Rotary Wing Dominance in the Commercial Drones Market

Within the Commercial Drones Market, the rotary-wing segment — encompassing multi-rotor and single-rotor helicopter configurations — constitutes the dominant hardware category by both unit volume and revenue share, accounting for an estimated 58–62% of total market value. This dominance is structural rather than cyclical and is rooted in several operational and commercial advantages that rotary platforms hold over fixed-wing and hybrid alternatives.

The primary competitive advantage of rotary-wing drones is their vertical take-off and landing (VTOL) capability, which eliminates the need for dedicated launch infrastructure. This characteristic is particularly decisive in urban and semi-urban environments where clear runway space is unavailable, making rotary platforms the default choice for applications such as infrastructure inspection, real estate photography, emergency response staging, and last-mile logistics trials. In agricultural contexts, multi-rotor platforms are widely used for precision spraying because their ability to hover and maneuver at low altitudes with high positional accuracy directly translates into uniform chemical application and reduced input waste.

The multi-rotor sub-category within rotary systems — including quadcopters, hexacopters, and octocopters — dominates commercial procurement decisions due to their mechanical simplicity, redundancy architecture (additional rotors provide failsafe capability), and the availability of a mature aftermarket for spare parts and accessories. DJI Technology Co., Ltd. has built a near-unassailable position in this sub-segment, particularly in the prosumer and small enterprise tier, with its Matrice and Agras product lines achieving widespread adoption in over 100 countries. The company's integrated ecosystem — combining airframes, gimbal cameras, flight controllers, and proprietary software — creates significant switching costs for enterprise customers.

Yuneec International Co. Ltd. and Parrot SA represent secondary competitors in the rotary segment, each pursuing differentiated strategies. Yuneec targets professional cinematography and inspection operators with its Typhoon and H520 lines, while Parrot has pivoted toward defense-grade and enterprise software-integrated platforms following the divestment of its consumer product lines. SKYDIO has emerged as a disruptive force within the rotary segment specifically through its AI-powered obstacle avoidance technology, which enables fully autonomous flight in complex, GPS-denied environments — a capability increasingly valued by public safety agencies and industrial inspection teams.

Leptron Unmanned Aircraft Systems, Inc. specializes in heavy-lift rotary platforms designed for payload delivery and aerial work in industrial settings, occupying a niche but high-value corner of the segment. AeroVironment, Inc., while historically associated with fixed-wing military small UAS, has expanded its rotary portfolio to serve dual-use commercial and defense customers, particularly in surveillance and reconnaissance applications.

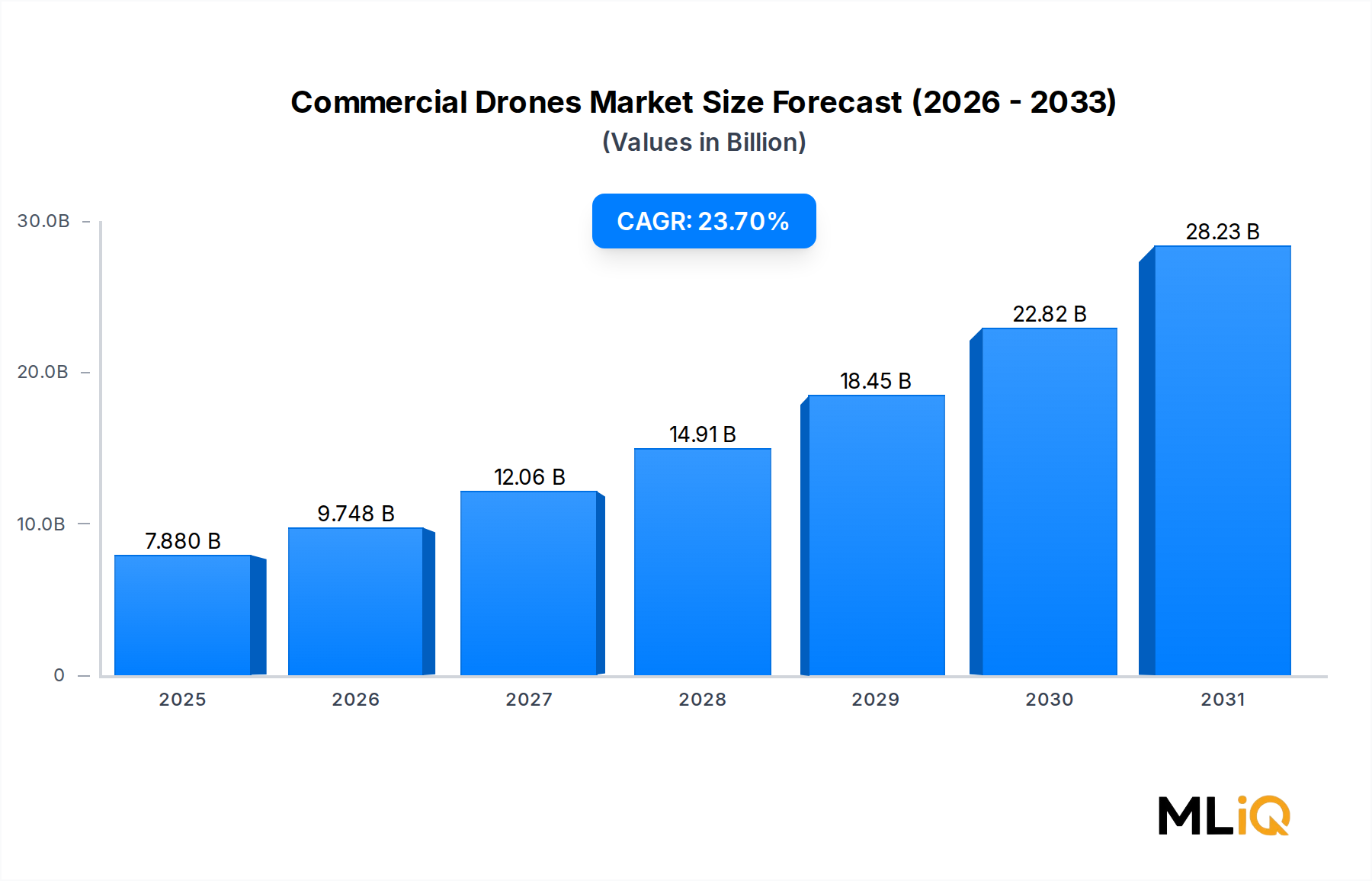

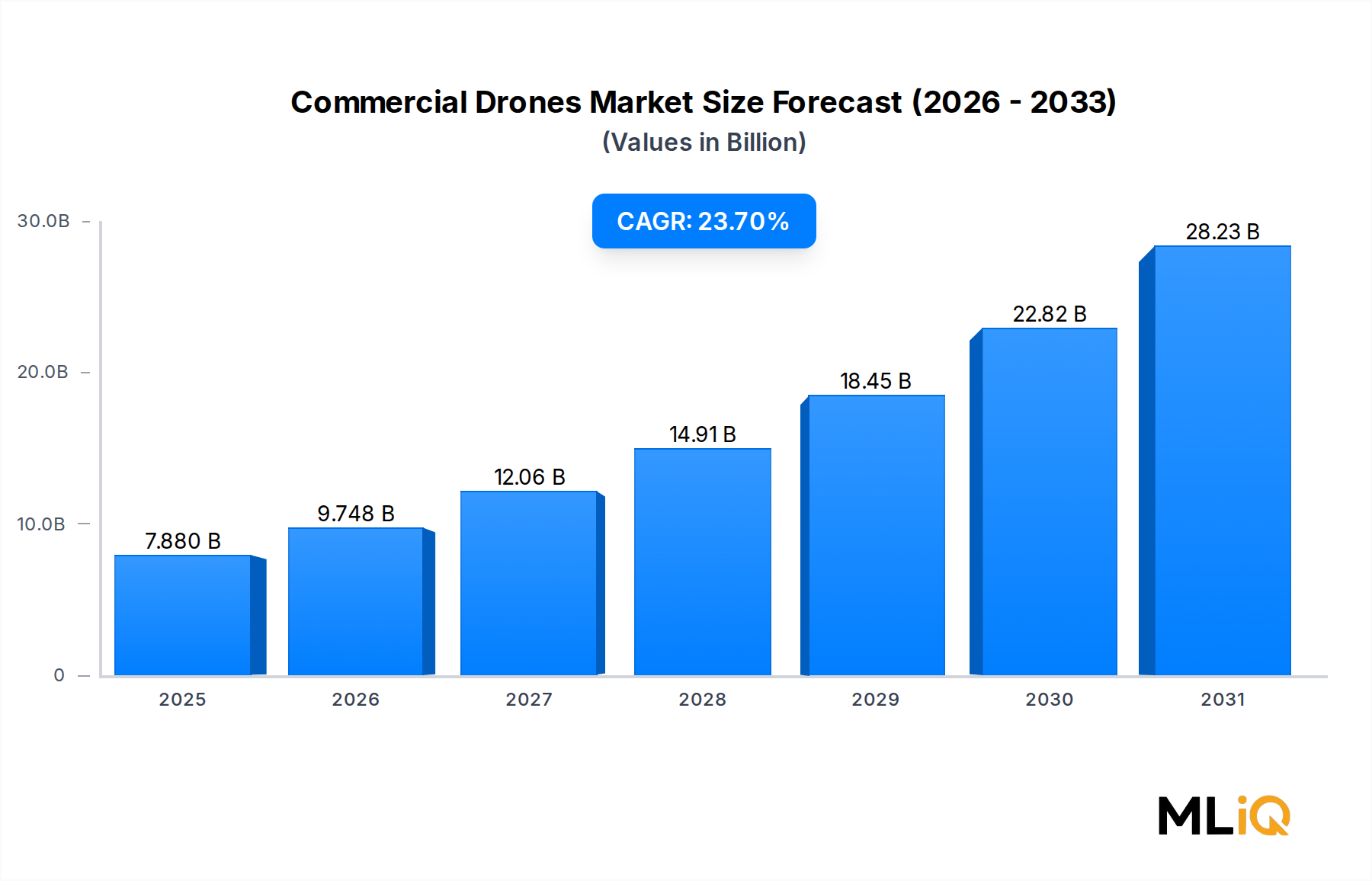

The rotary segment's share is consolidating rather than expanding proportionally, as fixed-wing platforms capture long-endurance survey missions and hybrid eVTOL configurations attract investment for cargo and passenger transport applications. Nevertheless, the absolute revenue generated by rotary platforms continues to grow at a rate consistent with the overall market CAGR of 23.7%, underpinned by the breadth of its addressable use cases and the continued decline in per-unit costs. Component-level innovations — including more efficient brushless motor designs, lightweight carbon fiber frames, and advances in the Drone Battery Market — are extending flight endurance and payload capacity, further reinforcing rotary dominance in the near to medium term.