Railway Transport Dominance in the Intermodal Freight Transportation Market

Railway Transport represents the single largest segment within the Intermodal Freight Transportation Market, commanding the highest revenue share among all transportation type segments. Its dominance is rooted in a combination of structural cost advantages, geographic scalability, and increasing governmental support for rail infrastructure as a climate-friendly logistics solution.

From an economic standpoint, rail-based intermodal transport offers a substantially lower cost per ton-mile compared to trucking, particularly for long-haul corridors exceeding 500 miles. For high-volume shippers in manufacturing, retail replenishment, and energy supply chains, this cost differential translates directly into margin improvement, making rail-dominant intermodal the preferred solution at scale. In the United States, for instance, Class I railroads haul approximately 40% of all freight ton-miles, and intermodal traffic consistently ranks as one of the fastest-growing revenue categories for major carriers.

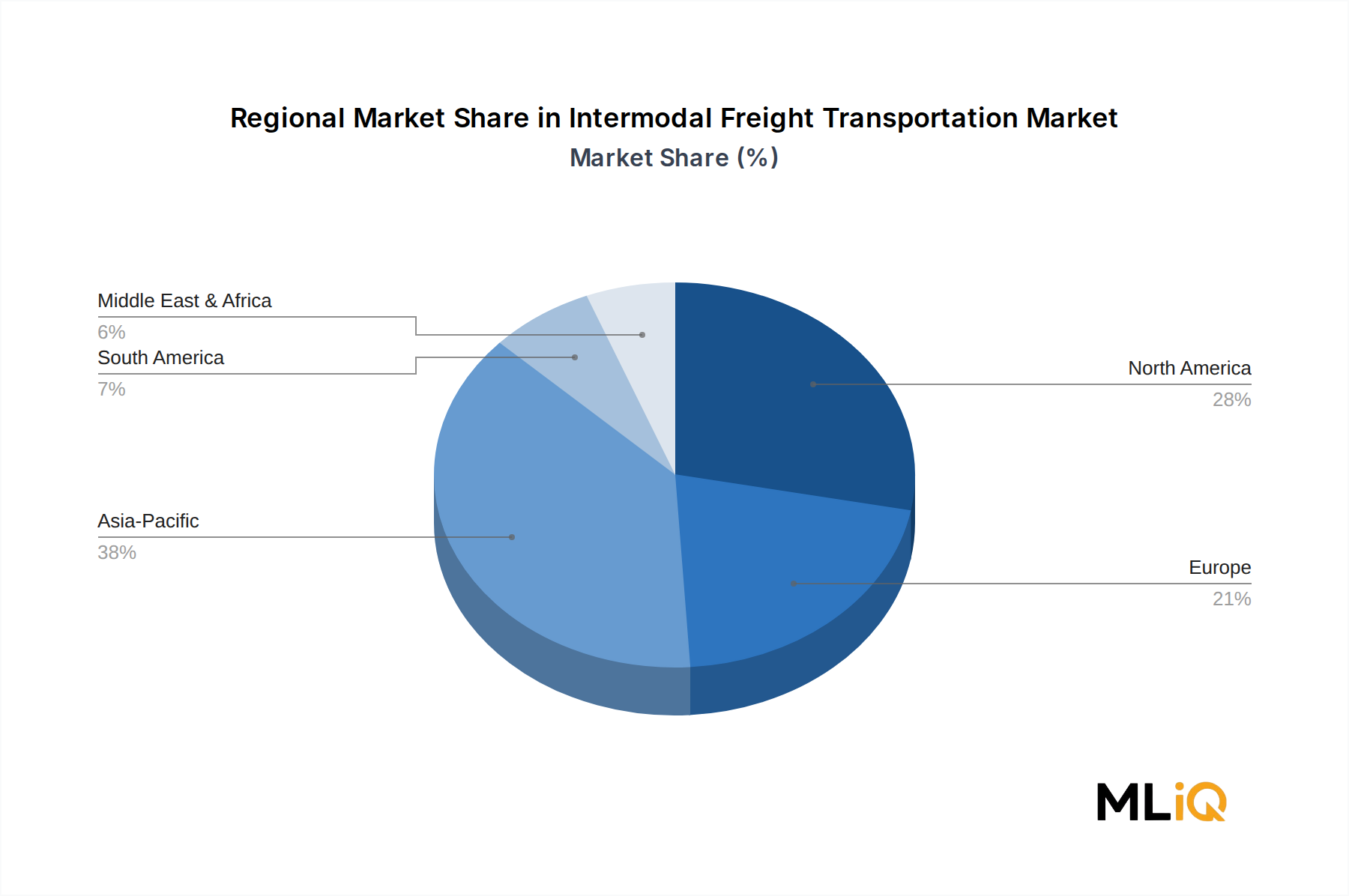

In Asia Pacific — the largest and fastest-growing regional segment — railway intermodal has received unprecedented investment through national infrastructure programs. China's Belt and Road Initiative has extended rail freight corridors deep into Central Asia and Europe, opening new lanes for containerized cargo that previously depended entirely on maritime shipping. India's Dedicated Freight Corridor (DFC) project, connecting the country's major industrial hubs, is similarly catalyzing a structural shift away from over-congested road networks.

In Europe, the Trans-European Transport Network (TEN-T) framework mandates progressive electrification and capacity upgrades across key rail freight corridors, directly supporting intermodal growth. Rail's environmental credentials — emitting approximately 75–80% less CO₂ per ton-kilometer than equivalent road transport — are increasingly central to corporate sustainability procurement criteria, further reinforcing rail's dominant position within the intermodal stack.

Key players deeply entrenched in the railway intermodal segment include Hub Group, Inc., which operates one of North America's largest intermodal networks with thousands of containers and an extensive drayage fleet. J.B. Hunt Transport, Inc. similarly leverages its Intermodal segment as its highest-volume business unit, operating in close partnership with BNSF Railway across transcontinental lanes. These players have invested heavily in proprietary container fleets, terminal access agreements, and digital visibility platforms to differentiate their service quality.

CLX Logistics, LLC. and STG USA have also carved out significant positions by focusing on specialized intermodal services for complex supply chains, including temperature-sensitive and oversized cargo movements that require precise coordination between rail and drayage operators. LOGISTEED, Ltd. brings a strong Asia-Pacific orientation, leveraging rail intermodal capacity on the Eurasian land bridge.

The Railway Transport segment's market share is not merely holding steady — it is actively growing as a proportion of total intermodal revenue. This expansion is being driven by capacity constraints in the truckload market, persistent driver shortages affecting road freight, and accelerating shipper migration to rail-first strategies. While rail infrastructure bottlenecks at terminal interchange points remain a constraint, ongoing capital investment by both public and private stakeholders is progressively alleviating these chokepoints. The segment's outlook through 2033 is exceptionally strong, with double-digit volume growth anticipated across North America, Asia Pacific, and select European markets.