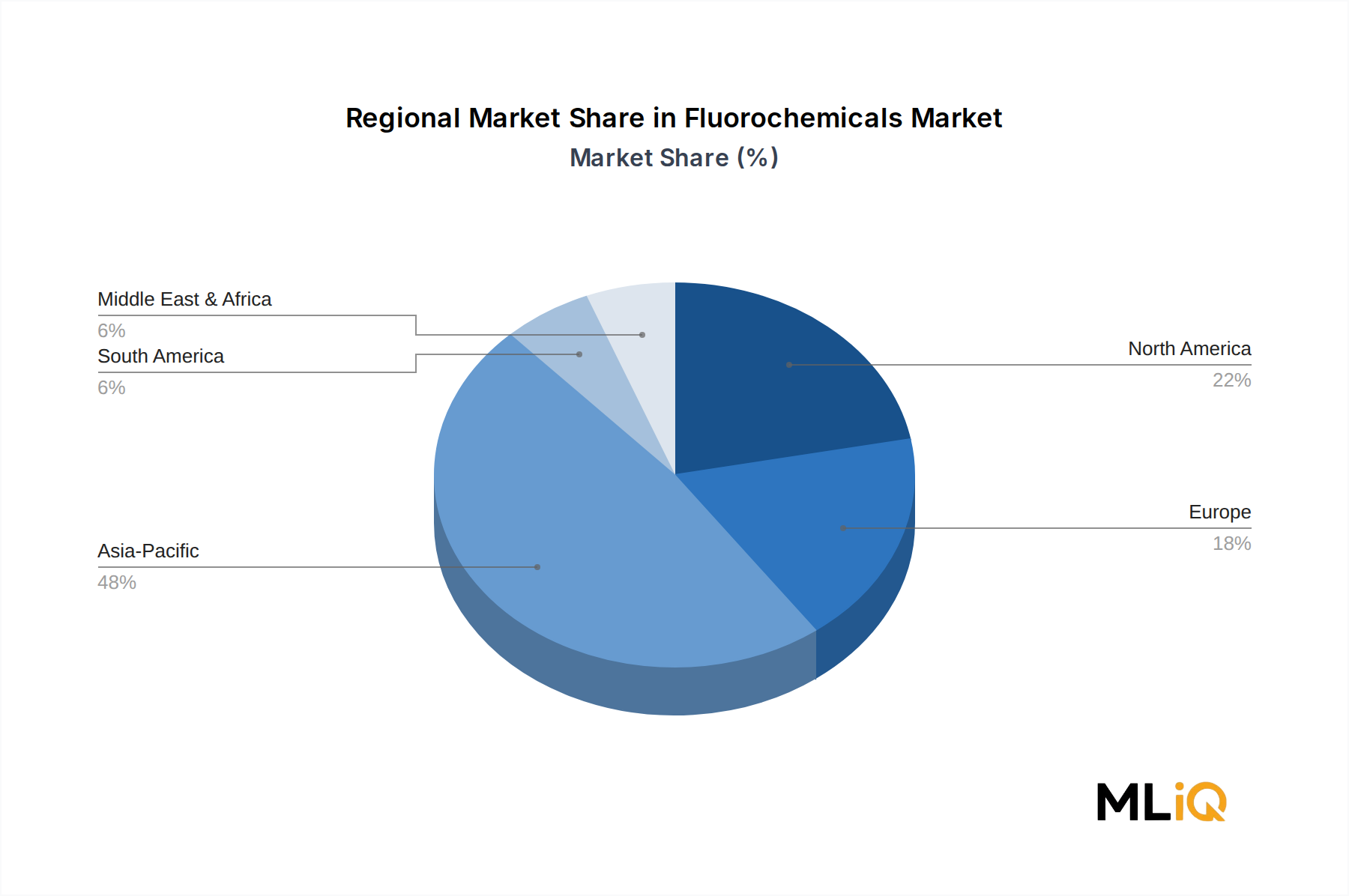

Deutschland, als größte Volkswirtschaft Europas und ein führender Industriestandort, stellt einen bedeutenden Markt für Fluorchemikalien dar, dessen Dynamik sowohl von globalen Trends als auch von spezifischen regionalen und nationalen Gegebenheiten geprägt ist. Obwohl der Bericht den europäischen Markt als den am stärksten regulierten hervorhebt, besteht in Deutschland eine robuste Nachfrage, insbesondere in den Kernindustrien Automobilbau, Luft- und Raumfahrt, Elektronik und Spezialchemikalien. Die im Bericht genannte Nachfrage nach Fluorpolymeren aus der Batteriefertigung für Elektrofahrzeuge ist für Deutschland von besonderer Relevanz, da das Land ein Zentrum für Automobilinnovation und -produktion ist und den Übergang zur Elektromobilität aktiv vorantreibt. Die fortgesetzten Investitionen in die Halbleiterfertigung in Europa, die jährlich deutlich über 139,5 Milliarden € (ca. 150 Milliarden USD im Original) umfassen können, wirken sich ebenfalls direkt auf den deutschen Markt aus, da hochreine Fluorchemikalien hier unverzichtbar sind. Deutschland ist zudem ein wichtiger Akteur bei der industriellen Modernisierung und der Entwicklung von Systemen mit niedrigem GWP, was die Nachfrage nach entsprechenden Kältemitteln und Materialien stimuliert.

Zu den dominanten Unternehmen, die auf dem deutschen Markt aktiv sind, zählen global aufgestellte Spezialchemiekonzerne wie Solvay (Belgien) und Arkema (Frankreich), die mit ihren Fluorpolymer-Portfolios eine starke Position, insbesondere im Batteriesektor und in der Industrie, einnehmen. Auch The Chemours Company (USA) ist mit seinen Marken Teflon und Freon, die in vielen deutschen Industriezweigen eingesetzt werden, präsent. Honeywell International Inc. (USA) spielt eine wichtige Rolle bei der Bereitstellung von HFO-Kältemitteln, die für die Einhaltung der europäischen F-Gas-Verordnung von großer Bedeutung sind. Europäische Spezialisten wie MAFLONS P A (Europa) bedienen zudem den Markt für industrielle Dichtungen und Beschichtungen, der in Deutschland sehr ausgeprägt ist. Der Ausstieg von 3M (USA) aus der PFAS-Produktion hat auch in Deutschland zu einer Umstrukturierung der Lieferketten geführt und Chancen für andere Anbieter geschaffen.

Der regulatorische Rahmen in Deutschland wird maßgeblich durch EU-Vorschriften bestimmt. Die REACH-Verordnung (Registrierung, Bewertung, Zulassung und Beschränkung chemischer Stoffe) ist für alle Fluorchemikalien von zentraler Bedeutung und stellt hohe Anforderungen an die Chemikaliensicherheit. Die F-Gas-Verordnung (EU 517/2014) treibt den Übergang zu Kältemitteln mit geringerem Treibhauspotenzial voran, was den deutschen HVAC-Sektor und die Automobilindustrie direkt beeinflusst. Darüber hinaus hat der von der Europäischen Chemikalienagentur (ECHA) vorgeschlagene universelle PFAS-Beschränkungsvorschlag weitreichende Implikationen für die Produktion und Verwendung von über 10.000 Substanzen in Deutschland. Institutionen wie der TÜV spielen eine wichtige Rolle bei der Zertifizierung und Überprüfung von Produkten und Prozessen, um Sicherheits- und Qualitätsstandards zu gewährleisten, die in deutschen Industrien hoch geschätzt werden.

Die primären Vertriebskanäle für Fluorchemikalien in Deutschland sind Business-to-Business (B2B). Hersteller beliefern direkt OEMs in der Automobil-, Elektronik- und Chemieindustrie oder nutzen spezialisierte technische Distributoren, die kleinere industrielle Abnehmer bedienen. Die Nachfrage wird von hochspezialisierten Anwendungen bestimmt, die maßgeschneiderte Materialien und technische Unterstützung erfordern. Das Einkaufsverhalten deutscher Unternehmen ist oft von einem Fokus auf Qualität, technische Leistung, Zuverlässigkeit und langfristige Lieferbeziehungen geprägt. Angesichts der strengen Umweltauflagen und der Sensibilität gegenüber PFAS achten deutsche Unternehmen und Endverbraucher zunehmend auf umweltfreundlichere und nachhaltigere Produktlösungen, auch wenn dies mit höheren Kosten verbunden sein kann. Die Bereitschaft, in fortschrittliche und konforme Materialien zu investieren, ist hoch, um technologische Führerschaft und regulatorische Konformität sicherzustellen.

Dieser Abschnitt ist eine lokalisierte Kommentierung auf Basis des englischen Originalberichts. Für die Primärdaten siehe den vollständigen englischen Bericht.