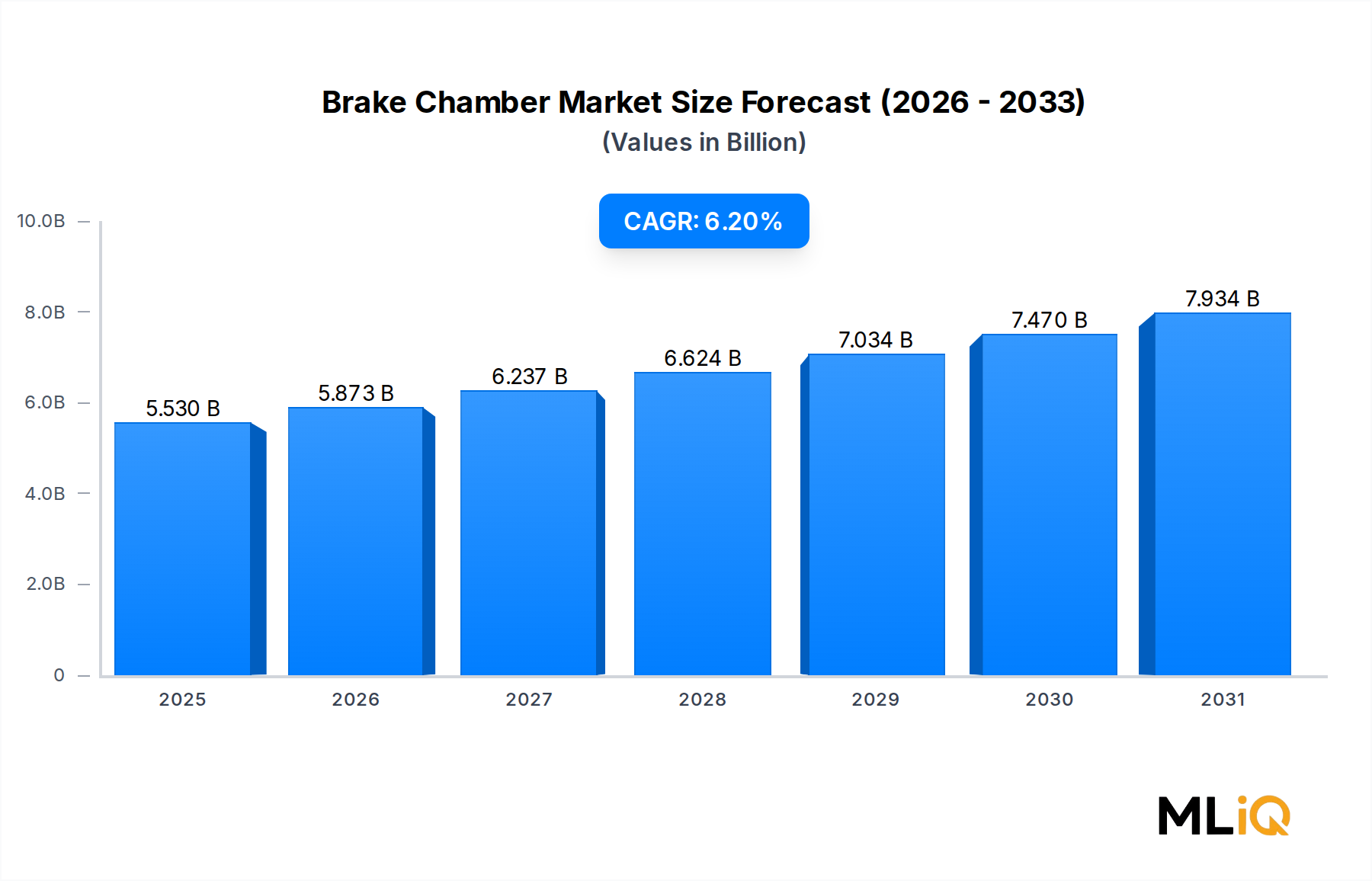

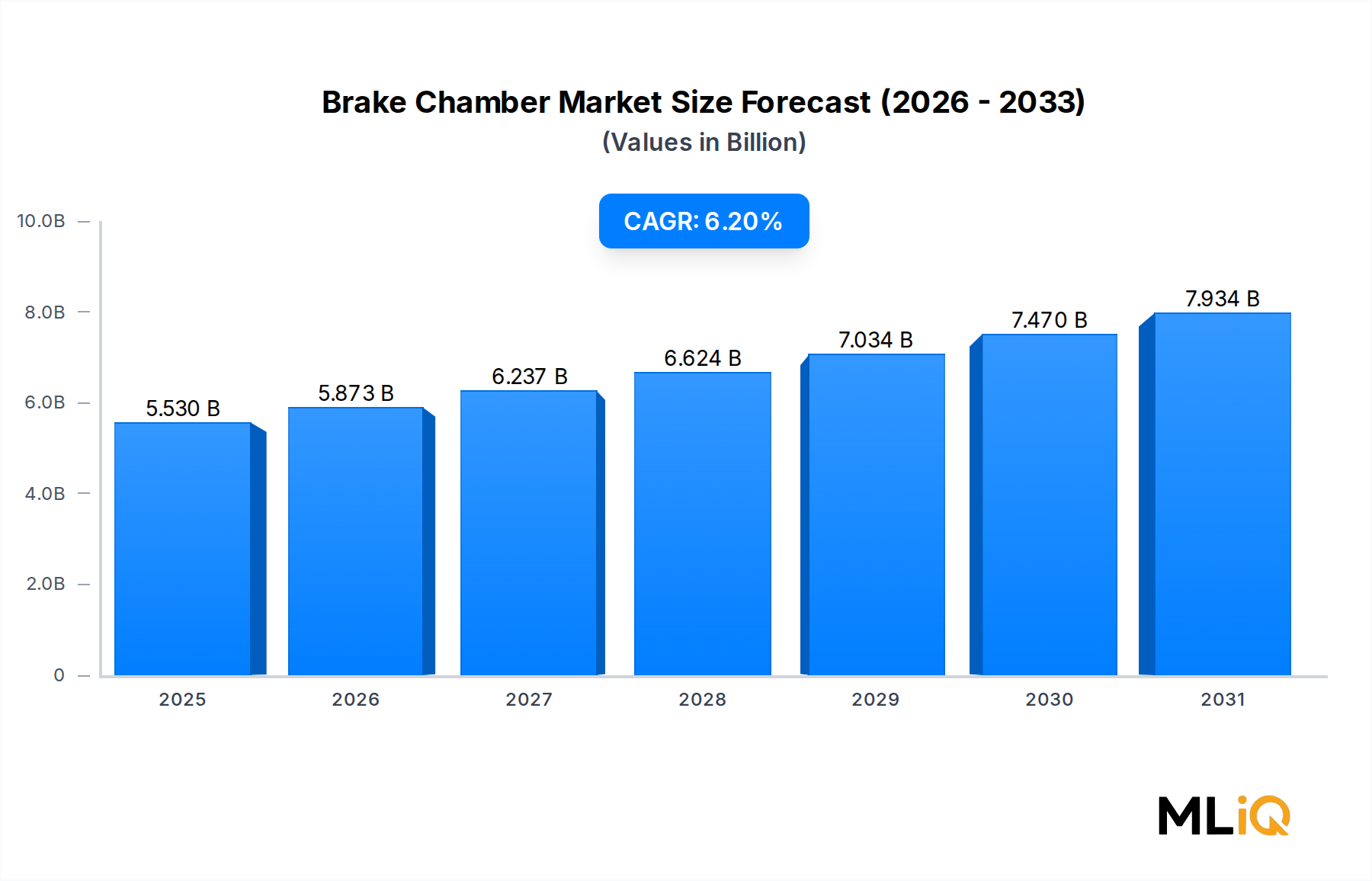

Spring Brake Chamber Dominance in the Brake Chamber Market

Within the Brake Chamber Market, the Spring Brake Chamber Market segment commands the largest revenue share, consistently accounting for an estimated 60–65% of total market value. This dominance is driven by regulatory requirements, functional versatility, and universal OEM adoption across heavy- and medium-duty truck platforms globally.

Spring brake chambers are dual-function units that integrate both the service brake and the spring-actuated parking/emergency brake into a single housing, commonly referred to as a "piggyback" configuration. When air pressure is lost — whether due to line failure, vehicle shutdown, or emergency conditions — the internal spring automatically applies the brake, providing a fail-safe mechanism mandated by vehicle safety codes in virtually every major market. This intrinsic safety design is the primary reason spring brake chambers have displaced standalone service-only chambers in the heavy-duty segment.

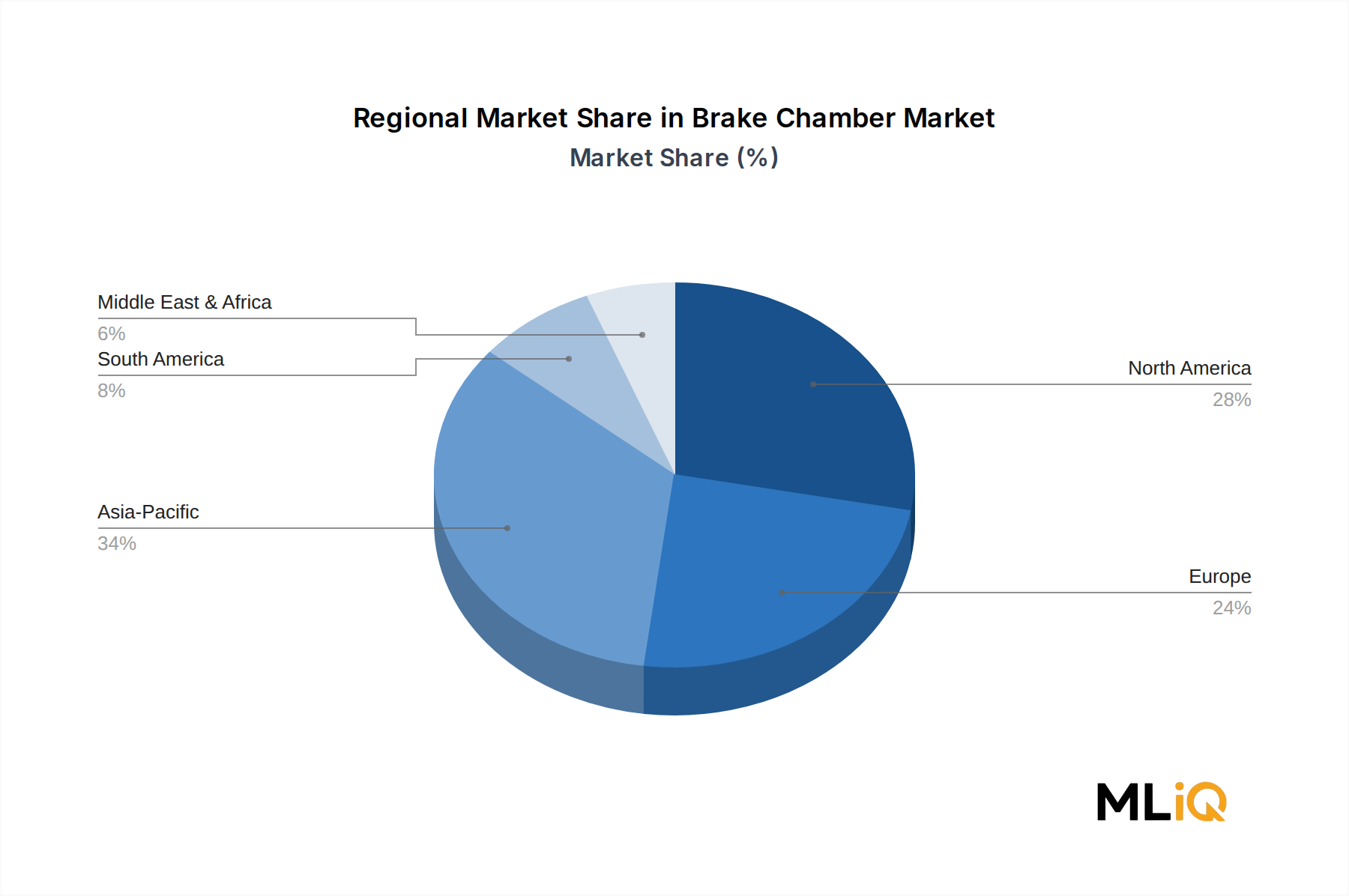

From a regulatory standpoint, FMVSS 121 in the United States and equivalent ECE R13 regulations in Europe require that all vehicles above specified Gross Vehicle Weight Ratings (GVWR) incorporate spring-actuated parking brake systems. This creates a structural, non-discretionary demand floor that insulates the spring brake chamber sub-segment from cyclical downturns to a greater degree than lighter vehicle components.

The functional superiority of spring brake chambers is also reflected in their performance envelope. Modern units are engineered to deliver consistent actuation force across temperature ranges from -40°C to +120°C, resist corrosion from road salt and moisture, and maintain seal integrity across pressure cycles exceeding 1 million actuations. These specifications align with the operational demands of long-haul trucking, where brake reliability directly affects driver safety and cargo security.

Key players within this sub-segment include Bendix Commercial Vehicle Systems, which offers its premium TufTrac and NeverSeize spring brake chamber lines featuring anti-corrosion housing treatments; Knorr-Bremse AG, which integrates spring brake chamber technology with its EBS (Electronic Braking System) platform for seamless data communication; and WABCO Holdings Inc., whose spring brake chambers are specified by major OEMs including Daimler Truck, Volvo Trucks, and PACCAR. Haldex AB and TSE Brakes, Inc. serve as significant secondary suppliers, particularly in the North American aftermarket.

The spring brake chamber segment's share is not only large but also consolidating. As vehicle platforms move toward higher integration — with brake management ECUs communicating directly with actuation hardware — OEMs are increasingly standardizing on spring brake chamber designs from Tier 1 suppliers who can provide both hardware and embedded software calibration data. This raises the barrier to entry for commodity suppliers and reinforces the dominance of established players.

In the medium-duty truck sub-segment, spring brake chambers are gaining penetration that was historically held by hydraulic-assisted braking systems, particularly in markets where pneumatic system costs have declined due to manufacturing scale. This lateral expansion adds incremental volume to an already dominant segment.

Aftermarket dynamics further reinforce spring brake chamber leadership. Fleet maintenance schedules in North America call for diaphragm inspection at 100,000-mile intervals and full chamber replacement at 250,000–350,000 miles, creating predictable replacement streams. With the average U.S. Class 8 truck operating for 700,000–1,000,000 miles over its service life, each vehicle generates two to three spring brake chamber replacement cycles, compounding market volume well beyond new vehicle production figures.