1. What are the major growth drivers for the Online Sports Betting Market market?

Factors such as are projected to boost the Online Sports Betting Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

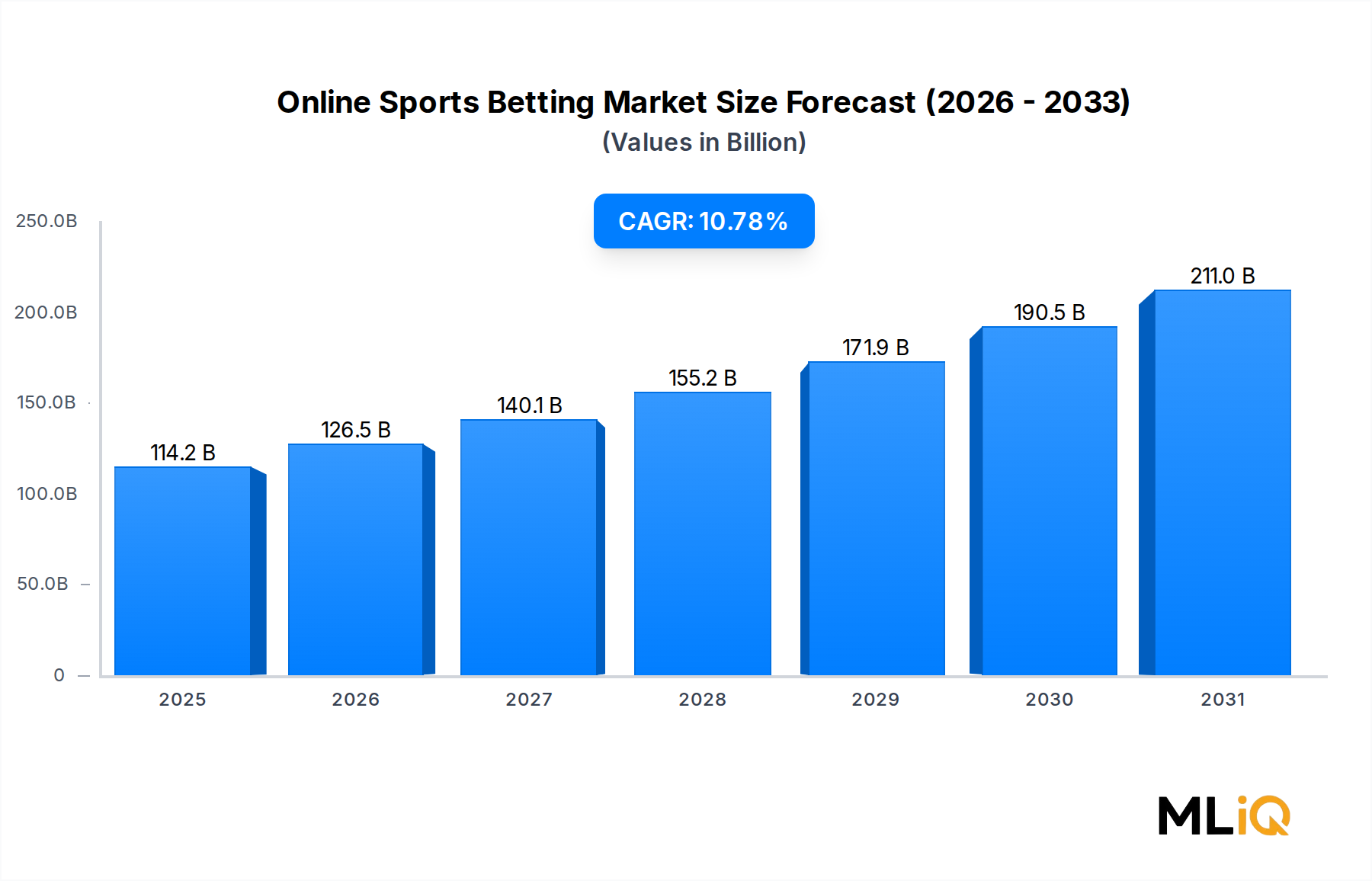

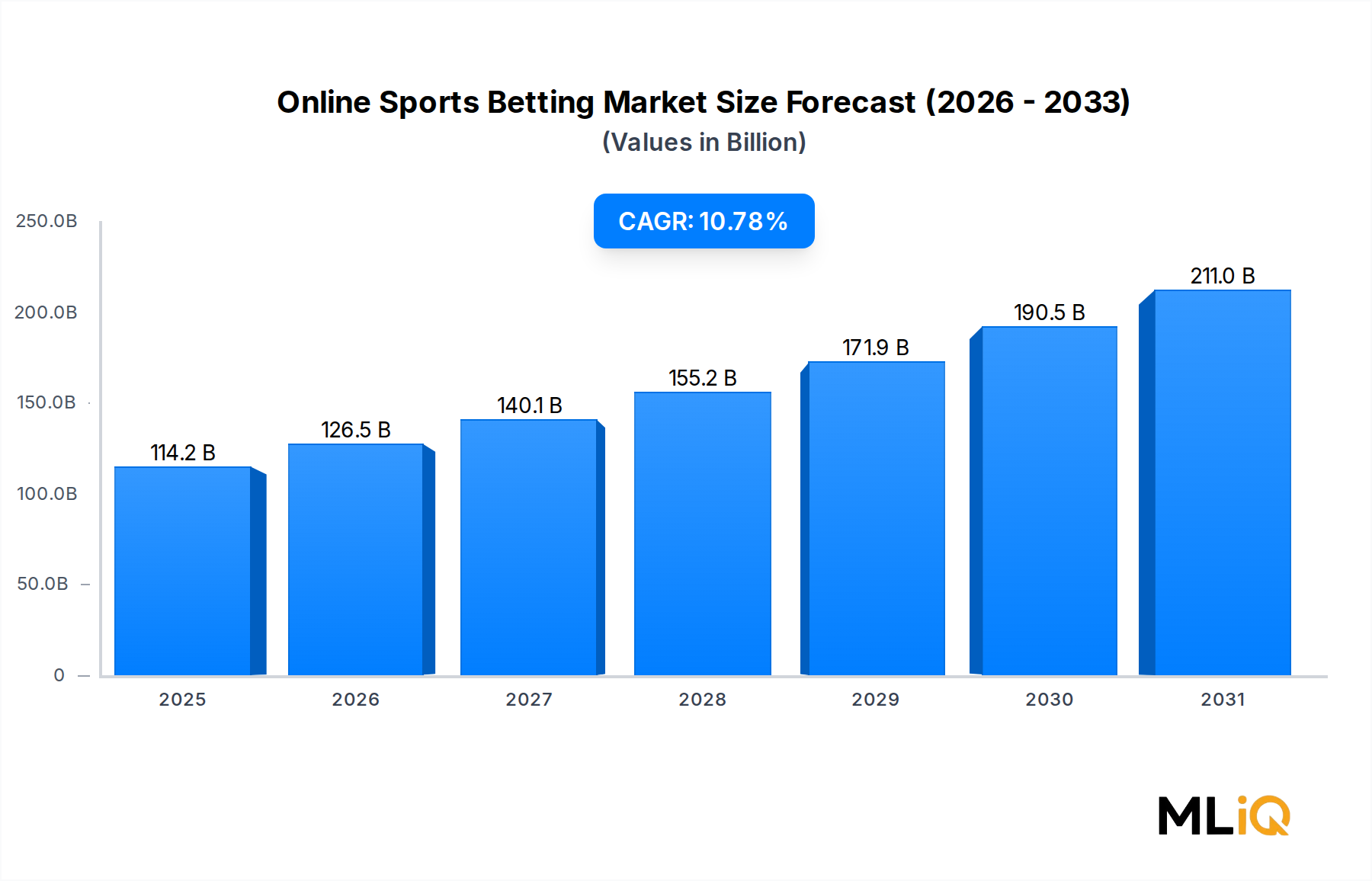

The global Online Sports Betting Market is valued at $114.15 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 10.78% through 2033, reaching an estimated valuation exceeding $260 billion by the end of the forecast period. This robust expansion is underpinned by a confluence of regulatory liberalization, accelerating smartphone penetration, and an unprecedented surge in live-event streaming consumption that has redefined how bettors engage with sports content globally.

Key demand drivers include the progressive legalization of sports wagering across North America following the 2018 U.S. Supreme Court ruling that struck down the Professional and Amateur Sports Protection Act (PASPA), effectively opening a multi-hundred-billion-dollar addressable market. Since that watershed moment, more than 35 U.S. states have enacted sports betting legislation, generating billions in handle and tax revenues annually. Simultaneously, digital payment infrastructure modernization has reduced friction in deposit-and-withdrawal cycles, improving bettor retention and lifetime value metrics.

From a macro perspective, the proliferation of 5G connectivity is enabling real-time, low-latency in-play wagering experiences that were previously constrained by network bottlenecks. Operators are capitalizing on this by expanding live betting catalogs, with in-play betting now representing over 40% of total wagering handle on major platforms. The integration of machine learning-driven odds compilation and dynamic pricing models has further enhanced operator margins while simultaneously improving market depth and bettor utility.

The competitive landscape is being reshaped by consolidation, with large-cap operators executing transformative M&A strategies to acquire proprietary technology stacks, data rights, and media distribution assets. The intersection of sports media and betting, exemplified by partnerships between leagues, broadcasters, and operators, is creating powerful customer acquisition channels that traditional advertising cannot replicate.

Looking forward, the Online Sports Betting Market is positioned for durable, compounding growth as emerging markets in Asia Pacific, Latin America, and Africa progressively liberalize their regulatory frameworks. The convergence of betting with interactive entertainment formats — including e-sports, virtual sports, and gamified micro-betting — is broadening the addressable demographic base beyond traditional sports bettors, drawing in digitally native, younger consumers who demand immersive, data-rich wagering experiences. The outlook through 2033 remains strongly constructive, with technology innovation serving as the primary lever for both top-line revenue growth and margin expansion across the value chain.

Within the Online Sports Betting Market, the mobile platform segment has emerged as the unambiguous revenue leader, accounting for an estimated 65% or more of total gross gaming revenue (GGR) globally as of 2025. This dominance reflects a structural behavioral shift among bettors who increasingly prefer the convenience, immediacy, and personalization afforded by smartphone applications over desktop or retail interfaces. The mobile segment's share has grown steadily from approximately 40% in 2018 to its current commanding position, driven by improvements in app design, biometric authentication, and location-based services.

Several factors underpin mobile's sustained supremacy. First, smartphone adoption rates have crossed 85% in key markets including the United Kingdom, Australia, and the United States, creating vast addressable audiences with always-on internet access. Second, operating system-level improvements — particularly around push notification delivery and widget-based live score integrations — have lowered the engagement threshold, enabling operators to reach bettors at contextually relevant moments during live sporting events. Third, the removal of betting applications from app store restrictions in regulated markets has dramatically expanded organic discovery and download volumes.

From a product architecture standpoint, mobile-first operators have invested heavily in native iOS and Android applications that leverage device-specific capabilities: haptic feedback for bet confirmation, augmented reality overlays for stadium-based experiences, and voice-activated bet placement via smart assistant integration. These features have contributed to measurably higher session frequency and bet-per-session metrics compared to desktop equivalents.

Flutter Entertainment Plc, operator of FanDuel and Paddy Power, has arguably set the industry benchmark for mobile product excellence, with its FanDuel application consistently ranking among the top-grossing sports applications in the U.S. App Store. Bet365, widely regarded as the global benchmark for mobile sports betting UX, processes the majority of its enormous betting volume — reportedly exceeding $70 billion in annual handle — through mobile channels. DraftKings, though not listed among the primary companies in this report, has also been a significant mobile-native contributor in the North American context.

The offline segment, conversely, is experiencing structural contraction as retail sportsbook economics are challenged by high fixed costs, geographic constraints, and the inability to offer in-play betting depth comparable to digital platforms. Regulatory requirements in certain jurisdictions mandate a retail presence as a condition of digital licensing, sustaining some offline volume, but the long-term trajectory clearly favors mobile consolidation.

The device outlook segmentation also reveals meaningful differentiation in bettor demographics. Desktop users tend to exhibit higher average bet sizes and longer session durations, skewing toward high-value recreational and professional bettors who prefer larger screen real estate for multi-market analysis. Mobile users, by contrast, demonstrate higher bet frequency with lower average stakes, reflecting casual, event-driven wagering behavior. Operators are architecting differentiated product experiences to serve both cohorts without cannibalizing one another, with cross-device continuity — including synchronized bet slips, shared wallet balances, and unified account histories — becoming a baseline product expectation rather than a premium feature.

The trajectory for the mobile segment suggests further share consolidation through 2033, with progressive web application (PWA) technology enabling operators to bypass app store distribution entirely in certain markets, reducing customer acquisition costs and expanding reach into markets where native app installations face regulatory or technical barriers.

The growth trajectory of the Online Sports Betting Market is governed by several high-conviction drivers and countervailing constraints that collectively define the risk-reward profile for operators and investors.

Regulatory expansion represents the most powerful structural driver. As of 2025, more than 100 jurisdictions globally have enacted some form of legal sports betting framework, compared to fewer than 40 in 2015. Each new regulated market creates immediate addressable revenue opportunity while simultaneously legitimizing the sector for institutional capital. The United States alone has generated over $220 billion in cumulative betting handle since PASPA's repeal, with annual GGR exceeding $11 billion by 2024. Brazil's 2023 sports betting legalization — covering a population of 215 million — represents perhaps the single largest near-term market expansion event globally.

Smartphone and internet penetration growth in Asia Pacific and Sub-Saharan Africa is a secondary structural driver. Mobile internet user counts in these regions are projected to grow by hundreds of millions over the forecast period, each representing a potential new bettor. The Mobile Gambling Market is a direct beneficiary of this infrastructure buildout, and synergies with the Online Sports Betting Market are substantial.

In-play betting product innovation is a demand-side driver with quantifiable impact. Operators offering comprehensive live betting catalogs report 25–35% higher GGR per active user compared to pre-match-only competitors, according to industry benchmarking data. The expansion of live betting across previously underserved sports — including cricket, tennis, and e-sports — broadens engagement windows and bet frequency.

Constraints include problem gambling regulation and responsible gaming compliance costs, which have increased materially in the United Kingdom and Australia. The UK Gambling Commission's affordability checks and stake limit proposals have suppressed high-value bettor activity, contributing to revenue headwinds for operators with heavy U.K. exposure. Cybersecurity and fraud risks represent an operational constraint, with account takeover fraud and bonus abuse imposing losses estimated at 1–3% of GGR industry-wide. Payment processing challenges in markets lacking established fintech infrastructure add friction that elevates churn rates among newly acquired customers.

Webis Holdings Plc: A smaller-cap operator with pari-mutuel and fixed-odds wagering exposure, primarily serving the U.S. and Isle of Man markets. The company has pursued niche positioning in horse racing-linked wagering products and totalisator pool services.

The Stars Group Inc.: A major online gaming conglomerate that operated PokerStars and BetStars before its acquisition by Flutter Entertainment in 2020. Prior to consolidation, it was one of the largest publicly traded online gaming companies by revenue, with significant sports betting operations across Europe and Australia.

888 Holdings Plc: A diversified online gambling operator with significant sports betting, casino, and poker verticals. The company completed its transformative acquisition of William Hill's non-U.S. operations in 2022, dramatically expanding its scale and geographic footprint across regulated European markets.

Sportech Plc: A technology and wagering solutions provider focused on football pools, pari-mutuel systems, and licensed gaming venues. Sportech differentiates through B2B technology licensing rather than direct consumer-facing operations, serving operators and governments.

Flutter Entertainment Plc: The largest online sports betting and gaming group globally by revenue, operating FanDuel, Paddy Power, Betfair, Sky Betting & Gaming, and PokerStars. Flutter's U.S. subsidiary FanDuel holds approximately 50% market share in American online sports betting GGR, making it the dominant force in the world's fastest-growing regulated market.

Churchill Downs Inc.: Primarily known for its iconic Kentucky Derby and horse racing assets, Churchill Downs has aggressively expanded into digital wagering through its TwinSpires platform and strategic investments in regional gaming properties. The company leverages its racing infrastructure as a differentiated customer acquisition channel.

GVC Holdings Plc: Now rebranded as Entain Plc, this operator owns Ladbrokes, Coral, bwin, and Sportingbet, among other brands. Entain operates one of the largest omni-channel betting networks globally and has been at the center of major M&A speculation including a proposed acquisition approach from MGM Resorts International.

Bet365: A privately held operator widely regarded as the world's largest online sports betting company by handle, with a reported $70+ billion annual wagering volume. Bet365's proprietary technology stack, in-play betting depth, and global product consistency set the competitive benchmark against which public competitors are often measured.

Kindred Group Plc: A Nordic-headquartered multi-brand operator running Unibet, 32Red, and Maria Casino, among others. Kindred has been a vocal advocate for responsible gambling leadership and has set public targets to derive 0% of revenue from harmful gambling by 2023, influencing industry-wide ESG positioning.

William Hill Plc: One of the most historically significant British bookmakers, William Hill was acquired by Caesars Entertainment in 2021. The U.K. and international digital operations were subsequently sold to 888 Holdings, while Caesars retained the U.S. digital and retail sports betting assets under the Caesars Sportsbook brand.

March 2023: Brazil enacted its sports betting regulatory framework, opening one of the world's largest untapped markets to licensed operators and triggering a wave of market entry applications from global operators including Bet365, Flutter Entertainment, and Kindred Group.

June 2023: 888 Holdings Plc completed the integration of William Hill's international digital assets, creating a combined entity with over $2 billion in annual revenue and presence in more than 15 regulated markets across Europe and beyond.

September 2023: Flutter Entertainment Plc listed its U.S. operations via a secondary listing on the New York Stock Exchange, providing FanDuel with enhanced capital markets access and validating the multi-billion-dollar valuation of the U.S. sports betting segment.

January 2024: The United Kingdom Gambling Commission published updated affordability check consultation proposals, prompting significant operator commentary and foreshadowing potential GGR headwinds for U.K.-focused operators exceeding £500 million annually.

April 2024: Entain Plc (formerly GVC Holdings) announced a strategic partnership with a leading U.S. media conglomerate to integrate branded betting content within live sports broadcasts, accelerating the convergence of media and wagering distribution.

October 2024: North Carolina launched legal online sports betting, adding a 10-million-plus adult population to the U.S. regulated market and generating over $200 million in handle within the first month of operation.

February 2025: Several Asian Pacific jurisdictions, including Thailand and the Philippines, advanced legislative frameworks for licensed online sports wagering, signaling a new wave of Asia Pacific market liberalization that could unlock $15–20 billion in incremental GGR opportunity by 2030.

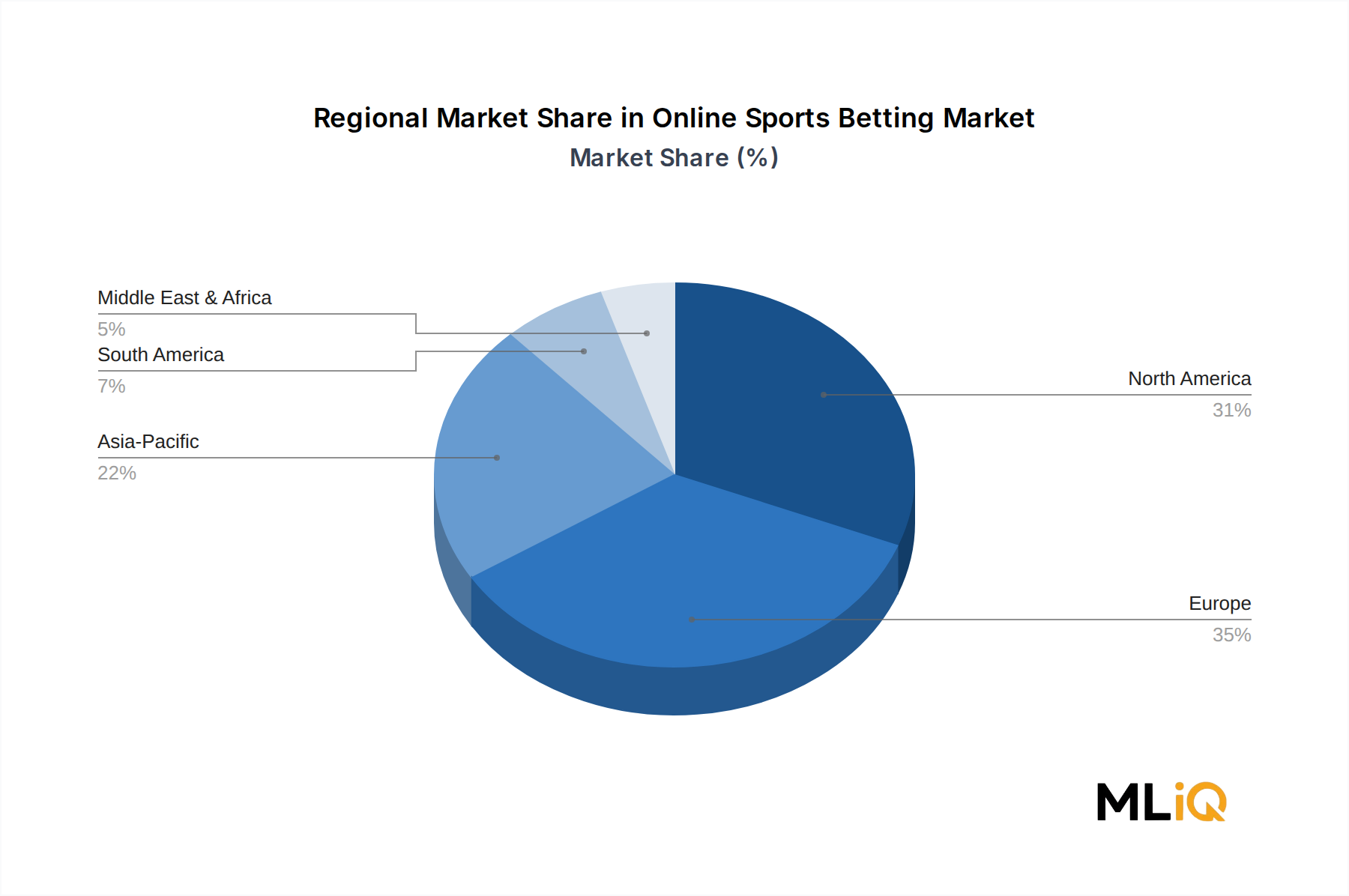

The Online Sports Betting Market exhibits pronounced regional heterogeneity in terms of market maturity, regulatory posture, growth velocity, and bettor behavior, necessitating differentiated strategic approaches for global operators.

Europe represents the most mature regional market, accounting for an estimated 38–42% of global GGR. The United Kingdom remains the single largest national market, with the UK Gambling Commission reporting licensed operator GGR exceeding £6.9 billion in sports betting for the most recent annual period. Germany, France, Spain, and Italy collectively contribute substantial additional volume, though regulatory fragmentation and tax differentials across jurisdictions create operational complexity. European market CAGR through 2033 is projected at approximately 5–6%, reflecting a mature base effect and increasing regulatory cost headwinds.

North America is the fastest-growing major regional market, driven almost entirely by the progressive U.S. state-by-state legalization cycle initiated in 2018. The region's CAGR is estimated at 17–20% through 2028, moderating thereafter as market penetration matures. The U.S. sports betting market generated over $11 billion in GGR in 2024, with projections suggesting a $20+ billion annual GGR market by 2030 as remaining population-dense states including California and Texas move toward legalization. Canada's Ontario market, launched in 2022, has rapidly attracted over 30 licensed operators and is tracking toward $1+ billion in annual GGR.

Asia Pacific is the highest-potential long-term regional opportunity, home to approximately 60% of the world's sports bettors on an informal basis. Formal market legalization in the Philippines, Japan (limited to certain sports), and increasingly in Southeast Asian markets is beginning to channel this latent demand into licensed frameworks. Regional CAGR is estimated at 14–16% through 2033, though this figure understates the total opportunity given the magnitude of unregulated activity that will gradually migrate to licensed platforms.

Latin America is experiencing rapid formalization, led by Brazil's landmark 2023 legislation. The region's combined GGR opportunity is estimated at $5–8 billion annually by 2030, with Brazil alone representing 60–70% of regional value. Argentina and Colombia have functional regulated frameworks with growing operator participation. Regional CAGR is estimated at 18–22% through 2030.

Middle East and Africa represents an emerging frontier. While religious and cultural constraints limit penetration across much of the Middle East, South Africa maintains an active licensed betting market, and broader Sub-Saharan Africa — particularly Nigeria, Kenya, and Ghana — is generating substantial mobile betting activity driven by young demographics and deep football engagement. African regional CAGR is estimated at 12–15% through 2033.

The Online Sports Betting Market has been one of the most active arenas for M&A, venture funding, and strategic partnership activity within the broader consumer technology and entertainment sectors over the past three years. Total disclosed transaction value across the sector exceeded $15 billion between 2021 and 2024, reflecting both consolidation among mature operators and growth-stage capital formation around technology enablers.

The most consequential M&A event of the recent cycle was Caesars Entertainment's acquisition of William Hill Plc for approximately $3.7 billion in 2021, which provided Caesars with a scaled digital sports betting platform to compete with Flutter and DraftKings in the U.S. market. The subsequent carve-out and sale of William Hill

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.78% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Online Sports Betting Market market expansion.

Key companies in the market include Webis Holdings Plc, The Stars Group Inc., 888 Holdings Plc, Sportech Plc, Flutter Entertainment Plc, Churchill Downs Inc., GVC Holdings Plc, Bet365, Kindred Group Plc, William Hill Plc.

The market segments include Platform, Type, Sports Type, Device Outlook.

The market size is estimated to be USD 114.15 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Online Sports Betting Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Online Sports Betting Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.