Dominance of Reward-Based Crowdfunding in the Crowdfunding Market

Reward-based crowdfunding represents the single largest segment by revenue share within the global crowdfunding ecosystem, accounting for the majority of active campaigns and registered users across all major platforms. Its dominance is structural rather than cyclical, rooted in the model's low regulatory burden, broad accessibility to non-accredited participants, and its alignment with creator-economy dynamics that have reshaped consumer engagement since 2015.

Under the reward-based model, backers contribute funds in exchange for non-financial incentives — typically early access to products, branded merchandise, or experiential rewards. This architecture eliminates the legal complexities associated with securities issuance, enabling platforms to onboard campaign creators in virtually any jurisdiction without triggering investor protection statutes. The result is a dramatically lower cost-to-launch, which has historically attracted the highest campaign volume of any model type.

Kickstarter PBC remains the most recognizable global incumbent in this segment, having facilitated billions in pledged funding since its 2009 inception. Its brand equity, curated creative community, and all-or-nothing funding mechanism create strong network effects that reinforce platform stickiness. Indiegogo, Inc. offers a more flexible model — allowing campaign creators to retain funds even if targets are not met — which has broadened its appeal to hardware and social-impact verticals. GoFundMe, while more closely associated with personal and charitable fundraising, also operates within the broader reward-adjacent donation-based spectrum, commanding exceptional brand recall among individual users globally.

The segment's dominance is simultaneously consolidating and evolving. Consolidation is evident in the market share concentration among the top three to five platforms, which collectively capture the vast majority of transactional volume. Smaller niche platforms focused on music, film, or community arts are increasingly struggling to achieve the liquidity thresholds needed to sustain network effects, leading to platform exits and acqui-hire activity.

Evolution, however, is keeping the segment dynamic. Integration with social commerce platforms — including direct API linkages with Instagram, TikTok, and YouTube — has reduced customer acquisition costs for reward-based campaigns by enabling organic viral distribution. The average campaign discovery cycle has compressed materially, shifting from weeks to days in high-engagement categories such as consumer electronics and gaming.

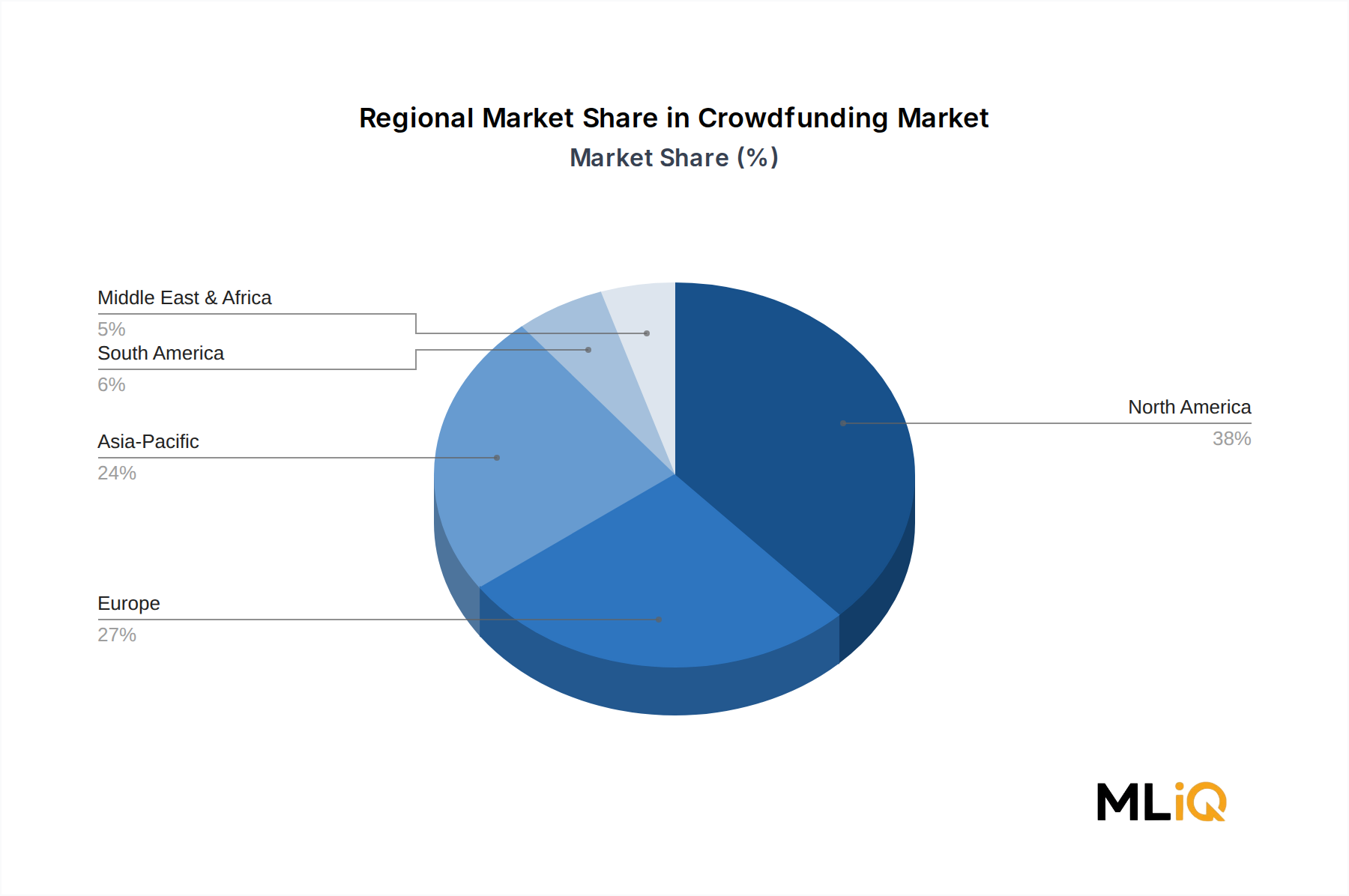

From a geographic standpoint, North America and Western Europe remain the revenue epicenters of reward-based crowdfunding, but Asia-Pacific is rapidly closing the gap. Platforms localizing for Japanese, South Korean, and Indian markets have recorded compounding growth in campaign creation rates, supported by the expansion of the Online Fundraising Market and integration with domestic digital payment rails.

The segment's revenue model — typically a percentage fee on successfully funded campaign totals, supplemented by payment processing revenue — generates attractive operating leverage at scale. Leading platforms are progressively layering in premium services such as analytics dashboards, backer relationship management tools, and white-label hosting to expand per-campaign revenue and reduce dependency on volume alone. This margin diversification positions reward-based crowdfunding for sustained share leadership even as equity and debt-based models post higher percentage growth rates.