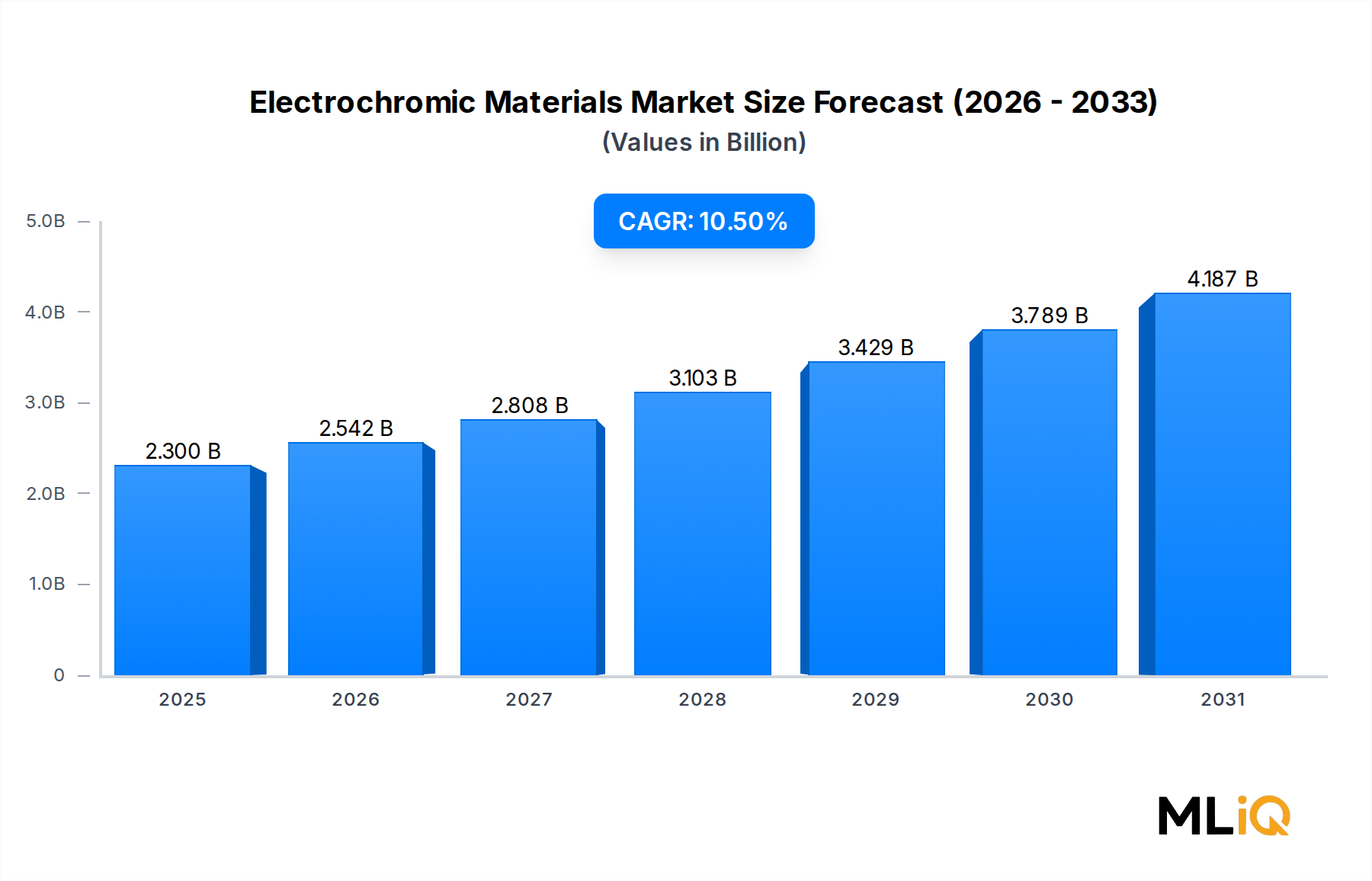

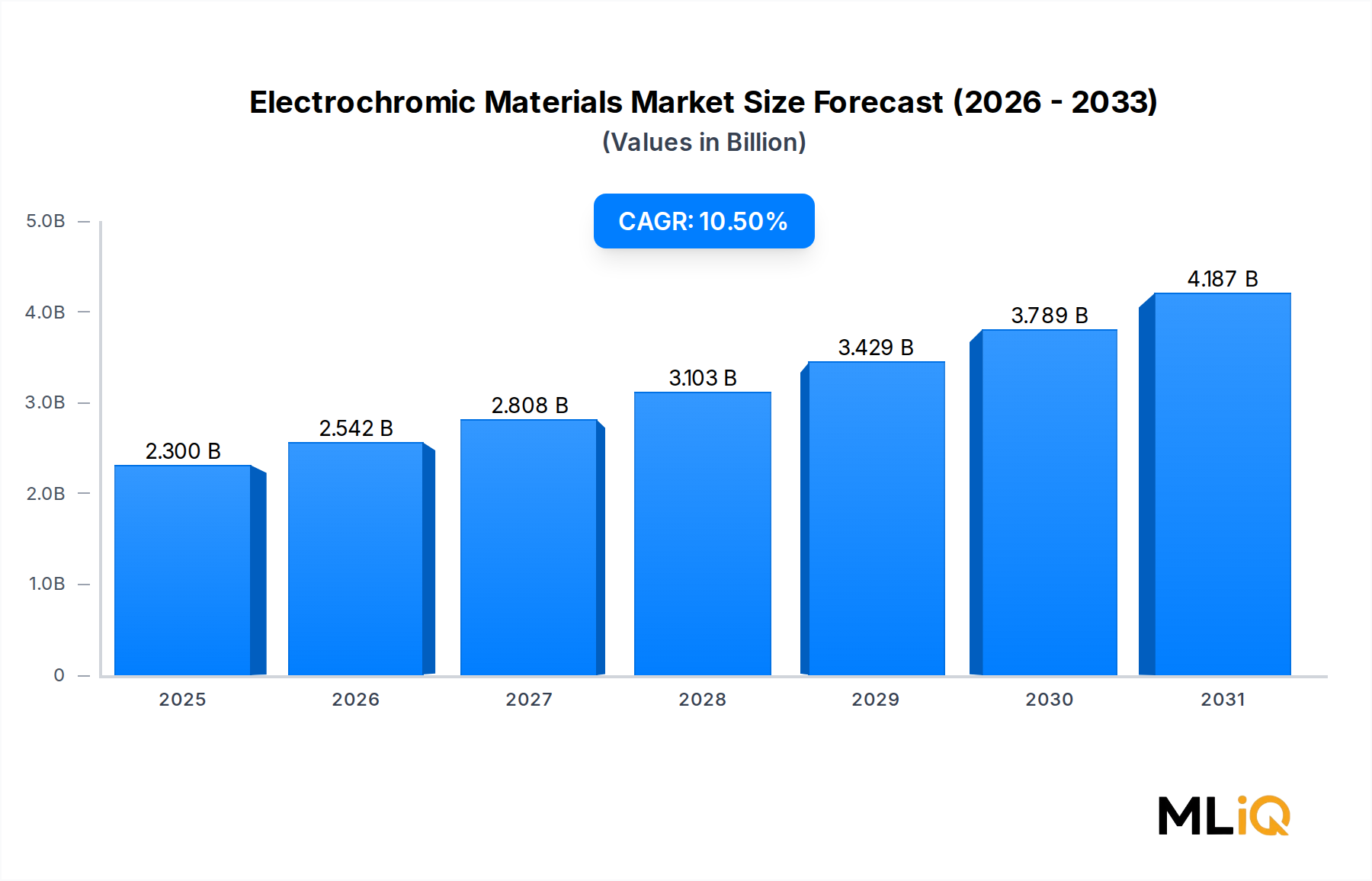

Der globale Markt für elektrochrome Materialien wird im Jahr 2025 auf 2,3 Milliarden USD (ca. 2,14 Milliarden €) geschätzt. Dies spiegelt eine robuste Expansionsentwicklung wider, die durch die Beschleunigung der Nachfrage aus den Bereichen Architektur, Automobil, Luft- und Raumfahrt sowie Unterhaltungselektronik untermauert wird. Der Markt wird voraussichtlich über den Prognosezeitraum mit einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 10,5 % wachsen, angetrieben durch die Konvergenz intelligenter Gebäudevorschriften, die Elektrifizierung des Transportwesens und steigende Verteidigungshaushalte – insbesondere der US-Regierung.

Elektrochrome Materialien sind Substanzen, die ihre optischen Eigenschaften – Transmission, Reflexion oder Absorption – bei Anlegen einer Spannung reversibel ändern. Diese funktionale Eigenschaft positioniert sie als grundlegende Wegbereiter für dynamische Verglasungen, adaptive Optiken und energieeffiziente Gebäudehüllen. Da globale Bauvorschriften zunehmend einen geringeren Energieverbrauch pro Quadratmeter vorschreiben, haben sich elektrochrome Gläser und Beschichtungen von Premium-Neuheiten zu nahezu standardmäßigen Spezifikationsartikeln im gewerblichen Bauwesen entwickelt.

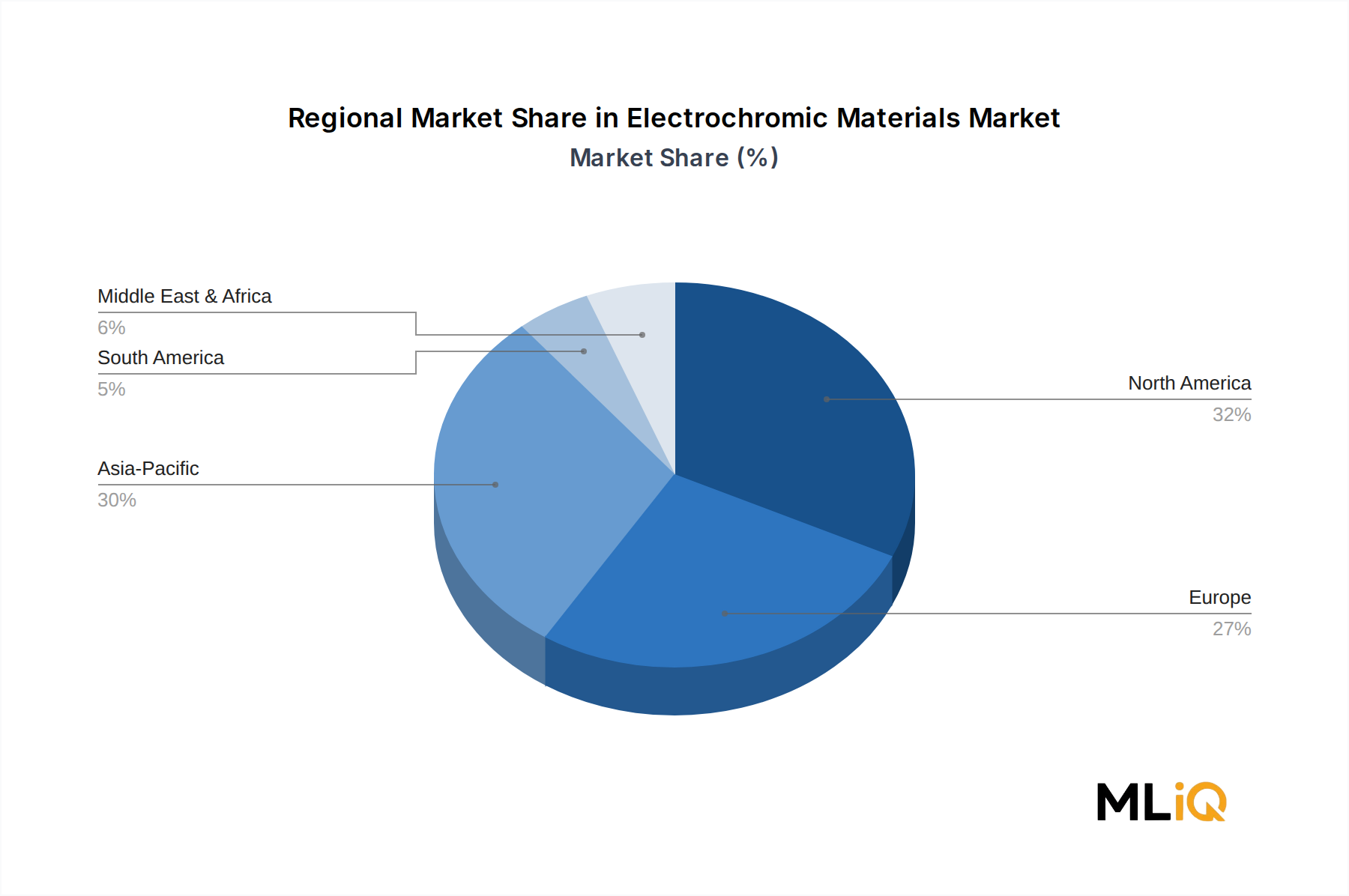

Ein entscheidender makroökonomischer Rückenwind ist der sich intensivierende Fokus auf grüne Gebäudezertifizierungssysteme wie LEED, BREEAM und WELL. Gebäude, die elektrochrome Fenstersysteme einsetzen, können die HLK-Lasten (Heizung, Lüftung, Klima) um bis zu 30 % reduzieren, eine Zahl, die bei institutionellen Immobilienentwicklern und Unternehmensnutzern, die Netto-Null-Verpflichtungen verwalten, stark Anklang findet. Dieses Nachfragesignal ist besonders robust in Nordamerika und Westeuropa, wo Vorschriften zur Offenlegung von Kohlenstoffemissionen die Kosten bei Nichteinhaltung erhöhen.

Im Bereich der Unterhaltungselektronik haben tragbare Geräte, intelligente Brillen und Displaytechnologien begonnen, dünne elektrochrome Schichten zu integrieren, um Sichtschutzfilterung, Blendungsreduzierung und Anpassung an das Umgebungslicht zu erreichen. Die Miniaturisierung elektrochromer Geräte und die Entwicklung flexibler Polymersubstrate erschließen völlig neue Anwendungsbereiche, einschließlich faltbarer Displays und adaptiver Linsensysteme.

Im Automobilsektor hat die Verbreitung elektrochromer Rückspiegel – die heute sowohl in Mittelklasse- als auch in Luxusfahrzeugen zu finden sind – eine dauerhafte, hochvolumige Einnahmequelle für Marktteilnehmer geschaffen. Die Akzeptanzraten von automatisch abblendenden Spiegeln in Personenkraftwagen haben in nordamerikanischen und europäischen OEM-Plattformen bis 2024 40 % überschritten, was signalisiert, dass dieses Teilsegment die Kommerzialisierungsschwelle überschritten hat und nun schnell skaliert.

Der Bereich Luft- und Raumfahrt sowie Verteidigung stellt eine höhermargige, volumenmäßig kleinere Gelegenheit dar. Beschaffungsprogramme der Regierungen in den Vereinigten Staaten, Frankreich und dem Vereinigten Königreich integrieren elektrochrome Kabinenverglasungen und adaptive Cockpit-Visiere in Flugzeugplattformen der nächsten Generation, was langfristige Verträge mit hohen Markteintrittsbarrieren für Wettbewerber ermöglicht.

Mit Blick auf die Zukunft wird die Entwicklung des Marktes durch die Kostenreduktionskurven der Vakuumbeschichtung und des Sol-Gel-Verfahrens, die Verfügbarkeit kritischer Rohstoffe wie Wolframtrioxid und Iridiumoxid sowie das Tempo regulatorischer Vorschriften, die eine dynamische Solarregelung in Gewerbegebäuden erfordern, geprägt sein. Analysten erwarten, dass der Markt bis zum Ende des Jahrzehnts 6,0 Milliarden USD übertreffen wird, wobei der asiatisch-pazifische Raum aufgrund der beschleunigten Urbanisierung und der expandierenden Fertigungskapazitäten in China, Südkorea und Indien als am schnellsten wachsende Region hervorgehen wird.