1. What are the major growth drivers for the Ethnic Wear Market market?

Factors such as are projected to boost the Ethnic Wear Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

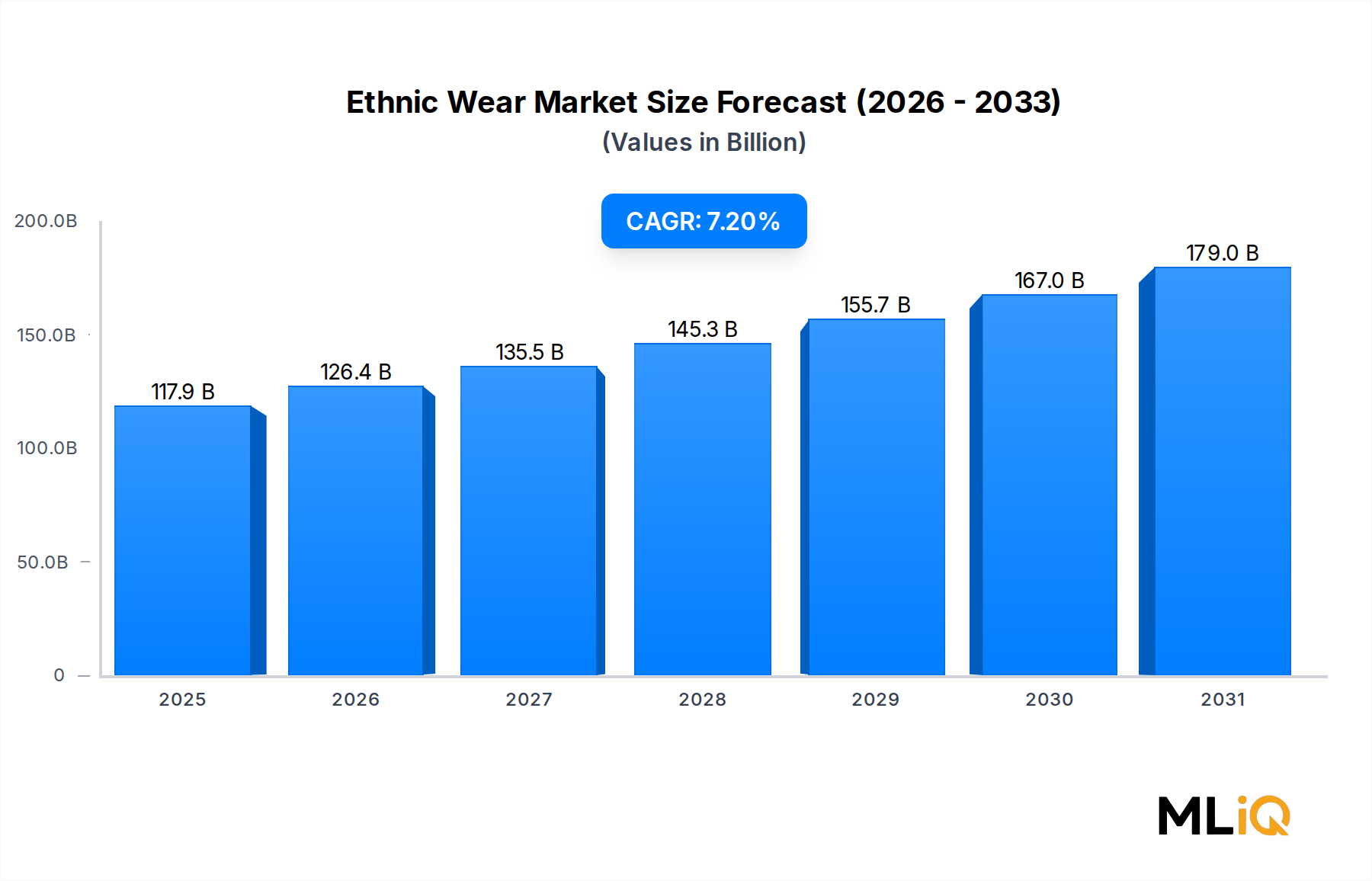

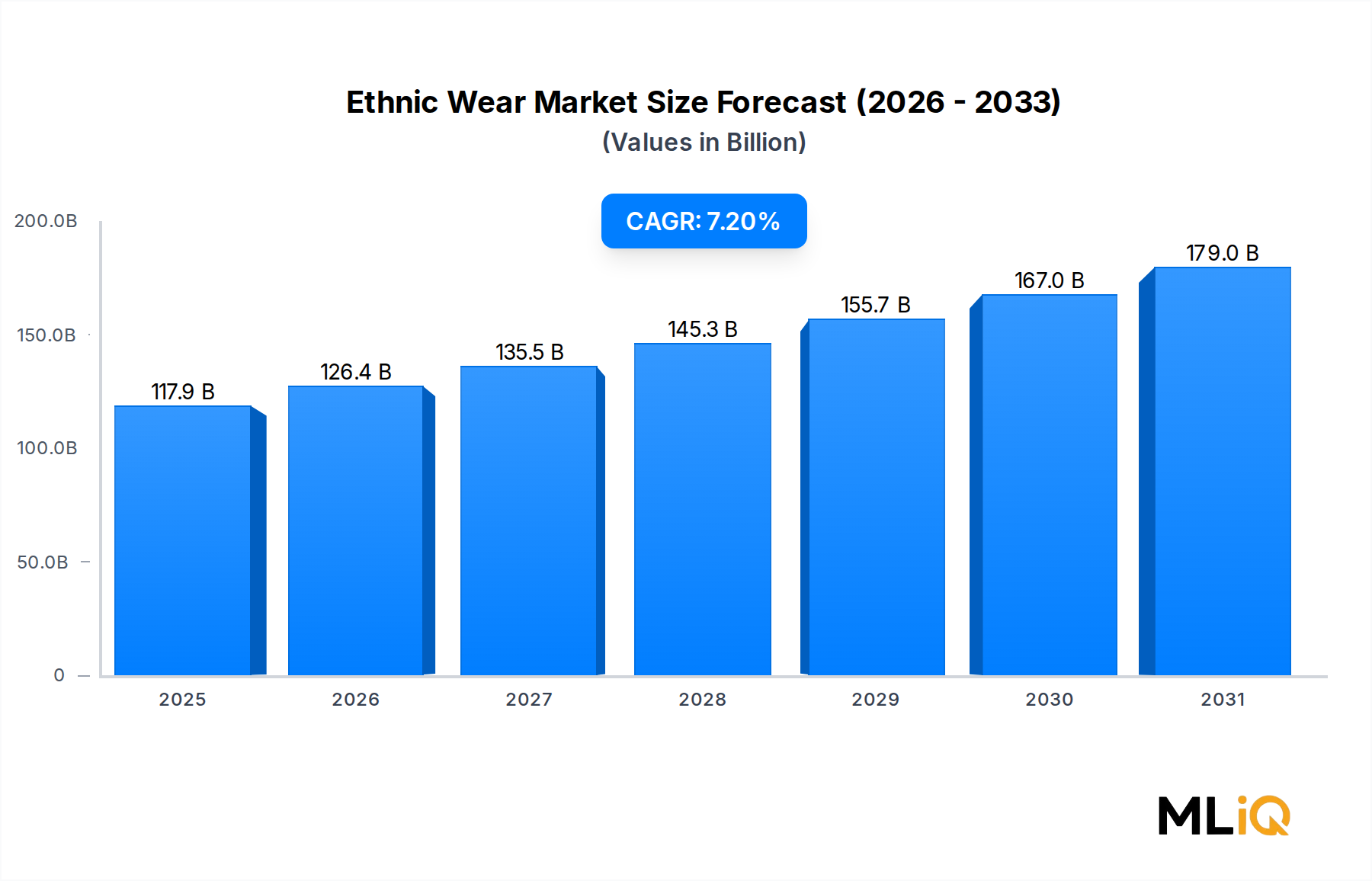

The global Ethnic Wear Market is valued at $117.93 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 7.2% through 2033. This trajectory positions the market among the most resilient segments within consumer goods, underpinned by a convergence of cultural pride, diaspora expansion, and the accelerating digitization of retail channels. At the projected CAGR, the market is on course to surpass $220 billion by the end of the forecast horizon, reflecting robust structural demand rather than cyclical recovery.

Several macro tailwinds are reinforcing this growth. First, the global South Asian, African, and Middle Eastern diaspora communities—collectively numbering over 600 million people—continue to seek culturally authentic apparel for festivals, weddings, and ceremonial occasions, creating year-round demand even in Western markets. Second, the rising middle class in Asia Pacific, particularly in India and Southeast Asia, is translating income growth directly into discretionary spending on premium ethnic garments. Third, the normalization of cultural fashion in mainstream retail—driven partly by global celebrity endorsements and social media visibility—has broadened the consumer base beyond traditional ethnic communities.

From a segmentation standpoint, women's wear commands the largest revenue share, estimated at over 58% of total market value, owing to the higher frequency of ethnic dress adoption during social and religious occasions. Traditional Wear remains the dominant product type, while Fusion Wear is the fastest-growing sub-segment, attracting younger demographics who blend ethnic aesthetics with contemporary silhouettes.

Distribution dynamics are shifting materially. Online channels now account for approximately 34% of total ethnic wear sales globally, up from under 20% five years ago. Platforms tailored to ethnic fashion—particularly in India, the GCC, and Sub-Saharan Africa—are enabling discovery and cross-border commerce at scale.

Key companies operating across this market include regional conglomerates, specialty designers, and digital-native brands that collectively serve a highly fragmented but growing consumer base. The competitive landscape rewards brand authenticity, fabric quality, and cultural resonance over pure price competition. Looking ahead, the integration of AI-driven personalization, sustainable sourcing mandates, and the expansion of occasion-specific product lines will define market leadership through 2033.

The women's segment stands as the unequivocal revenue leader within the Ethnic Wear Market, commanding an estimated 58–62% share of total global revenues. This dominance is not incidental; it reflects deeply embedded socio-cultural norms across South Asia, the Middle East, Sub-Saharan Africa, and Southeast Asia, where women's participation in festivals, weddings, religious ceremonies, and formal social occasions necessitates a wider, more diverse wardrobe of ethnic garments.

In the Indian context alone—which constitutes one of the largest single-country sub-markets—women's ethnic wear encompasses sarees, salwar kameez, lehengas, anarkalis, and a host of regional variants such as Banarasi silk weaves, Kanchipuram drapes, and Chanderi fabrics. The Indian women's ethnic wear sub-segment is valued at over $20 billion domestically and continues to grow at rates exceeding the broader market average, driven by the wedding industry—estimated to generate over $50 billion annually in India—and by the resurgence of ethnic wear in corporate and semi-formal dress codes post-pandemic.

Several leading companies have built their entire brand architecture around the women's ethnic segment. BIBA Fashion Limited has established itself as one of India's most recognized value-to-mid-premium ethnic brands for women, with over 350 exclusive brand outlets and a strong e-commerce presence. Fabindia Limited differentiates through its handloom and craft-forward positioning, appealing to urban, educated women who value artisan heritage alongside contemporary styling. TCNS Clothing Co. Ltd., the parent company of brands like W, Aurelia, and Wishful, has pursued a multi-brand strategy targeting distinct income and age cohorts within the women's segment, reporting consistent double-digit revenue growth in its ethnic and fusion categories.

Modanisa Elektronik Magazacilik ve Tic.A.S. represents a significant player in the Islamic modest wear sub-segment for women, serving markets across Turkey, the GCC, and the broader Muslim diaspora in Europe. With over 70,000 products on its platform from hundreds of brands, Modanisa has effectively become a marketplace aggregator for modest ethnic fashion.

Vedant Fashions Limited, the operator of the Manyavar and Mohey brands, has aggressively expanded its women's bridal ethnic wear line under the Mohey brand, capitalizing on the aspirational wedding occasion segment where average transaction values exceed $150–$300 per garment.

The women's segment's share is consolidating rather than eroding—despite the rapid growth of Fusion Wear and men's ethnic categories. Several dynamics sustain this consolidation: the occasion-driven purchase cycle for women is more frequent (multiple ceremonies per social season), the average selling price per unit is higher, and the style refresh cycle is shorter. Brand loyalty, however, remains lower than in Western fashion, making customer acquisition costs a persistent challenge for market participants.

Digital channels have disproportionately benefited women's ethnic wear. Platforms like Myntra, Nykaa Fashion, and Ajio in India, as well as global marketplaces, have reported that ethnic kurtas and sarees consistently rank among the top-five most-searched apparel categories by women users. This digital visibility translates into faster inventory turnover and improved margin profiles for digitally mature players.

Going forward, premiumization within the women's segment—particularly in bridal and occasion wear—will be the key margin lever. Brands that can combine authentic craftsmanship narratives with seamless omnichannel access are best positioned to capture outsized value as discretionary spending rises across the market's primary geographies.

The Ethnic Wear Market is shaped by a set of quantifiable demand drivers and structural constraints that collectively determine its growth trajectory through 2033.

Demand Driver 1 — Cultural Festivals and Wedding Seasonality: Occasion-driven purchasing is the single most powerful demand accelerator. In India alone, over 10 million weddings are conducted annually, each generating ethnic apparel purchases across the entire family unit. The GCC's Eid and Ramadan seasons generate a spike of 25–35% in ethnic wear retail sales, particularly in the modest fashion and traditional thobes/abayas categories. Festival-linked demand creates a predictable but concentrated revenue cycle that brands have learned to capitalize on through seasonal collection launches.

Demand Driver 2 — Diaspora Communities and Cultural Identity: Over 30 million members of the Indian diaspora and comparable populations from Africa, Southeast Asia, and the Middle East residing in North America, Europe, and Oceania actively purchase ethnic garments for cultural occasions. This diaspora demand supports premium pricing given the limited local availability of authentic ethnic wear and the high willingness to pay among identity-conscious consumers.

Demand Driver 3 — E-Commerce Penetration: Online sales of ethnic wear grew at an estimated 18–22% CAGR between 2019 and 2024, significantly outpacing offline channels. Mobile-first commerce in India, the ASEAN region, and Africa has removed geographic friction between producers and consumers.

Constraint 1 — Unorganized Sector Competition: An estimated 65–70% of ethnic wear production in South Asia and Sub-Saharan Africa is handled by unorganized, informal manufacturers who compete aggressively on price. This suppresses average selling prices in the mass market and compresses margins for organized players.

Constraint 2 — Raw Material Volatility: Dependence on natural fibers—particularly silk, cotton, and wool—makes production costs sensitive to commodity price fluctuations. Cotton prices surged over 40% between 2021 and 2022, directly squeezing margins across the value chain.

Constraint 3 — Cultural Sensitivity and Market Fragmentation: Unlike standardized Western fashion, ethnic wear is highly localized. A design suited for South Indian markets may not resonate in North India or the GCC, requiring extensive product localization that increases SKU complexity and inventory risk.

The competitive landscape of the Ethnic Wear Market is highly fragmented, with a mix of multi-national conglomerates, specialty ethnic fashion brands, and digitally native platforms. The following profiles the key players shaping market dynamics:

Landmark Group: A Dubai-headquartered retail conglomerate with extensive ethnic wear offerings across its Centrepoint and Splash banners in the GCC and South Asia; the group leverages its omnichannel infrastructure to serve both expatriate and local ethnic fashion consumers across more than 20 countries.

Thebe Magugu (Proprietary) Limited: A Johannesburg-based luxury fashion house recognized for fusing contemporary design language with African cultural motifs; the brand has gained international visibility following its LVMH Prize win and exports to select boutiques in Europe and North America.

BIBA Fashion Limited: One of India's leading women's ethnic wear brands with a retail footprint exceeding 350 exclusive outlets; BIBA's strength lies in accessible price points, consistent design refreshes, and a well-developed franchise distribution model across Tier-1 and Tier-2 Indian cities.

TCNS Clothing Co. Ltd.: Operates a portfolio of women's ethnic and fusion brands including W, Aurelia, and Wishful; the company's multi-brand strategy allows it to address distinct consumer cohorts, from value-seeking mass market buyers to aspirational premium shoppers.

Afrikrea: A Pan-African e-commerce marketplace specializing in African ethnic and artisan fashion; Afrikrea connects independent designers and artisans from across the continent to a global diaspora consumer base, positioning itself as a cultural commerce enabler.

Diwan Saheb Fashions Pvt. Ltd.: A specialist in traditional Indian men's ethnic wear including sherwanis and bandhgalas; the brand serves the premium wedding occasion segment and has established a niche in bespoke and semi-bespoke bridal wear.

Newhanfu: A China-based brand focused on Hanfu—traditional Chinese ethnic costume—that has benefited from the domestic cultural revival movement; the brand targets young Chinese consumers aged 18–35 who are driving the Hanfu renaissance via social media platforms like Weibo and Douyin.

ELIE SAAB: A Lebanese couture house with global recognition whose ethnic-inflected luxury eveningwear bridges Middle Eastern cultural aesthetics with high-fashion construction; the brand commands premium pricing and strong brand equity across the GCC and European luxury markets.

Fabindia Limited: India's largest retailer of handloom and craft-based ethnic apparel; Fabindia's model directly links rural artisan clusters with urban consumers, making it a cornerstone of India's ethical and sustainable ethnic fashion narrative.

Nesavaali Ltd.: A UK-based South Asian ethnic wear specialist serving the Indian diaspora in Britain; the brand focuses on occasion and bridal wear and operates both physical boutiques and an active online channel.

Raymond Limited: A vertically integrated Indian textile-to-apparel conglomerate with significant presence in men's ethnic wear; Raymond's Ethnix brand targets the wedding and formal occasion segment with a strong distribution network.

Ochre & Black Private Limited: An Indian luxury ethnic wear brand known for its handcrafted embellishments and premium fabric sourcing; it serves the high-net-worth bridal and couture occasion segment.

Modanisa Elektronik Magazacilik ve Tic.A.S.: The world's leading online modest fashion marketplace, connecting over 70,000 products from hundreds of brands to Muslim women consumers globally.

Vedant Fashions Limited: Operates the Manyavar and Mohey brands, dominating India's celebration and wedding ethnic wear segment with a network of over 600 exclusive outlets.

Rain & Rainbow: An Indian children's ethnic wear brand with a growing presence in the kids' occasion and festive wear category, serving the underserved yet fast-growing kids' ethnic fashion segment.

January 2024: Vedant Fashions Limited announced the expansion of its Mohey bridal ethnic wear store count by 50 new outlets across Tier-2 and Tier-3 Indian cities, targeting the underserved semi-urban bridal market.

March 2024: Fabindia Limited launched a dedicated sustainability initiative, committing to sourcing 100% of its cotton from certified organic or regenerative farming programs by 2027, in response to growing consumer demand for traceable supply chains.

May 2024: Modanisa Elektronik Magazacilik ve Tic.A.S. reported crossing 10 million registered users on its platform, marking a significant milestone in the global modest ethnic fashion e-commerce category.

July 2024: Afrikrea rebranded and restructured its marketplace platform to introduce a Pan-African designer accelerator program, providing selected African ethnic fashion designers with logistics, marketing, and export compliance support.

September 2024: BIBA Fashion Limited entered a strategic distribution partnership with a leading pan-India quick-commerce platform to offer same-day delivery on select ethnic wear SKUs in 15 major Indian cities, marking a first for the ethnic apparel category.

November 2024: Raymond Limited's Ethnix brand crossed 100 exclusive store openings nationally, cementing its position as one of India's fastest-scaling men's ethnic wear retail chains.

February 2025: TCNS Clothing Co. Ltd. announced the integration of AI-powered size recommendation technology across its W and Aurelia online storefronts, targeting a reduction in returns by 25% and improvement in customer satisfaction scores.

April 2025: Thebe Magugu (Proprietary) Limited secured a multi-season collaboration agreement with a European luxury department store group, expanding African ethnic fashion's footprint in Western premium retail.

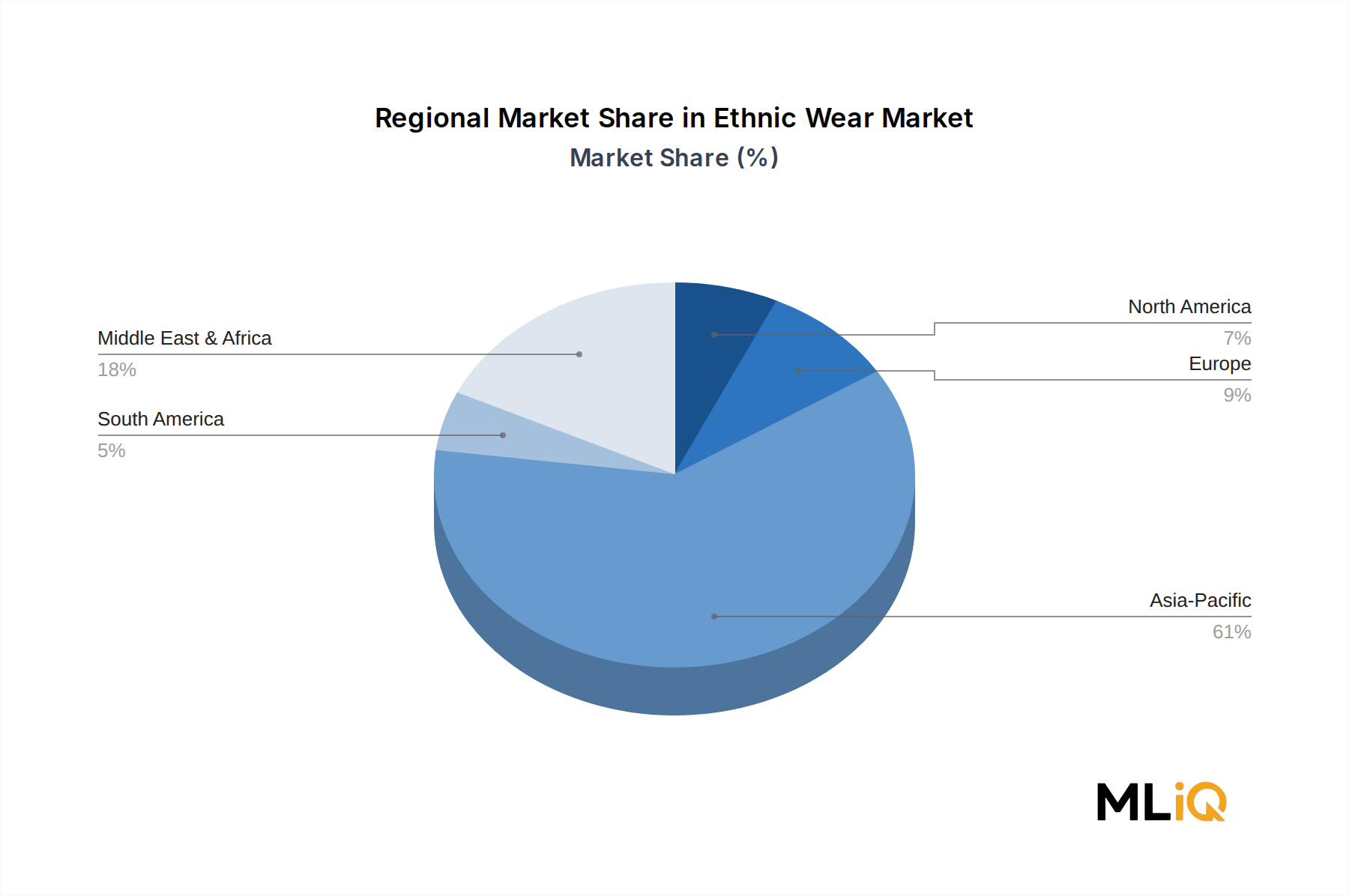

The Ethnic Wear Market exhibits pronounced regional heterogeneity in both growth dynamics and structural maturity, with Asia Pacific anchoring global revenues and Africa emerging as the most dynamic frontier.

Asia Pacific — Dominant Region: Asia Pacific accounts for an estimated 48–52% of global ethnic wear revenues, making it the undisputed market anchor. India alone contributes over $35 billion in domestic ethnic wear consumption, driven by its 1.4 billion population, deep-rooted ceremonial dressing culture, and a wedding market that generates consistent high-value purchases. The region's CAGR is estimated at 8.1%, outpacing the global average. China's Hanfu revival—driven by cultural nationalism and social media—is an increasingly significant growth contributor, with domestic Hanfu market estimates reaching $1.5 billion and growing at double-digit rates.

Middle East & Africa — Fastest-Growing Region: The Middle East & Africa region is projected to register the highest regional CAGR at approximately 9.3% through 2033. The GCC's affluent consumer base, combined with strong demand for modest fashion and traditional thobes, abayas, and kaftans, anchors the Middle Eastern sub-market. Sub-Saharan Africa—particularly Nigeria, Ghana, Kenya, and South Africa—is experiencing a cultural fashion renaissance, with Ankara, Kente, and Dashiki fabrics gaining global visibility. Africa's young population (median age under 20 in many countries) creates a long-duration demand runway.

Europe — Mature Diaspora-Driven Market: Europe's ethnic wear market, valued at approximately $8–10 billion, is primarily driven by South Asian, African, and Middle Eastern diaspora communities in the United Kingdom, France, Germany, and the Benelux countries. The UK alone hosts over 1.8 million South Asians, supporting a robust ethnic wear retail ecosystem in cities like Leicester, Birmingham, and London. The regional CAGR is estimated at 5.4%, reflecting market maturity and saturation in

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Ethnic Wear Market market expansion.

Key companies in the market include Landmark Group, Thebe Magugu (Proprietary) Limited, BIBA Fashion Limited, TCNS Clothing Co. Ltd., Afrikrea, Diwan Saheb Fashions Pvt. Ltd., Newhanfu, ELIA SAAB, Fabindia Limited, Nesavaali Ltd., Raymond Limited, Ochre & Black Private Limited, Modanisa Elektronik Magazacilik ve Tic.A.S., Vedant Fashions Limited, Rain & Rainbow.

The market segments include Type, End User, Distribution Channel.

The market size is estimated to be USD 117.93 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Ethnic Wear Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Ethnic Wear Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.