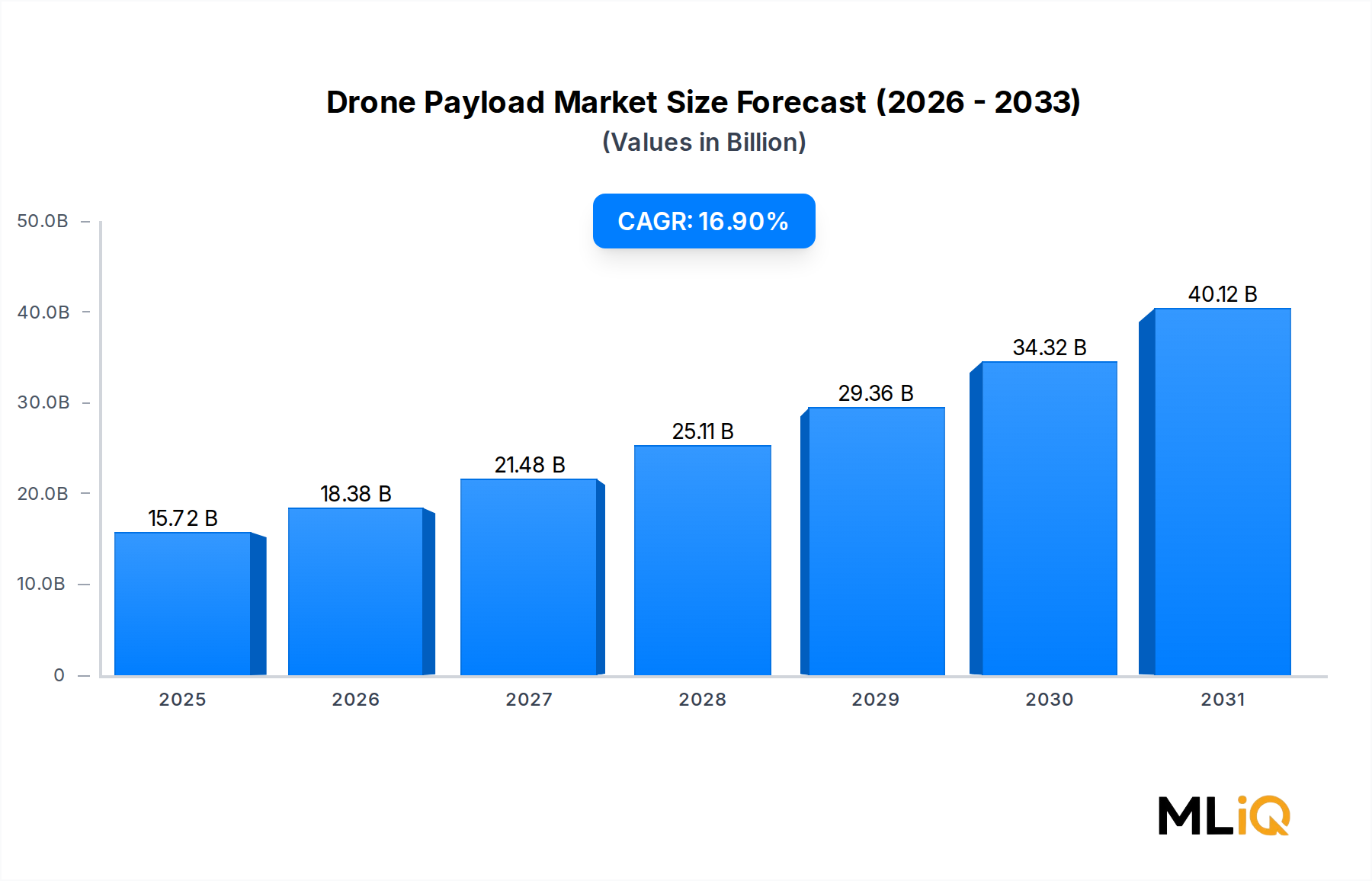

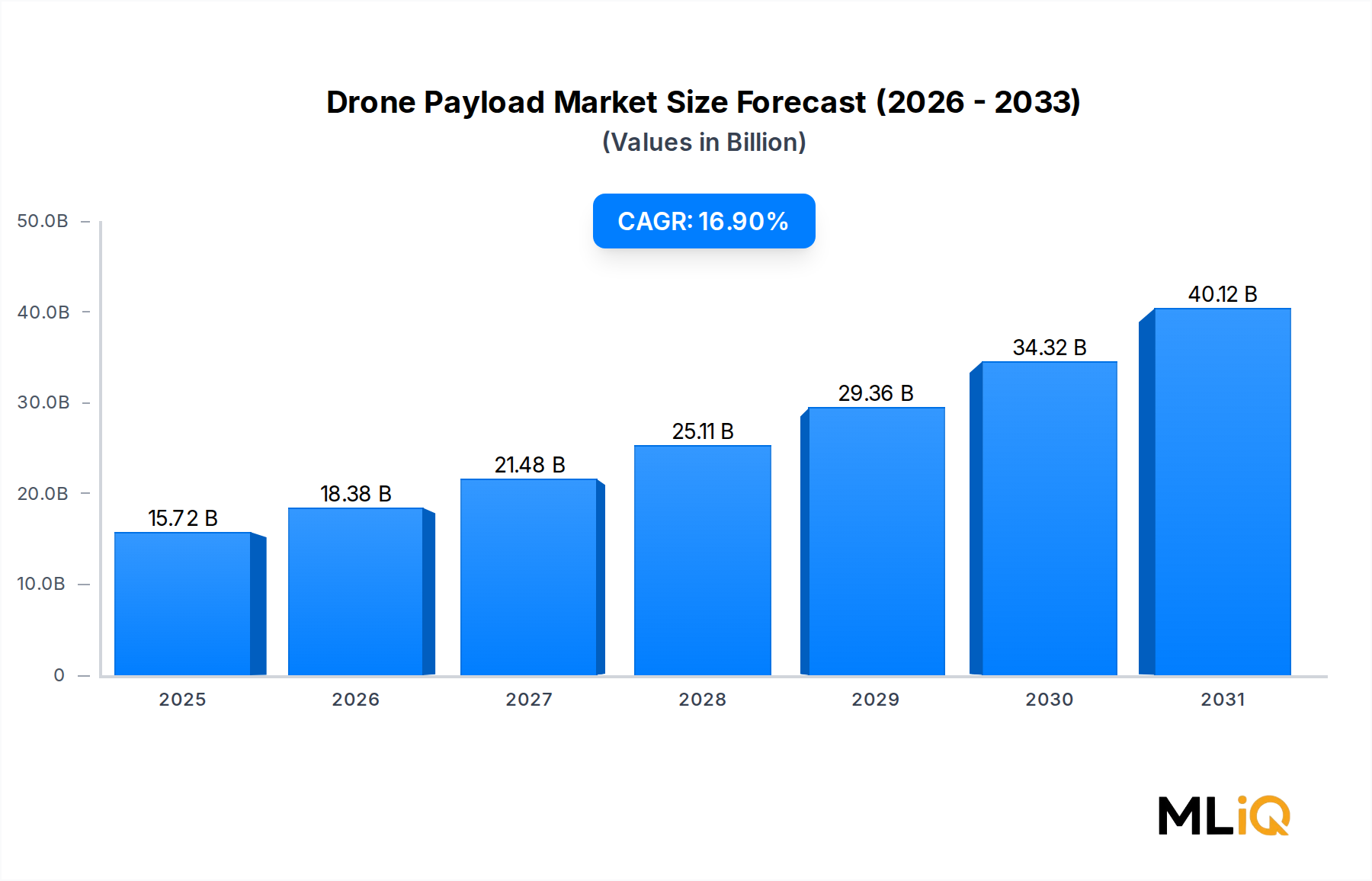

Cameras and Sensors Segment Dominance in the Drone Payload Market

Within the Drone Payload Market, the cameras and sensors segment commands the largest revenue share, a position it has maintained consistently and is expected to reinforce through the forecast period to 2033. This dominance is rooted in the sheer diversity of applications that camera and sensor payloads serve, spanning defense ISR, agricultural monitoring, infrastructure inspection, environmental surveillance, media production, and disaster response. Unlike weaponry or radar and communication payloads — which are either highly restricted or operationally specialized — cameras and sensors represent the universal utility layer of drone technology, deployable by government agencies, commercial operators, research institutions, and individual professionals alike.

The defense application continues to generate the highest per-unit revenue within this segment. Electro-optical/infrared (EO/IR) turret systems, hyperspectral imagers, LiDAR units, and multi-spectral sensors mounted on medium-altitude long-endurance (MALE) and high-altitude long-endurance (HALE) UAVs represent some of the highest-value payload configurations in the market. Teledyne FLIR LLC is the defining incumbent in EO/IR payloads, with its Star SAFIRE and Hadron series representing the benchmark for defense-grade thermal imaging across fixed-wing and rotary-wing platforms. The broader Electro-Optical Infrared System Market serves as a critical growth engine feeding directly into this segment, as advances in detector sensitivity, image resolution, and thermal contrast differentiation continue to elevate payload performance standards.

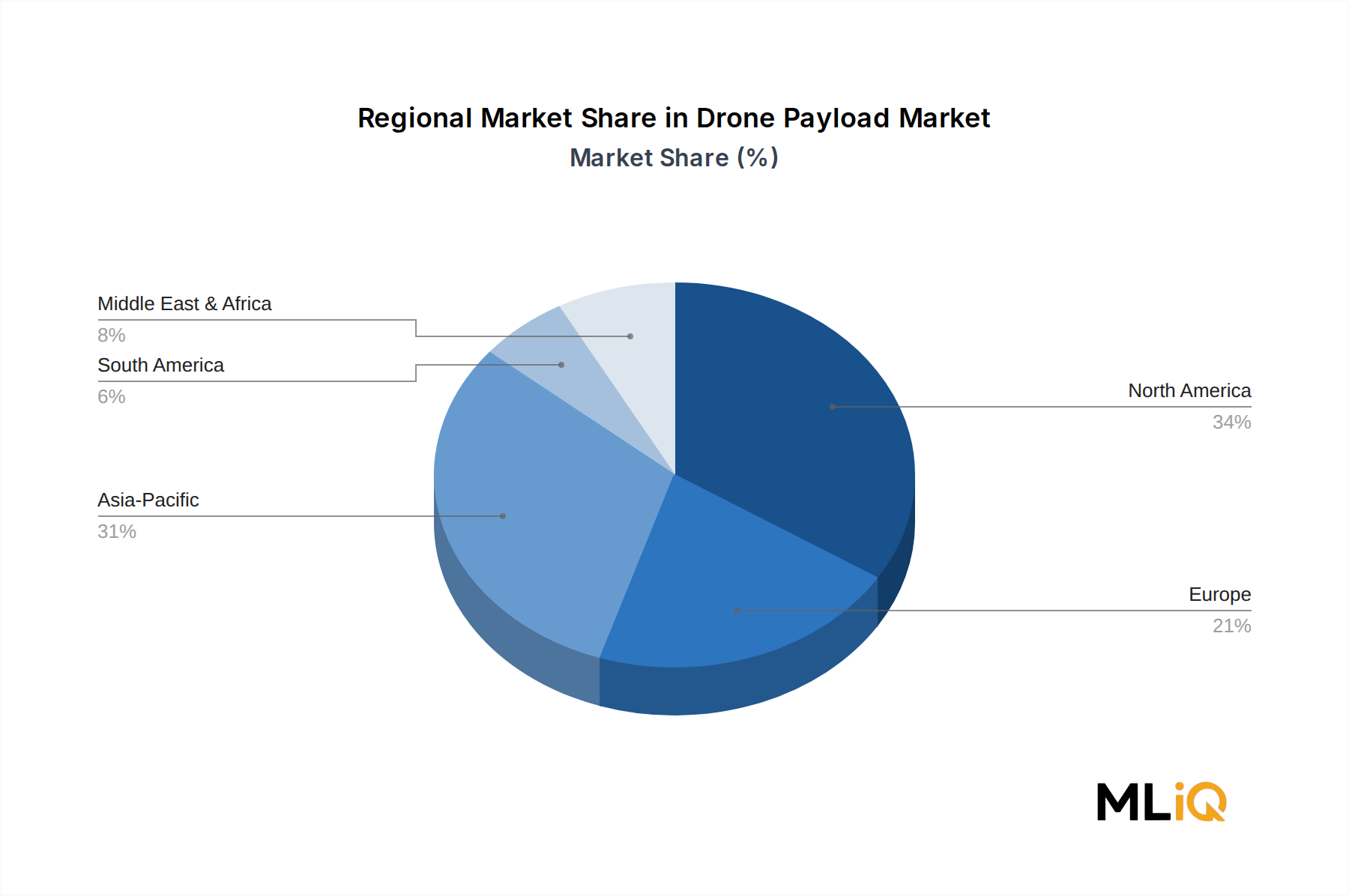

In the commercial domain, the proliferation of high-resolution RGB cameras, multispectral sensors, and LiDAR systems has been instrumental in unlocking the Precision Agriculture Market. Farmers and agribusiness operators in North America, Brazil, China, and Australia are deploying sensor-equipped drones to conduct crop health assessments, soil moisture mapping, pest infestation detection, and yield prediction modeling at costs substantially below traditional manned aircraft or satellite imaging solutions. This agricultural application alone represents a significant pull factor on the cameras and sensors payload segment, with demand particularly strong in ASEAN and South American markets.

Median selling prices for commercial drone sensor payloads have declined substantially over the past five years due to improvements in MEMS-based sensor manufacturing, optical component miniaturization, and intensifying competition among Asian suppliers. This price compression has paradoxically expanded the total addressable market by bringing high-quality sensor payloads within reach of smaller operators, municipalities, and emerging-market clients. The Drone Camera Market, as a distinct commercial sub-segment, has seen unit volumes grow substantially year-over-year as resolution capabilities crossing 50 megapixels and 4K video at high frame rates become standard offerings in mid-tier payloads.

Key players reinforcing segment dominance include DJI Technology, whose Zenmuse series — covering EO, thermal, and LiDAR configurations — has become the default reference point for commercial drone payloads globally. Autel Robotics has intensified competition at the prosumer tier with its EVO series payloads, while Parrot SA has carved a defensible niche in agricultural and public safety sensor systems in Europe and North America. On the defense side, IMSAR LLC has made significant inroads with its miniaturized SAR payloads, enabling fixed-wing and multi-rotor platforms to deliver all-weather, day-night ground surveillance capabilities previously restricted to much larger aircraft.

The segment's share is not merely stable — it is consolidating. As artificial intelligence-driven onboard processing becomes embedded in sensor payloads, enabling real-time object detection, classification, and autonomous decision-making, the functional gap between cameras and sensors and other payload types narrows from a software perspective while the hardware advantage of the sensors segment remains structural. This trajectory reinforces its dominant position well into the 2030s.