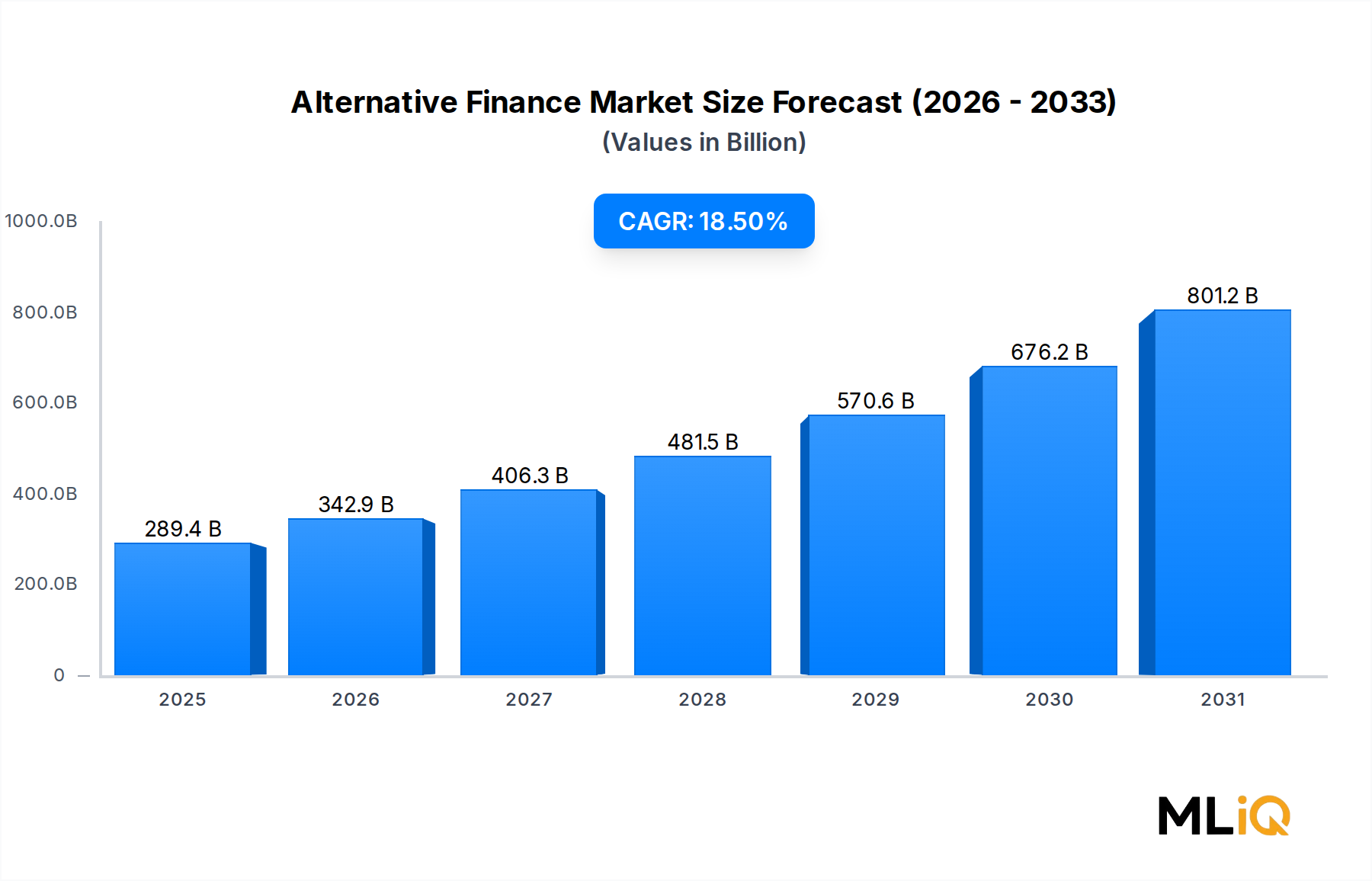

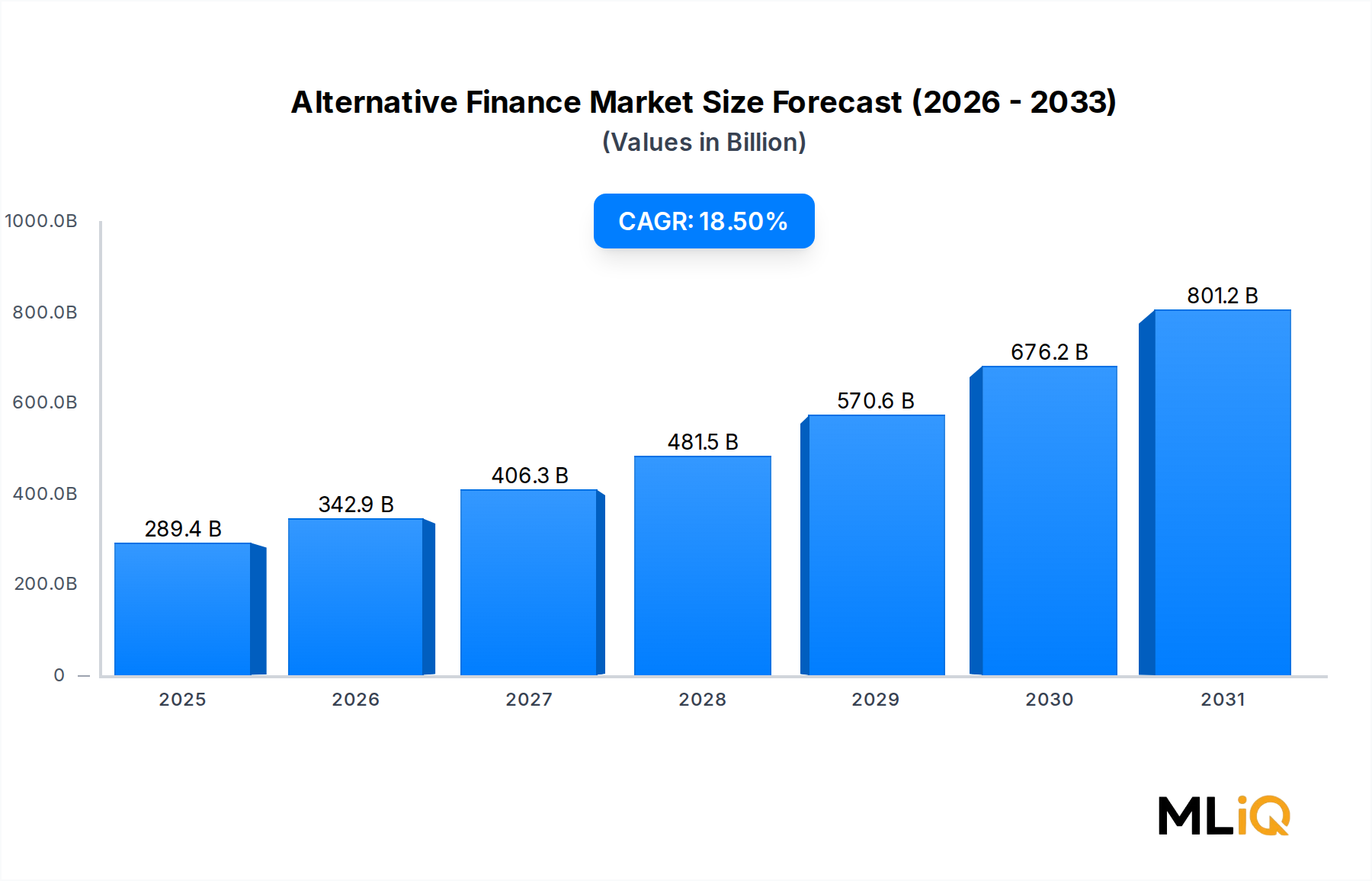

Peer-to-Peer Lending Dominance in the Alternative Finance Market

Within the Alternative Finance Market, Peer-to-Peer (P2P) lending commands the largest revenue share across the Type segmentation, consistently accounting for over 40% of total market volume in recent years. This dominance is not incidental — it reflects a structural alignment between platform mechanics, borrower demographics, investor appetite, and regulatory progressiveness that no other sub-segment has yet replicated at scale.

P2P lending operates by directly connecting borrowers with individual or institutional lenders through digital platforms, eliminating the intermediary cost layers inherent in traditional banking. This cost efficiency translates into competitive borrowing rates and superior investor yields, a dual value proposition that has proven remarkably resilient across economic cycles. Platforms in this space typically leverage proprietary credit-scoring algorithms that incorporate non-traditional data sources — transaction histories, behavioral analytics, social verification — enabling more granular risk segmentation than conventional credit bureaus allow.

LendingClub Bank, one of the most established players in the North American P2P lending ecosystem, has evolved from a pure marketplace model toward a hybrid bank-platform structure, acquiring Radius Bank to obtain a banking charter. This strategic pivot reflects a broader industry trend toward regulatory anchoring, allowing platforms to access cheaper capital, accept deposits, and offer a more comprehensive product suite. Similarly, Prosper Funding LLC has refined its institutional investor program, enabling bulk loan purchases that smooth liquidity cycles and reduce platform volatility.

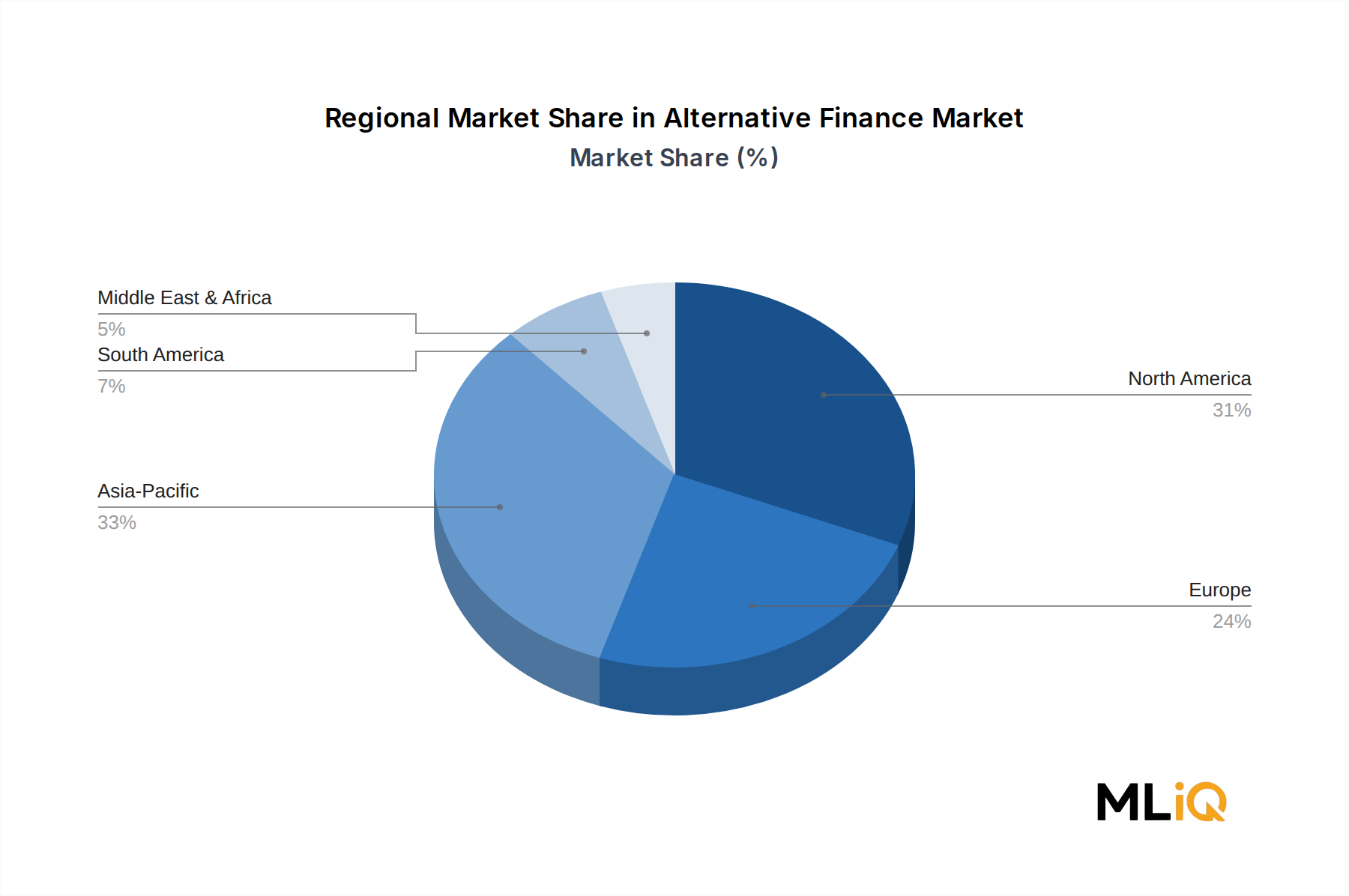

In Europe, Funding Circle Limited has carved out a dominant position in SME lending, operating across the United Kingdom, Germany, and the Netherlands. Its institutional-grade underwriting standards and government-backed loan program participation have positioned it as a quasi-institutional lender rather than a retail crowdfunding vehicle. Mintos, operating as a pan-European marketplace, aggregates loan originators from over 30 countries, offering investors diversified exposure to global credit instruments through a single interface — a model that has attracted over €700 million in investor capital.

The P2P lending segment is also witnessing consolidation, particularly in Asia Pacific, where regulatory tightening in China dramatically reduced the number of operating platforms from thousands to a handful of licensed entities post-2019. This regulatory pruning, while initially disruptive, has improved average platform quality and investor confidence, ultimately contributing to a more sustainable growth trajectory.

Institutional participation is reshaping the segment's investor base. Where P2P lending was initially consumer-driven, institutional investors now account for an estimated 60–75% of loan funding on major platforms in mature markets. This shift has compressed retail yields but introduced greater capital stability, reduced platform default exposure, and attracted secondary market infrastructure.

The Peer-to-Peer Lending Market intersects significantly with the broader Digital Lending Market, sharing technology infrastructure, compliance frameworks, and data partnerships. As open banking mandates expand globally, P2P platforms gain real-time access to verified financial data, further enhancing underwriting precision. The segment's share is expected to consolidate rather than decline, as smaller platforms either exit or merge with larger operators possessing the regulatory capital and technology investment capacity required to compete at scale.