more likely to purchase a pontoon boat than the general population. According to National Marine Manufacturers Association data, pontoon boats have been the best-selling boat type by unit volume in the United States for several consecutive years, underscoring their mainstream recreational appeal.

Premiumization is a defining trend within the recreational segment. Entry-level pontoon boats in the sub-$30,000 range continue to attract first-time buyers, but the fastest revenue growth is occurring in the $60,000–$120,000 luxury tier, where manufacturers compete on features such as built-in wet bars, premium sound systems, LED lighting packages, hydraulic lifting platforms, and high-end upholstery. This premiumization trend has materially elevated average selling prices (ASPs) and expanded gross margins for OEMs that successfully execute upmarket positioning.

Key players dominating the recreational segment include Polaris Industries through its Bennington and Godfrey brands, Avalon Pontoon Boats with its emphasis on hand-crafted premium interiors, and Brunswick Corporation's Sea Ray and Lund divisions. White River Marine Group, operating as the exclusive boat brand supplier for Bass Pro Shops and Cabela's, also commands significant volume through its vertically integrated retail distribution model.

The segment's share is not merely holding — it is consolidating. Fishing-configured pontoon boats (a hybrid sub-category) are increasingly cannibalizing traditional bass boat demand, as anglers recognize the stability and livability advantages of pontoon platforms for multi-person fishing excursions. Sports applications such as watersports towing are also being absorbed into the recreational segment as manufacturers integrate tow pylons and wake-enhancing features into recreational-grade models.

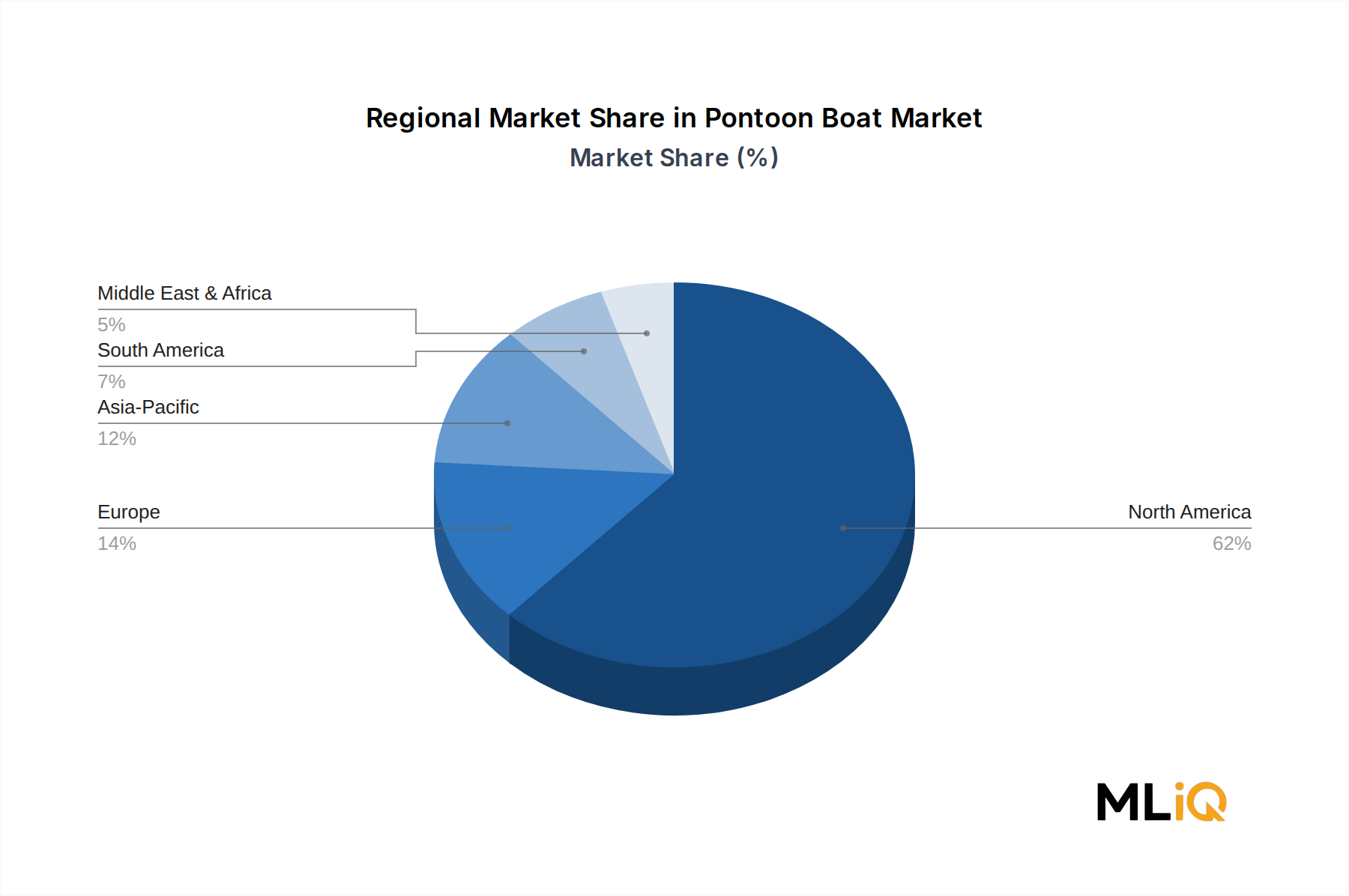

Geographically, the recreational segment is most concentrated in North America (United States and Canada), which accounts for approximately 72% of global recreational pontoon boat sales. European demand is nascent but growing, particularly in the Nordic countries and around large inland lakes in Germany and France. The Asia Pacific region presents the most significant long-term opportunity, as rising middle-class affluence in countries like China, India, and Australia drives first-generation adoption of recreational watercraft.

Segment consolidation risk is low in the near term. The structural advantages of pontoon design — stability, deck space, customizability, and relatively low operating cost — position recreational pontoon boating as a durable leisure category that is not easily displaced by competing watercraft typologies. OEMs with strong dealer networks and established brand equity are well-positioned to capture incremental share as the market expands.