1. What are the major growth drivers for the Germany Sharing Economy Market market?

Factors such as are projected to boost the Germany Sharing Economy Market market expansion.

+1 2315155523

Germany Sharing Economy Market

Germany Sharing Economy Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

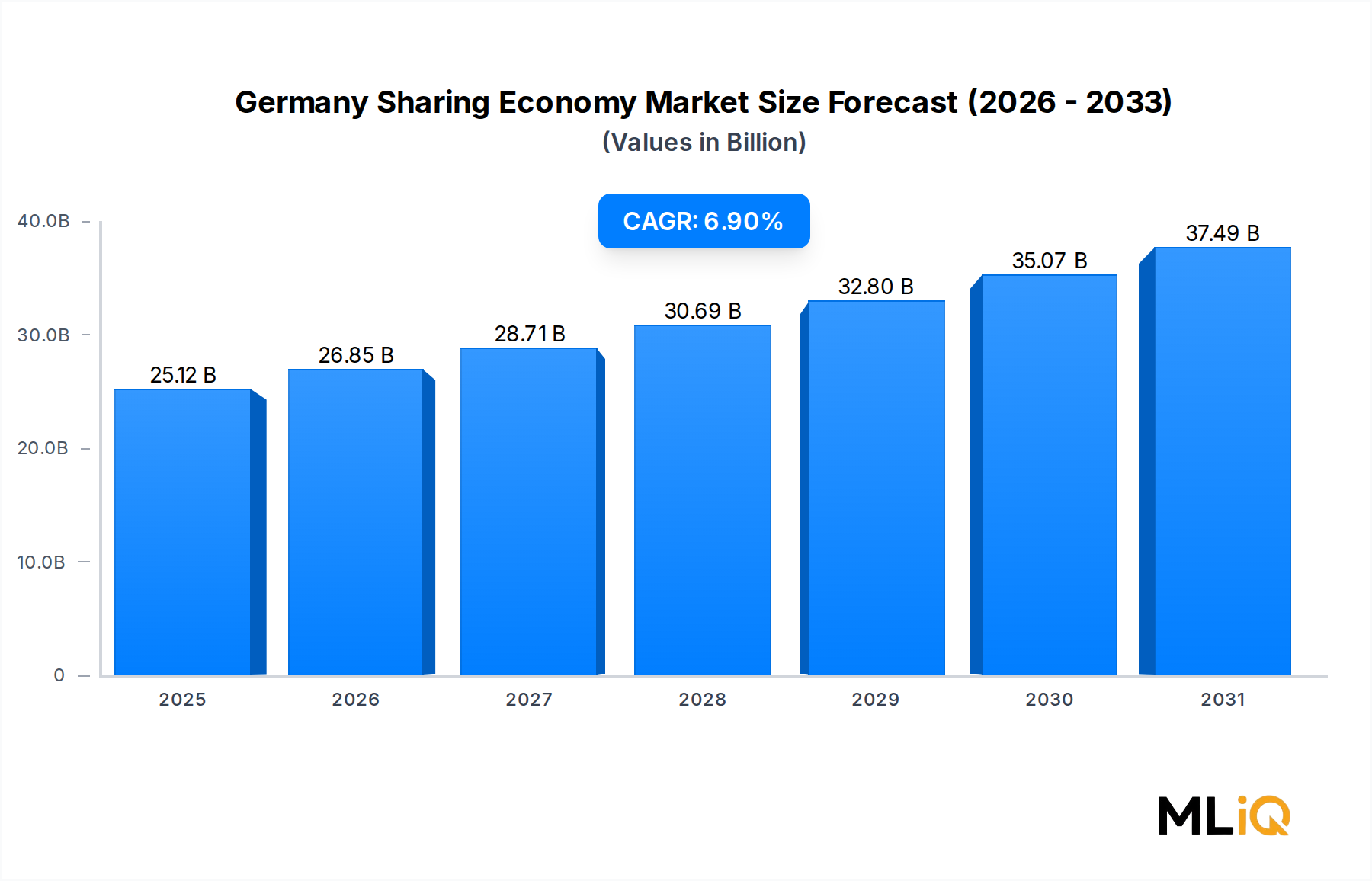

The Germany Sharing Economy Market is projected to reach a valuation of $25.12 billion by 2033, expanding at a compound annual growth rate (CAGR) of 6.9% during the forecast period from 2025 to 2033. Germany, as Europe's largest economy, has positioned itself as one of the most dynamic sharing economy ecosystems globally, underpinned by robust digital infrastructure, high smartphone penetration, and a culturally ingrained disposition toward sustainability and resource efficiency.

The market's growth trajectory is anchored by several intersecting macro tailwinds. First, urbanization continues to intensify in cities such as Berlin, Munich, Hamburg, and Frankfurt, driving demand for asset-light service models spanning transportation, accommodation, and financial services. Second, generational shifts in consumption preferences — particularly among Millennials and Generation Z — have accelerated adoption of access-over-ownership models. These demographic cohorts collectively represent more than half of the active participants in Germany's sharing platforms.

Digital trust infrastructure has matured considerably, with German consumers demonstrating heightened confidence in platform-mediated transactions, supported by GDPR-compliant data handling and transparent user rating systems. This has especially benefited accommodation and transportation sub-segments, which together account for the lion's share of market revenues.

On the macroeconomic front, rising cost-of-living pressures across German metropolitan areas are prompting households to monetize underutilized assets — from cars and spare rooms to consumer electronics and financial capital — generating supply-side dynamism that reinforces market liquidity. The convergence of the Platform Economy Market and the sharing model has further enabled hyper-efficient matchmaking between asset owners and consumers.

Sustainability policy remains a powerful demand driver. Germany's Climate Action Programme and its ambitious 2045 carbon neutrality goal have created a regulatory environment that actively incentivizes shared mobility and collaborative consumption patterns. The federal government's support for public transport integration and multimodal mobility hubs has amplified the appeal of transportation sharing services.

Looking ahead, the market is expected to evolve toward greater vertical integration, with leading platforms diversifying service portfolios and leveraging artificial intelligence for dynamic pricing, demand forecasting, and fraud detection. The proliferation of 5G connectivity across German urban and peri-urban zones will further reduce transaction friction. With a well-developed logistics network, a highly educated workforce, and a regulatory framework that balances innovation with consumer protection, the Germany Sharing Economy Market is positioned for sustained, structurally sound expansion through 2033.

Among all segments within the Germany Sharing Economy Market, Sharing Transportation commands the largest revenue share, a position it has maintained over multiple consecutive years and one that shows no sign of relinquishing as new entrants and incumbent players alike continue to invest heavily in fleet expansion and technology integration.

The transportation sharing segment encompasses car-sharing, ride-hailing, scooter-sharing, bike-sharing, and multimodal mobility platforms. Car-sharing alone accounts for a disproportionately large portion of segment revenues, driven by Germany's historically strong automotive culture being reinterpreted through the lens of collaborative access. Germany hosts one of Europe's densest networks of shared vehicles, with major metropolitan areas boasting station-based and free-floating schemes that serve millions of registered users.

Several structural factors explain the segment's dominance. Germany's high vehicle ownership costs — including insurance, maintenance, fuel, and increasingly, parking — make car-sharing economically attractive, particularly for urban dwellers who require a vehicle intermittently rather than daily. Studies indicate that a single shared car in a German city can replace between eight and twelve privately owned vehicles, underscoring the asset utilization efficiency that underpins the model's value proposition.

From a demand perspective, Millennials represent the highest-volume user cohort within transportation sharing, driven by environmental consciousness, digital fluency, and a preference for flexibility over long-term asset commitment. Generation Z is rapidly closing the gap, with mobile-first booking behaviors and a near-zero psychological attachment to vehicle ownership accelerating their uptake of shared mobility services.

The competitive landscape within transportation sharing is notably concentrated among a handful of well-capitalized operators. MyWheels operates as a cooperative-style platform connecting private car owners with renters, fostering community trust and expanding accessible inventory without capital-intensive fleet ownership. Flinkster, operated by Deutsche Bahn, integrates car-sharing seamlessly with Germany's rail network, offering multimodal journey planning that reduces dependence on private vehicles. Car2Go, subsequently rebranded into Share Now after the merger between Daimler and BMW's mobility units, pioneered free-floating car-sharing in Germany and remains a flagship operator in major cities. Cambio provides station-based car-sharing across multiple German cities, particularly strong in Cologne, Bremen, and Hamburg.

The segment is also witnessing a critical strategic pivot toward electrification. Fleet operators are progressively replacing internal combustion engine vehicles with battery electric vehicles, catalyzed by Germany's national EV incentive frameworks and the growing availability of charging infrastructure. This transition aligns car-sharing operators with Germany's decarbonization agenda and reduces long-run operating costs, though it requires substantial upfront capital investment.

Scooter and micro-mobility sharing have emerged as high-growth sub-segments within transportation sharing, particularly for last-mile connectivity in dense urban cores. Regulatory frameworks governing e-scooter operations in German cities — including maximum speeds, designated parking zones, and licensing requirements — have matured sufficiently to provide operational predictability for platform operators.

Overall, the Sharing Transportation segment's dominance is both structural and durable. Its integration with public transport networks, alignment with Germany's environmental policy priorities, and appeal across multiple demographic cohorts ensure it will continue to attract the largest share of investment, regulatory attention, and consumer adoption within the Germany Sharing Economy Market through the forecast horizon.

The Germany Sharing Economy Market is influenced by a distinct set of quantifiable drivers and constraints that collectively determine its growth velocity and structural depth.

Driver: Digital Infrastructure Penetration. Germany's internet penetration rate exceeds 90% of the population, and smartphone ownership surpasses 85%, creating a near-universal addressable market for platform-based services. Mobile app transaction volumes across sharing platforms have grown at double-digit rates annually, reducing onboarding friction and enabling real-time asset matching at scale.

Driver: Environmental Policy Mandates. Germany's Federal Climate Change Act (Klimaschutzgesetz) mandates a 65% reduction in greenhouse gas emissions by 2030 relative to 1990 levels. Shared mobility and collaborative consumption models directly contribute to emission reduction targets by maximizing asset utilization and reducing idle resource consumption. This policy alignment effectively subsidizes demand for sharing economy participation through behavioral incentives and, in some cases, direct subsidies.

Driver: Generational Consumption Shift. Millennials and Generation Z together constitute approximately 55% of active sharing economy platform users in Germany. These cohorts exhibit a statistically significant preference for subscription and access-based consumption over ownership, a trend quantified across multiple consumer sentiment surveys conducted between 2021 and 2024.

Constraint: Regulatory Fragmentation. Germany's federal structure results in significant variation in sharing economy regulations across its sixteen states (Bundesländer). Short-term rental regulations, for instance, differ substantially between Berlin, Bavaria, and Hamburg, creating compliance complexity that increases operational costs for accommodation-sharing platforms and discourages market entry by smaller operators.

Constraint: Data Privacy Compliance Costs. GDPR compliance represents a non-trivial cost burden for sharing economy platforms operating in Germany. Smaller platforms report allocating between 8% and 12% of operating budgets to data governance, legal compliance, and cybersecurity — costs that disproportionately disadvantage startups relative to established incumbents with dedicated compliance infrastructure.

Constraint: Trust Deficit in Niche Segments. While trust in mainstream sharing platforms is well-established, niche segments such as peer-to-peer tool sharing and collaborative finance continue to face adoption barriers linked to perceived counterparty risk, platform reliability concerns, and limited consumer awareness, constraining growth in otherwise high-potential sub-markets.

The Germany Sharing Economy Market is characterized by a diverse competitive ecosystem spanning mobility, accommodation, finance, and consumer goods rental verticals. Key players include:

MyWheels: A cooperative car-sharing platform that connects private vehicle owners with renters across Germany, emphasizing community trust and peer-reviewed reliability, making it a distinctive alternative to corporate fleet operators.

Fairmondo: Germany's cooperative online marketplace for ethical and sustainable goods sharing, positioning itself as a fair-trade alternative to mainstream e-commerce and rental platforms with a strong values-driven community.

Flinkster: Operated by Deutsche Bahn, Flinkster offers station-based car-sharing tightly integrated with Germany's rail network, enabling seamless multimodal travel planning and serving millions of registered users nationwide.

Wimdu GmbH: A Berlin-based vacation and short-term accommodation rental platform that competed in the peer-to-peer accommodation segment, building a significant European inventory before strategic consolidation reshaped the market.

DriveNow: A premium free-floating car-sharing service co-founded by BMW, which pioneered app-based vehicle rental in German cities and later merged into the Share Now platform as part of a broader mobility consolidation strategy.

Grover: A Berlin-headquartered consumer electronics rental and subscription platform enabling access-over-ownership for smartphones, laptops, and gaming hardware, serving both individual consumers and business clients across Germany and Europe.

Car2Go: The Daimler-backed free-floating car-sharing pioneer that launched in Germany and expanded across European and North American cities, setting foundational operational standards for the urban shared mobility sector before its consolidation into Share Now.

Cambio: A station-based car-sharing cooperative operating across multiple German cities with a strong presence in Cologne, Hamburg, and Bremen, known for transparent membership structures and reliable vehicle availability.

Otto Now: A consumer goods rental service enabling Germans to access appliances, electronics, and furniture on subscription or short-term rental terms, operating as an extension of the established Otto retail group's logistics and customer base.

Share Now: The merged entity of Car2Go and DriveNow, combining Daimler and BMW's mobility assets into Europe's largest free-floating car-sharing operator, with a progressively electrifying fleet and deep integration with urban mobility ecosystems across German cities.

January 2023: Share Now announced a significant fleet electrification milestone, with electric vehicles comprising over 30% of its German city fleet operations, aligning with municipal zero-emission zone requirements in Berlin and Munich.

March 2023: Grover secured a major debt financing round to expand its consumer electronics rental catalog in Germany, targeting the growing Consumer Electronics Rental Market segment with new product categories including e-bikes and smart home devices.

June 2023: The German Federal Ministry for Digital and Transport released updated regulatory guidance on e-scooter sharing operations, standardizing parking enforcement protocols across twelve major German cities and improving operational predictability for platform operators.

September 2023: Fairmondo launched an enhanced cooperative membership model, increasing profit-sharing provisions for platform participants and deepening its community governance structure in response to growing interest in ethical marketplace alternatives.

November 2023: Flinkster expanded its interoperability with Deutsche Bahn's BahnCard loyalty program, enabling seamless credit transfers between rail travel and car-sharing expenditures, a development expected to grow its registered user base by an estimated 15% within twelve months.

February 2024: Cambio announced the integration of real-time availability APIs with third-party urban mobility aggregator apps, broadening its market reach to users who do not engage directly with the Cambio native application.

May 2024: Germany's Bundestag passed updated platform liability provisions as part of the national Digital Markets Act transposition, introducing new requirements for sharing economy platforms regarding user verification, dispute resolution timelines, and income reporting transparency.

August 2024: MyWheels reported a 22% year-over-year increase in registered peer vehicle owners on its platform, reflecting growing supply-side participation driven by rising vehicle ownership costs across German urban centers.

While the Germany Sharing Economy Market is analyzed in the context of a single national geography, meaningful sub-regional differentiation exists across Germany's major economic corridors and metropolitan regions. Additionally, positioning Germany within its broader European and global competitive context provides critical strategic perspective.

Germany (Primary Market): Germany represents the dominant revenue contributor within the European sharing economy landscape, with its market valued at $25.12 billion by 2033 at a CAGR of 6.9%. Berlin leads as the most active city-level market, accounting for the highest density of sharing platform registrations, driven by a large young adult population, progressive local governance, and a startup-friendly ecosystem.

North America (Comparative Reference): The United States remains the world's largest sharing economy market by absolute value, with a market size several multiples that of Germany. However, Germany's regulatory maturity and sustainability alignment give it a differentiated growth profile. North American platforms frequently use Germany as a test market for European regulatory-compliant expansion strategies.

Europe (Adjacent Markets): The United Kingdom, France, and the Benelux countries represent Germany's closest peer markets within Europe. France has demonstrated particularly aggressive growth in urban mobility sharing, while the Nordics show high per-capita engagement with collaborative finance platforms, an area where Germany's Peer-to-Peer Lending Market is still maturing relative to Scandinavian counterparts.

Asia Pacific (High-Growth Reference): China and India represent the fastest-growing sharing economy markets globally, driven by massive urban populations and mobile payment ecosystem maturity. While not directly competitive with Germany's market, Asia Pacific platforms increasingly export technology and business model innovations that German operators adapt for local regulatory and cultural contexts.

Middle East & Africa (Emerging Segment): GCC nations, particularly the UAE and Saudi Arabia, are investing in sharing economy infrastructure as part of broader economic diversification strategies, representing potential partnership markets for German platform technology exporters operating in the Urban Mobility Market space.

Within Germany itself, Munich and Hamburg follow Berlin as the second and third most active markets respectively, with Munich showing the highest average transaction value per user due to elevated income levels and premium service preferences, while Hamburg demonstrates particular strength in maritime logistics and cargo sharing verticals unique to its port-city context.

The Germany Sharing Economy Market, while primarily a services and platform-mediated sector, maintains meaningful upstream dependencies on physical infrastructure, digital hardware, and energy inputs that introduce supply chain complexity and price volatility risks.

Digital Infrastructure Components: Sharing economy platforms depend critically on server hardware, semiconductor chips, and networking equipment to sustain real-time matching, geolocation services, and payment processing. The global semiconductor shortage of 2021–2023 demonstrated the vulnerability of platform operators that rely on in-house hardware for IoT-enabled asset tracking — a core technology for car-sharing and scooter-sharing fleet management. Chip prices remain elevated relative to pre-shortage baselines, increasing the cost of deploying connected vehicle technology and smart lock systems used in accommodation sharing.

Electric Vehicle Battery Supply Chain: As transportation sharing operators transition their fleets to electric vehicles, they become directly exposed to lithium, cobalt, and nickel price dynamics. Lithium carbonate prices experienced extreme volatility between 2021 and 2023, rising by over 500% before correcting sharply. This volatility affects the total cost of ownership calculations for EV fleets and, by extension, the pricing economics of car-sharing services. German fleet operators increasingly pursue long-term battery supply agreements to hedge against spot market exposure, with some exploring second-life battery programs to extend asset value.

Energy and Charging Infrastructure: The roll-out of Electric Vehicle Charging Infrastructure Market assets is a critical upstream dependency for electric car-sharing viability. Germany's charging network, while expanding, remains unevenly distributed between urban and rural zones. Energy price volatility — amplified by the post-2022 European energy market disruptions linked to geopolitical tensions — has directly impacted charging operating costs for shared EV fleet operators, squeezing per-kilometer margins.

Data Center Energy Consumption: Platform operators face growing cost pressure from data center energy expenses, particularly as AI-driven demand forecasting and dynamic pricing models increase computational load. Germany's industrial electricity prices rank among Europe's highest, creating a competitive disadvantage relative to platforms hosted in lower-cost jurisdictions,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Germany Sharing Economy Market market expansion.

Key companies in the market include MyWheels, Fairmondo, Flinkster, Wimdu GmbH, DriveNow, Grover, Car2Go, Cambio, Otto Now, Share Now.

The market segments include Type, End User.

The market size is estimated to be USD 25.12 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 3049, and USD 5107 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Germany Sharing Economy Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Germany Sharing Economy Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.