Scooter and Motorcycle Segment Dominance in the Two-Wheeler Market

Within the Two-Wheeler Market, the motorcycle segment holds the largest share by revenue, owing to its expansive price range, diverse end-use applications, and entrenched consumer loyalty across both utility and recreational use cases. Globally, motorcycles account for an estimated 55–60% of total market revenue, although scooters lead in unit volume in key Asian markets. This bifurcation makes motorcycle the dominant segment by value, a distinction critically important for revenue analysis.

Motorcycles span an exceptionally wide price band — from sub-$1,000 commuter units in Southeast Asia to premium touring machines exceeding $30,000 in Western markets. This breadth allows the segment to simultaneously address utility-driven demand in developing economies and aspirational, lifestyle-oriented demand in affluent markets. In India, the 100–125cc commuter motorcycle category constitutes the largest single sub-segment by volume, with Hero MotoCorp Limited and Bajaj Auto Ltd. collectively commanding a dominant share of this space. In contrast, in Europe and North America, mid-displacement (500–1000cc) and large-displacement (above 1000cc) motorcycles drive disproportionate revenue contributions relative to unit volume.

The premium motorcycle segment has been particularly resilient. BMW AG, through its BMW Motorrad division, reported consecutive years of record deliveries exceeding 200,000 units annually, reflecting the robustness of high-income consumer demand even during macroeconomic volatility. Triumph Motorcycles has similarly repositioned itself as a premium-to-luxury brand, with new model launches in the adventure and roadster segments gaining strong European reception.

In the mainstream segment, Honda Motor Co., Ltd. retains global leadership by virtue of its unmatched production scale, dealer network depth, and model breadth. Honda's CB series and Activa platforms collectively represent tens of millions of units in annual production. Yamaha Motor Co., Ltd. holds a strong second position globally, particularly in Indonesia and Vietnam, where its sport and commuter lineups enjoy brand equity among younger demographics.

The motorcycle segment's share is consolidating rather than expanding at the expense of scooters. The scooter category — particularly automatic transmission variants — has absorbed a significant portion of first-time urban buyers in Asia, given ease of operation and lower maintenance requirements. This competitive dynamic between motorcycle and scooter within the Two-Wheeler Market has pushed OEMs to develop shared platform architectures that reduce development costs while allowing rapid derivatives across both body styles.

Electrification is beginning to alter segment dynamics. While most electric two-wheeler launches to date have been scooter-format, OEMs including Kawasaki Heavy Industries, Ltd. and BMW AG have announced electric motorcycle platforms, signaling the segment's commitment to retaining relevance in a low-emission future. TVS Motor Company and Bajaj Auto Ltd. have also committed to electric motorcycle development pipelines targeting both domestic and export markets.

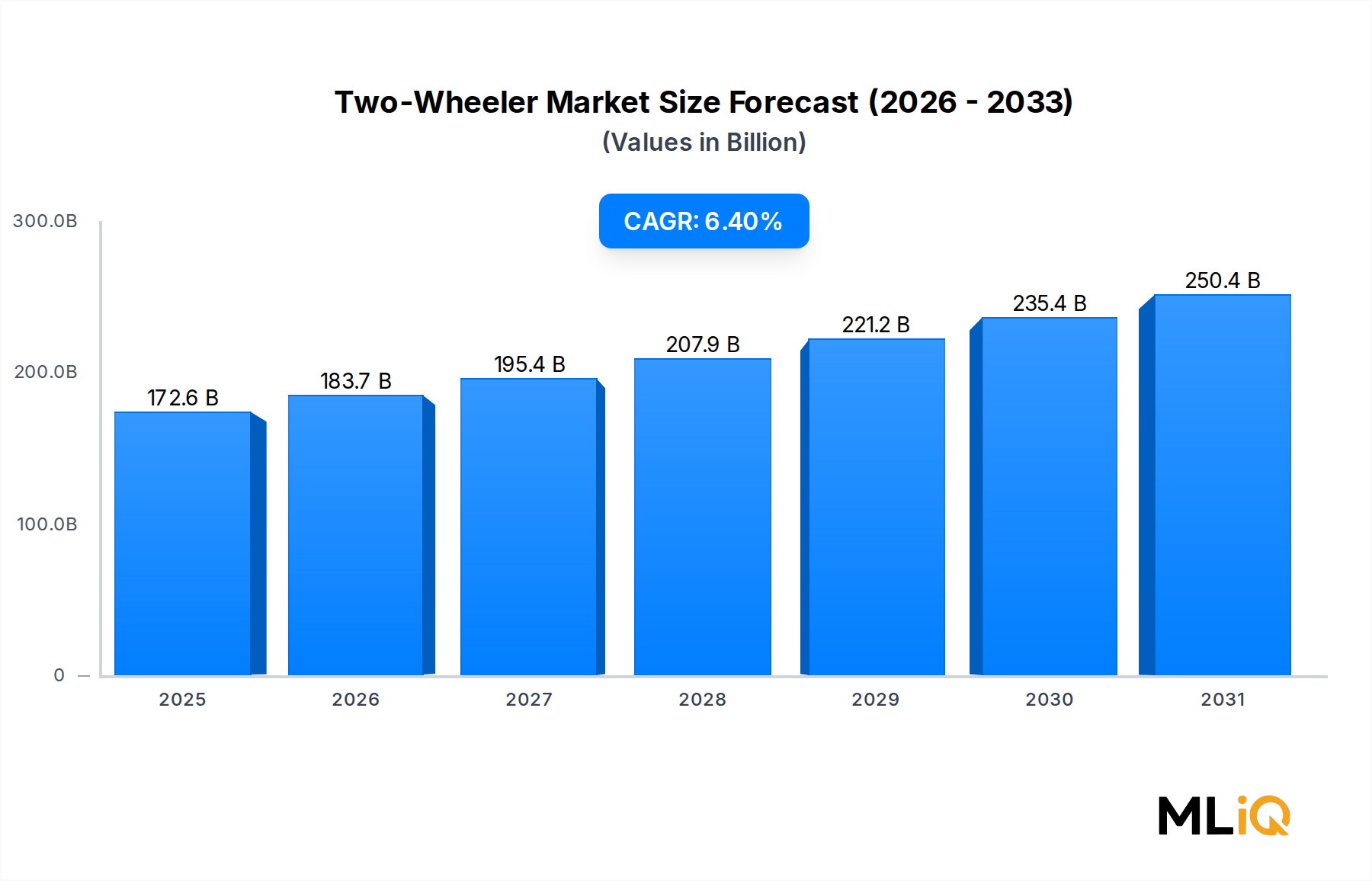

Overall, the motorcycle segment's dominance by revenue is expected to persist through 2033, with its CAGR aligned closely with the market average of 6.4%. The premium sub-segment is likely to outperform, while the entry-level commuter sub-segment in Asia faces margin compression from intensifying local competition and raw material cost pressures.