Institutional and Individual Investor Dominance in the Balanced Funds Market

Within the Balanced Funds Market, the Investor Type segment — specifically the combined Institutional and Individual investor category — represents the primary revenue-generating cohort and commands the largest share of assets under management (AUM) globally. Understanding the interplay between these two investor archetypes is essential to appreciating how the market sustains its high-growth trajectory.

Institutional investors, encompassing pension funds, insurance companies, sovereign wealth funds, endowments, and corporate treasuries, have historically formed the backbone of balanced fund AUM. These entities allocate to balanced funds primarily for liability-driven investment (LDI) purposes, seeking stable risk-adjusted returns that align with long-duration liability profiles. For example, pension funds managing retirement obligations over 20–30 year horizons find balanced funds particularly suited to their actuarial requirements, as the blended equity-debt structure reduces sequence-of-returns risk while maintaining growth potential.

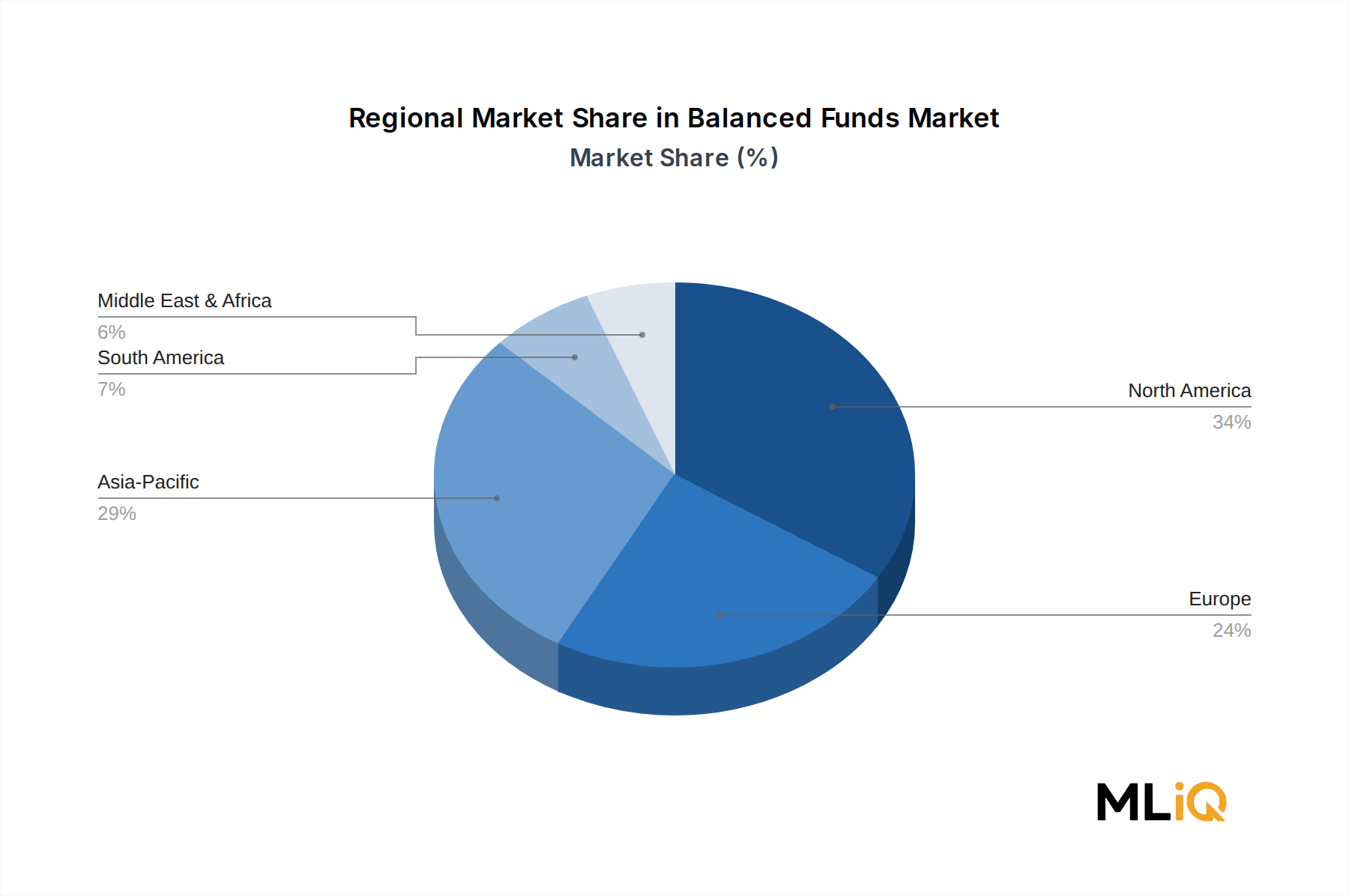

In parallel, the individual investor segment has undergone a transformational expansion, especially in emerging markets across Asia Pacific and Latin America. Rising disposable incomes, increased digital access, and government-led financial inclusion campaigns have onboarded tens of millions of new retail investors into the mutual fund ecosystem. Systematic Investment Plans (SIPs) linked to balanced funds have become a dominant retail investment mechanism in markets such as India, where SIP inflows into hybrid fund categories reached record levels in 2023 and 2024.

The convergence of institutional discipline and retail scalability within the same fund structures is a structural differentiator of the Balanced Funds Market. Fund managers increasingly design multiple share classes within a single balanced fund — institutional class shares with lower expense ratios for large allocators, and retail class shares with value-added advisory features for individual investors — thereby maximizing AUM across both cohorts simultaneously.

Key players capitalizing on this dual-investor dynamic include The Vanguard Group Inc., which leverages its low-cost index-based balanced fund lineup to attract both institutional mandates and self-directed retail investors globally. JPMorgan Chase & Co. offers actively managed balanced funds targeting institutional clients with bespoke ESG integration overlays, while simultaneously distributing standard balanced fund products through its retail banking network. Goldman Sachs has positioned its multi-asset solutions division to serve institutional clients seeking factor-tilted balanced fund exposures.

The dominance of the Institutional and Individual investor segment is further reinforced by tax-advantaged account structures in key markets. In the United States, 401(k) plans and Individual Retirement Accounts (IRAs) channel enormous capital flows into balanced funds as default investment options. Canada's Registered Retirement Savings Plan (RRSP) ecosystem similarly funnels individual savings into hybrid fund vehicles managed by institutions such as Canada Life Assurance Company and Scotiabank.

The segment's share is not merely consolidating — it is actively expanding, driven by demographic tailwinds, digital onboarding, and the structural shift from defined-benefit to defined-contribution retirement systems globally. This transition places the investment decision — and consequently, the selection of balanced funds — directly in the hands of individual investors, even while institutional frameworks govern the product manufacturing and regulatory compliance landscape.

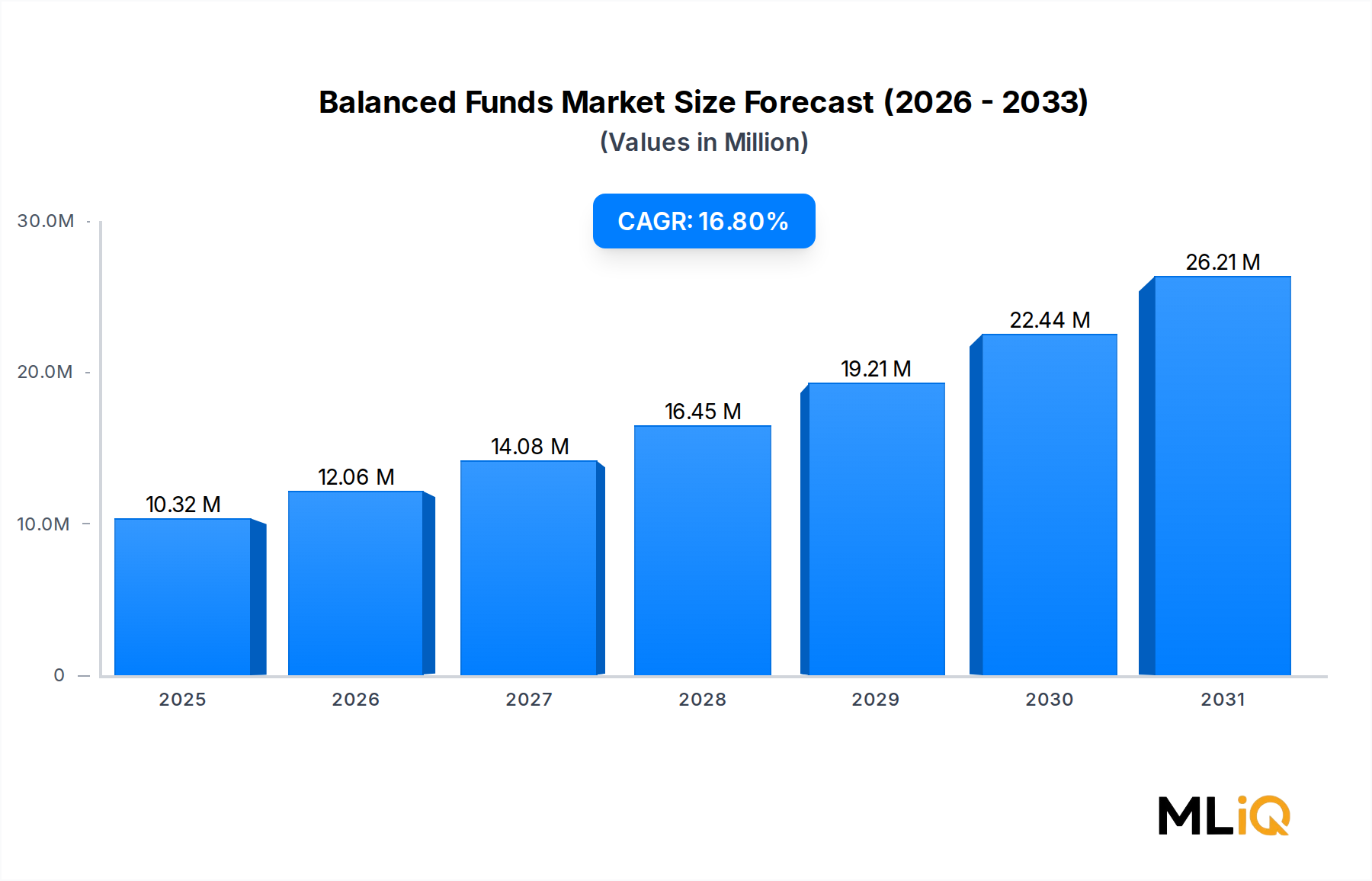

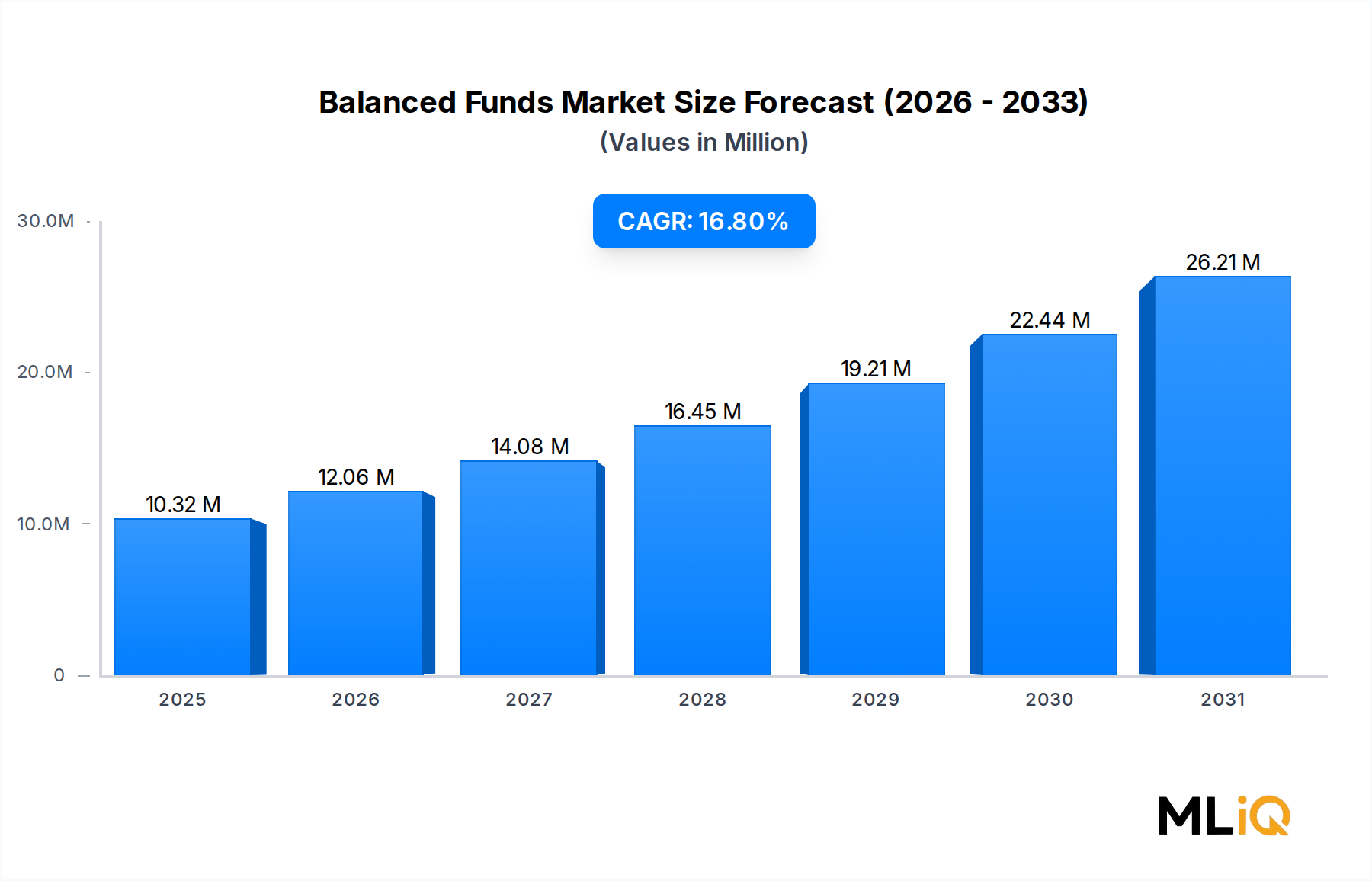

From a competitive standpoint, fund houses are investing heavily in investor education, digital engagement platforms, and personalized financial planning tools to deepen penetration within both sub-cohorts. The long-term stickiness of balanced fund investors, particularly those enrolled in systematic investment programs, creates a durable and recurring AUM base that underpins the market's projected growth to $10,321.51 billion by 2033.