AC Motor Segment Dominance Within the Electric Vehicle Motor Market

Among the two primary motor type segments — AC Motor and DC Motor — the AC Motor segment commands the largest revenue share in the Electric Vehicle Motor Market and continues to consolidate its leadership position. AC motors, particularly permanent magnet synchronous motors (PMSMs) and induction motors, are preferred in the majority of high-performance BEV applications due to their superior power-to-weight ratio, higher efficiency across a broad RPM range, regenerative braking compatibility, and reduced maintenance burden compared to brushed DC alternatives.

The dominance of AC motors in passenger car applications is exemplified by their near-universal adoption in premium and mass-market BEV platforms. PMSMs, which utilize rare earth permanent magnets to generate rotor magnetic fields without the resistive losses of wound-rotor induction designs, deliver efficiency ratings typically exceeding 95% under optimal load conditions, making them the preferred topology for range-critical passenger EV applications. Induction motors, while slightly less efficient at peak load, offer cost advantages and magnet-free designs that appeal to manufacturers seeking to reduce exposure to rare earth price volatility — an increasingly strategic consideration given geopolitical dynamics in rare earth supply chains.

The EV Traction Motor Market, which largely overlaps with the AC motor segment in the BEV context, is seeing significant capacity investment from suppliers including NIDEC CORPORATION, which has publicly committed to a multi-billion-dollar expansion of its traction motor manufacturing footprint across Asia, Europe, and North America. Similarly, BorgWarner Inc. and Continental AG have deepened their AC motor portfolios through both organic development and targeted acquisitions, while Mitsubishi Electric Corporation brings decades of industrial AC motor expertise into the automotive segment.

Axial-flux AC motor architectures deserve particular attention within this dominance analysis. These designs offer substantially higher torque density and a flat form factor suited to in-wheel or integrated e-axle configurations, and are attracting increasing OEM interest for next-generation platforms targeting performance and space efficiency. Companies such as AISIN CORPORATION are actively developing axial-flux variants for integration into hybrid and plug-in hybrid platforms.

From a vehicle type perspective, Battery Electric Vehicles are the primary volume driver for AC motor adoption, given that full-electric platforms require maximum motor efficiency to optimize range from a fixed energy storage capacity. Hybrid Vehicles and Plug-in-Hybrid Vehicles also increasingly utilize AC motor designs within their hybrid drive modules, though the power output requirements are often lower than in full-BEV applications.

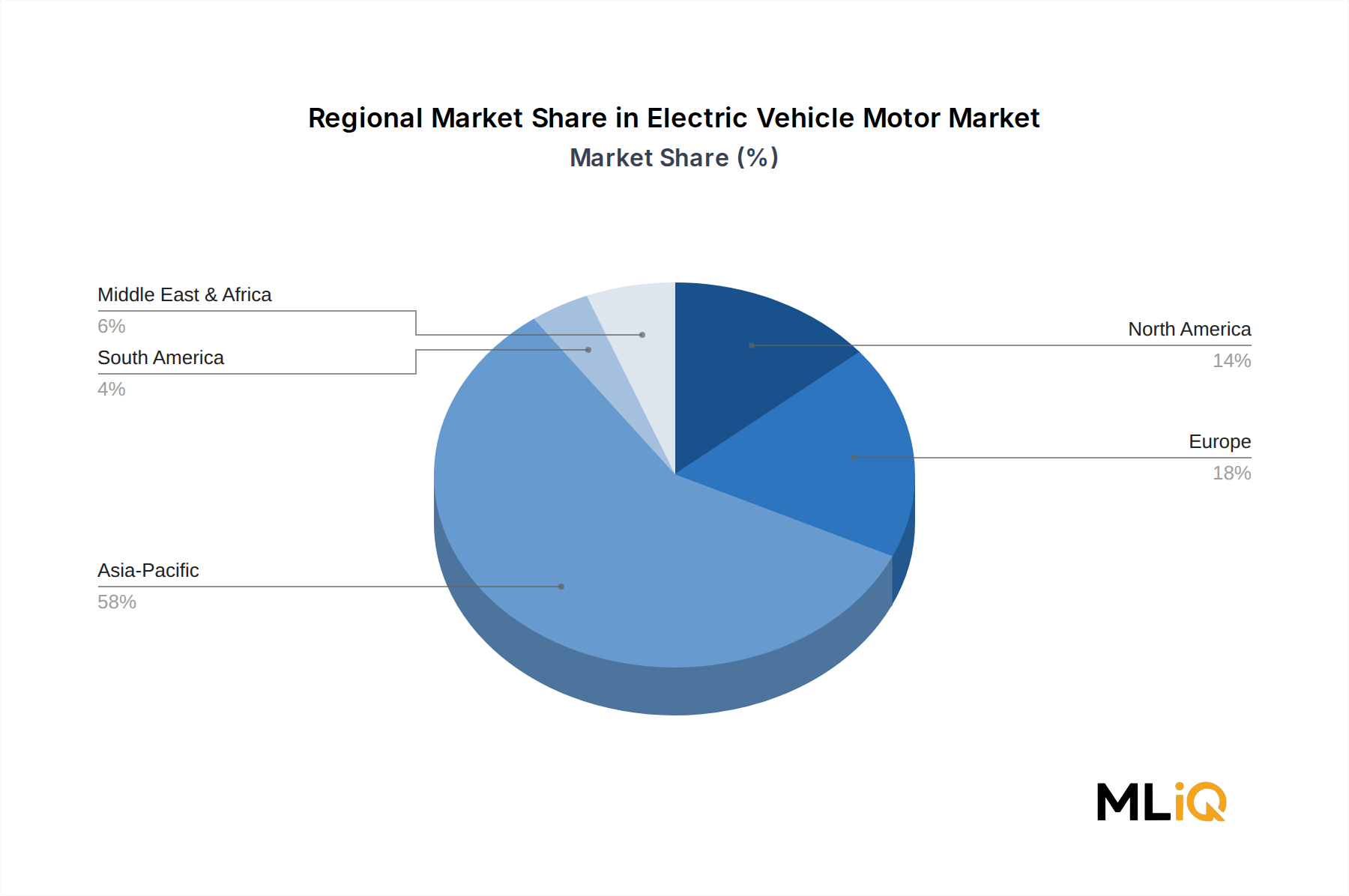

The segment's share is growing, not merely consolidating. As BEV penetration rates rise globally — China exceeded 35% NEV market share in 2023, while Europe crossed the 20% threshold for new BEV registrations in several national markets — the absolute volume of AC motors demanded per year is compounding rapidly. The Permanent Magnet Motor Market, closely intertwined with the PMSM sub-segment of AC motors, is itself a high-growth node benefiting from the same demand dynamics, reinforcing the structural tailwinds for AC motor suppliers across the value chain.

The DC Motor segment, while declining in relative share, retains relevance in lower-cost, lower-performance applications such as auxiliary systems, commercial micro-mobility platforms, and legacy hybrid architectures. However, the directional trend is clearly toward AC motor dominance as platform electrification matures and performance expectations rise across all vehicle segments.