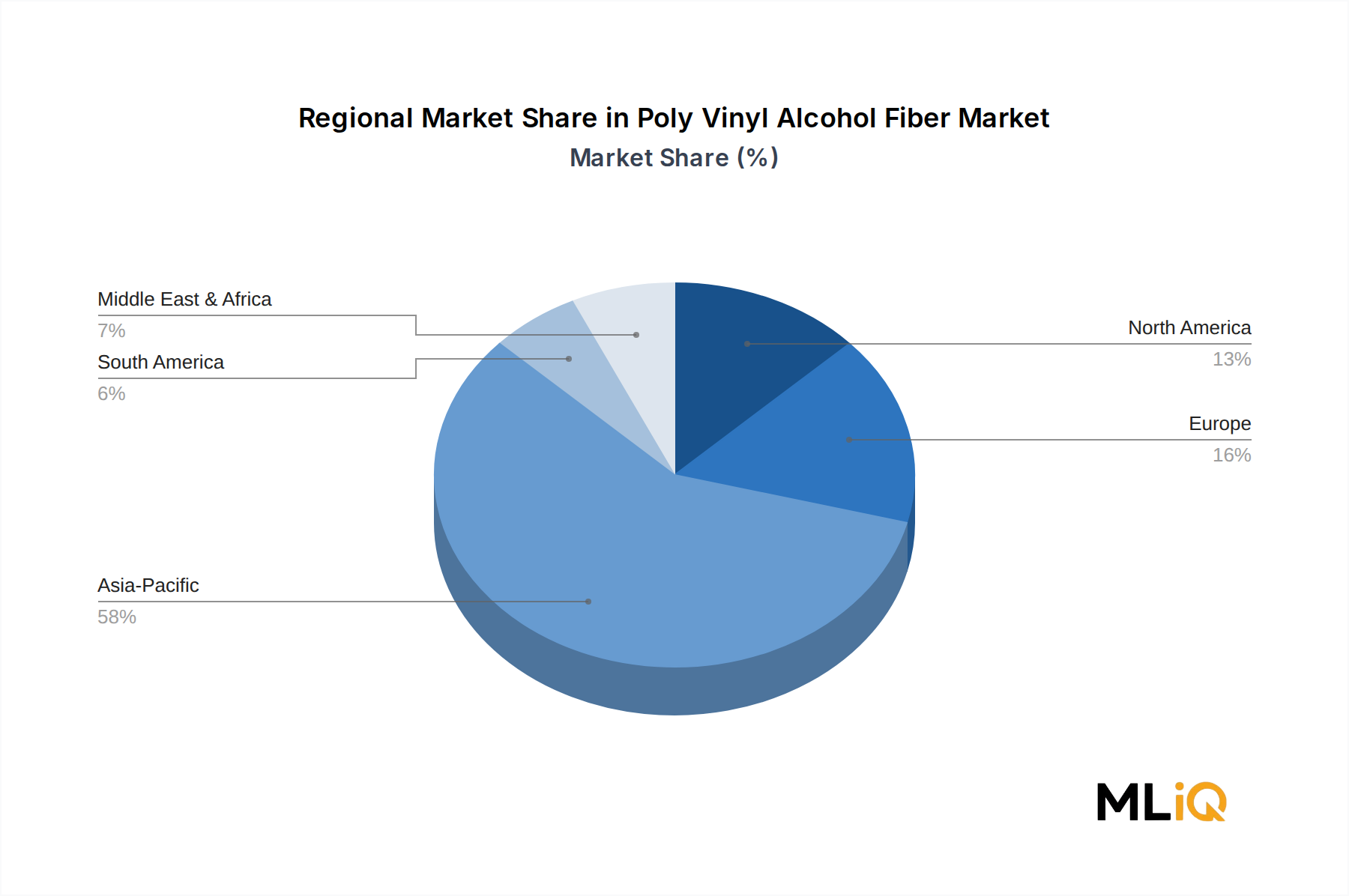

Der Polyvinylalkoholfaser-Markt weist ausgeprägte regionale Unterschiede hinsichtlich Wachstumsgeschwindigkeit, Verbraucherbasis und Endanwendungsmix auf.

Asien-Pazifik ist der dominante regionale Markt und macht im aktuellen Zeitraum schätzungsweise 54–58 % des globalen Marktumsatzes aus. China ist der primäre Verbrauchsknotenpunkt, angetrieben durch massive inländische Infrastrukturinvestitionen, eine etablierte Textilproduktionsbasis und ein vertikal integriertes PVA-Faserproduktionsökosystem. Die Region Asien-Pazifik wächst mit einer regionalen CAGR von etwa 5,1 %, der höchsten unter allen Regionen, unterstützt durch die Urbanisierungs-getriebene Baunachfrage in Indien, Vietnam, Indonesien und dem ASEAN-Block. Indien ist ein aufstrebender Wachstumsmarkt, in dem staatliche Infrastrukturprogramme wie der National Infrastructure Pipeline eine starke inkrementelle Nachfrage generieren.

Nordamerika repräsentiert den zweitgrößten regionalen Markt nach Umsatz, geschätzt auf 18–21 % des globalen Anteils. Die Vereinigten Staaten sind der dominante Ländermarkt innerhalb dieser Region, angetrieben durch die Nachfrage nach spezifikationsgerechten PVA-Fasern in der Infrastruktursanierung, bei Brückenbelägen und SHCC-Anwendungen. Die Region wächst mit einer regionalen CAGR von etwa 3,8 %, was einen reifen, aber technisch anspruchsvollen Markt widerspiegelt, in dem Premium-Faserqualitäten höhere durchschnittliche Verkaufspreise erzielen. Kanada und Mexiko stellen kleinere, aber stetig wachsende Teilmärkte dar, wobei die Bauaktivität der primäre Nachfragetreiber ist.

Europa macht etwa 15–17 % des globalen Marktumsatzes aus, wobei Deutschland, Frankreich und das Vereinigte Königreich die führenden nationalen Märkte sind. Das Wachstum der Region, geschätzt auf eine CAGR von 3,5 %, wird durch strenge Baustandards und die Infrastruktur-Renovierungsagenda des Green Deal unterstützt. Der europäische Markt tendiert aufgrund regulatorischer Qualitätsschwellen zu hochspezifizierten PVA-Faserqualitäten.

Die Region Naher Osten und Afrika ist der am schnellsten wachsende Grenzmarkt innerhalb des Polyvinylalkoholfaser-Marktes, mit einer regionalen CAGR von schätzungsweise 5,6–6,0 %, angetrieben durch groß angelegte Bauprojekte in den GCC-Ländern, insbesondere Saudi-Arabiens Vision 2030-Programm und Megainfrastrukturentwicklungen in den VAE. Südamerika, angeführt von Brasilien und Argentinien, stellt einen kleineren, aber wachsenden Markt dar, der mit einer CAGR von etwa 3,2 % expandiert, primär getrieben durch Bau- und Textilnachfrage.