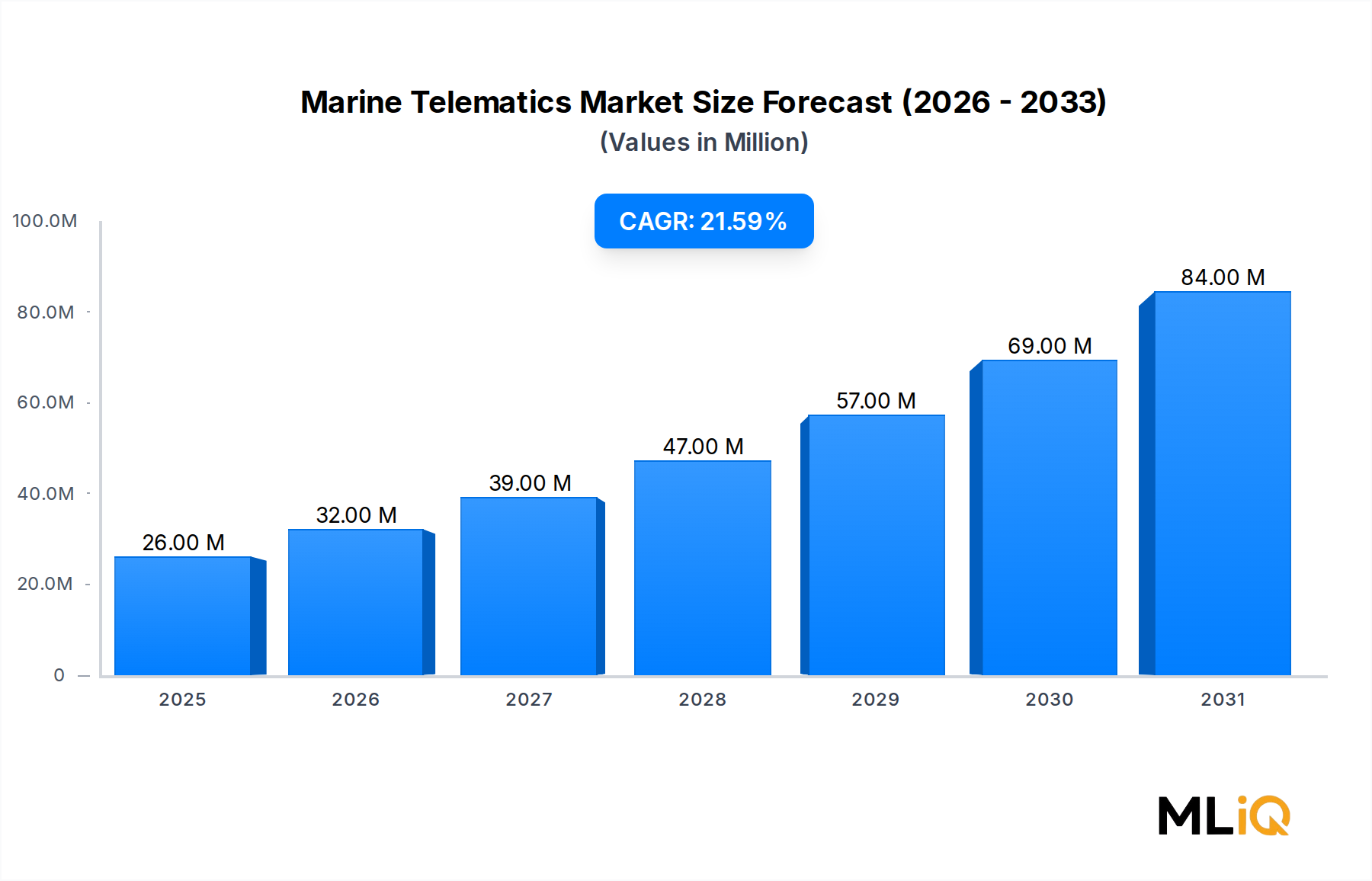

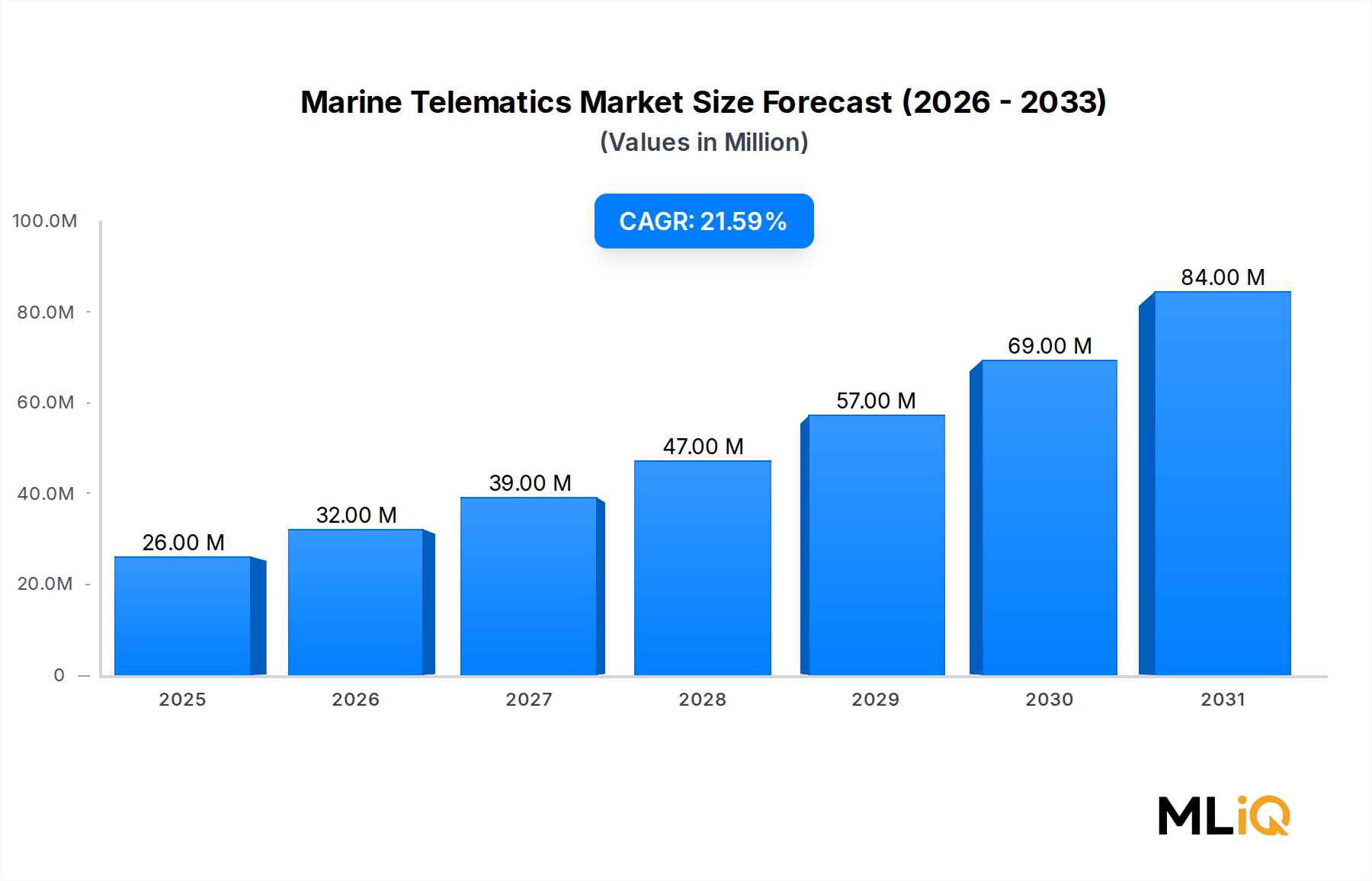

Commercial Segment Dominance in the Marine Telematics Market

Among the application segments analyzed in the Marine Telematics Market — commercial, passenger, and defense — the commercial segment commands the largest revenue share and is projected to maintain its leadership position throughout the forecast period of 2025–2033. This dominance stems from a combination of structural demand factors, regulatory pressure, and the sheer scale of the global commercial maritime fleet, which encompasses container ships, bulk carriers, tankers, fishing vessels, and offshore support vessels.

The commercial segment's primacy is rooted in the economic imperative facing shipping companies: fuel costs alone account for approximately 50–60% of total vessel operating expenses. Marine telematics platforms that deliver real-time engine diagnostics, voyage optimization algorithms, and fuel consumption monitoring directly address this cost pressure, creating a strong return-on-investment case that accelerates adoption. Leading operators of large commercial fleets have demonstrated that telematics-enabled route optimization can reduce fuel expenditure by 8–15% per voyage, a figure that compounds meaningfully at scale.

Regulatory compliance is another structural driver within the commercial segment. The IMO's Carbon Intensity Indicator (CII) regulations, which came into effect in January 2023 and impose annual vessel performance ratings, have made telematics data collection not merely advantageous but operationally necessary for fleet compliance reporting. Commercial operators failing to document fuel efficiency improvements face restrictions on vessel operations, creating a hard deadline-driven adoption cycle that no segment-level competitor can avoid.

Within the commercial segment, service sub-categories play differentiated roles. Safety and security telematics — covering emergency alerting, anti-piracy tracking, and man-overboard detection — represent the foundational layer upon which commercial operators first deploy telematics systems. Information and navigation services, the second major sub-segment, add voyage planning, weather routing, and electronic chart integration. Diagnostics services are the fastest-growing sub-segment within commercial applications, as predictive maintenance algorithms mature and demonstrate measurable reductions in unexpected mechanical failures.

Key players actively competing for commercial segment contracts include Sentinel Marine Solutions, which specializes in real-time fleet visibility for offshore support vessel operators; Traxens, which has positioned its IoT container tracking platform for intermodal commercial logistics; and Technoton, a provider of fuel monitoring hardware widely deployed across bulk carrier and tanker fleets. These companies have pursued differentiated strategies — hardware-led, platform-led, and connectivity-led — reflecting the diversity of commercial operator requirements.

The commercial segment's share within the overall Marine Telematics Market is not merely holding steady but actively consolidating, as smaller niche providers are being absorbed into broader platform ecosystems. The move toward integrated telematics suites that bundle safety, navigation, diagnostics, and entertainment into a single subscription offering is compressing the standalone hardware market and concentrating revenue among platform-capable vendors. This consolidation dynamic suggests the commercial segment will increasingly be defined by a small number of full-stack solution providers and a longer tail of hardware component specialists.

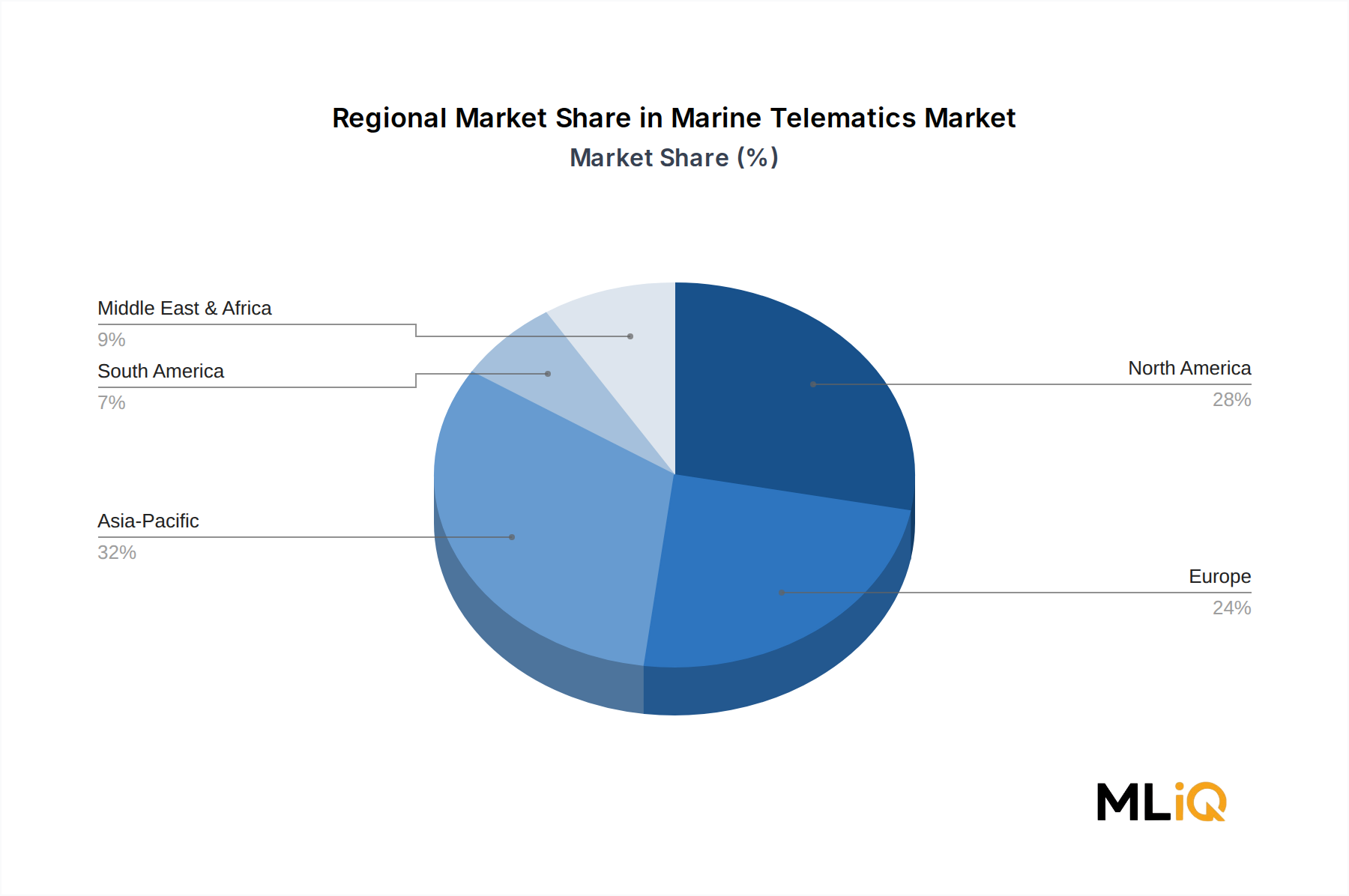

From a geographic standpoint, commercial segment demand is most concentrated in Asia Pacific, where the world's largest merchant fleets are registered, and in Northern Europe, which hosts significant offshore energy and fishing fleet operations. The North American Gulf of Mexico offshore services market is also a high-value commercial subsegment, driven by oil and gas exploration activity that relies heavily on telematics for vessel dispatch and safety compliance.

The passenger and defense segments, while growing, remain considerably smaller in absolute revenue terms. The passenger segment is gaining momentum as ferry operators and cruise lines invest in passenger-facing entertainment and navigation telematics, while the defense segment is characterized by high unit values but constrained volume due to procurement cycles and classification requirements. Neither segment is positioned to challenge commercial dominance within the forecast horizon.