Spices Segment Dominance in the Seasoning And Spices Market

Within the Seasoning And Spices Market, the Spices sub-segment commands the largest revenue share and serves as the structural backbone of the overall industry. Comprising whole, crushed, and ground variants of products such as black pepper, turmeric, cumin, chili, coriander, and cardamom, the spices category benefits from universal applicability across geographies, cuisines, and end-use channels. Its dominance is rooted in both cultural necessity and functional utility — spices fulfill simultaneous roles as flavor agents, colorants, and preservatives, making them indispensable to food manufacturing and household cooking alike.

The spices sub-segment's share is reinforced by its deep penetration into the industrial food processing sector. Manufacturers of meat and poultry products, soups, sauces, dressings, and frozen food formulations depend heavily on standardized spice inputs to achieve consistent flavor profiles at scale. The expansion of the Processed Food Market globally has therefore acted as a direct demand amplifier for the spices category. As ready-to-eat and ready-to-cook product lines proliferate across both developed and emerging economies, sourcing volumes for spice inputs are growing commensurately.

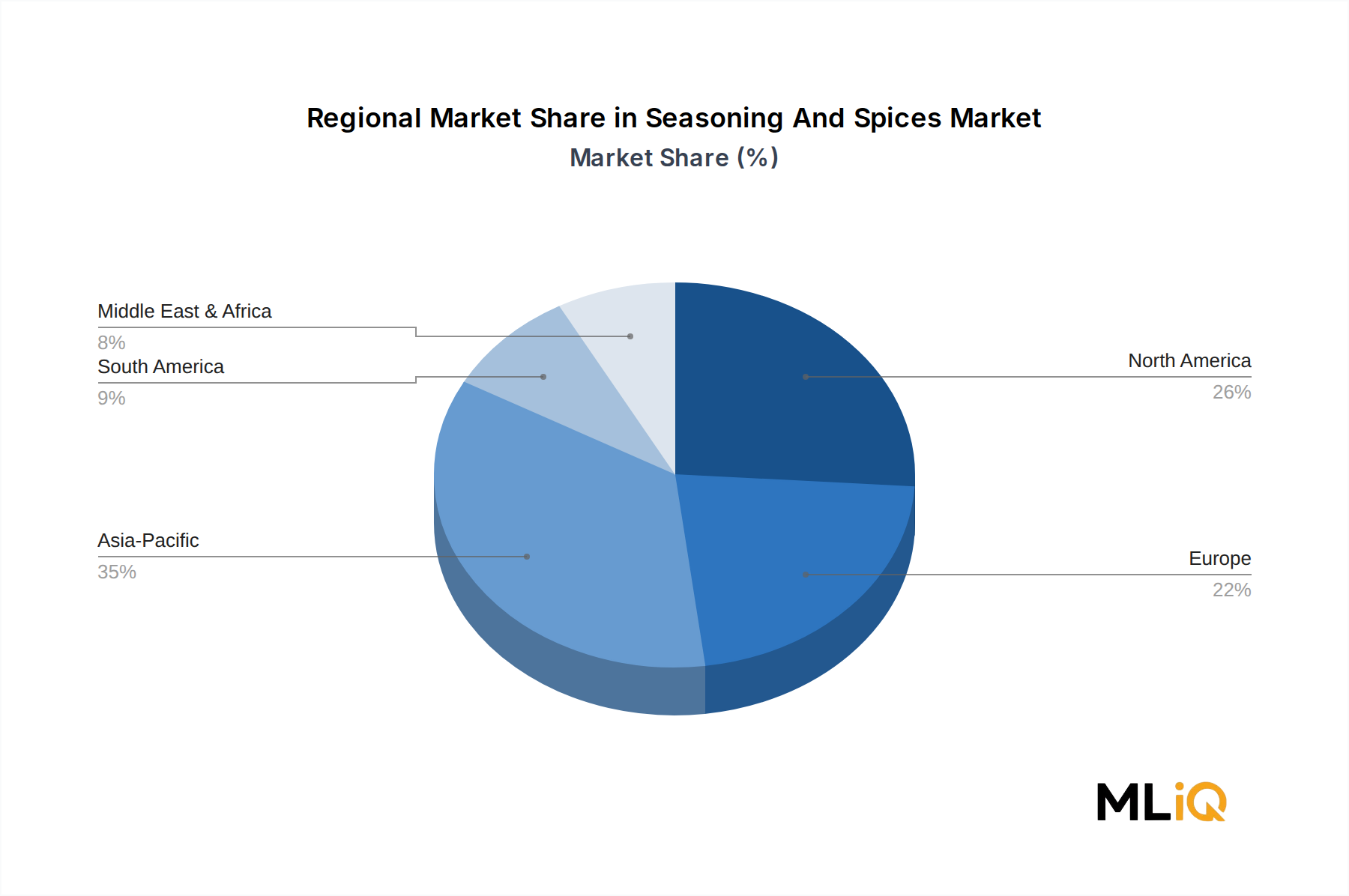

From a geographic production standpoint, India remains the world's largest producer, consumer, and exporter of spices, accounting for a disproportionate share of global supply for turmeric, chili, and cumin. Vietnam leads global black pepper production, while Indonesia and Madagascar are dominant suppliers of nutmeg and vanilla, respectively. This geographic concentration creates supply-side resilience risks, which have become a recurring boardroom concern for multinational food companies.

Key players operating with particular strength in the spices sub-segment include McCormick & Company, Inc, which maintains one of the broadest global portfolios of branded and private-label spice products, and Olam International Limited, which operates an integrated supply chain from farm-level procurement to value-added processing and distribution. Mahashian Di Hatti Private Limited holds a commanding position in the Indian domestic spice market with its MDH brand, while Ariake Japan Co., Ltd. has developed proprietary extraction and processing technologies that allow it to supply high-purity spice-derived flavor compounds to industrial clients in Asia and beyond.

The segment's revenue share is not just holding steady — it is gradually consolidating, driven by three intersecting dynamics. First, private-label spice programs from hypermarket and supermarket chains are expanding, capturing price-sensitive consumer segments while maintaining volume growth. Second, the emergence of ethnic cuisine as a mainstream preference in North America and Western Europe is broadening the addressable category for spices historically considered niche. Third, functional food trends are elevating the profile of spices with documented health attributes — turmeric's curcumin content, for instance, is driving a crossover between the spice category and the nutraceutical sector, creating premium product tiers that command higher margins.

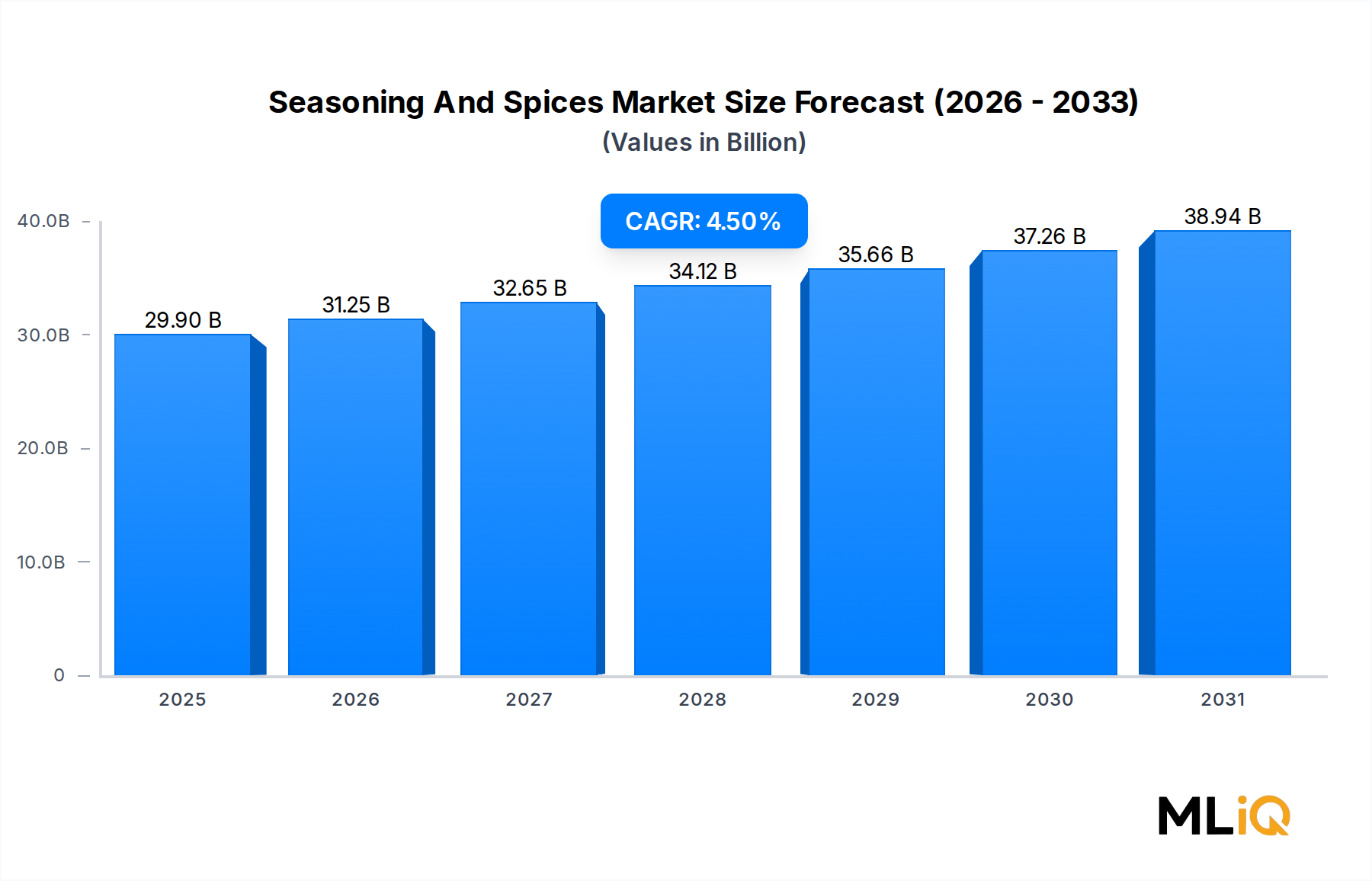

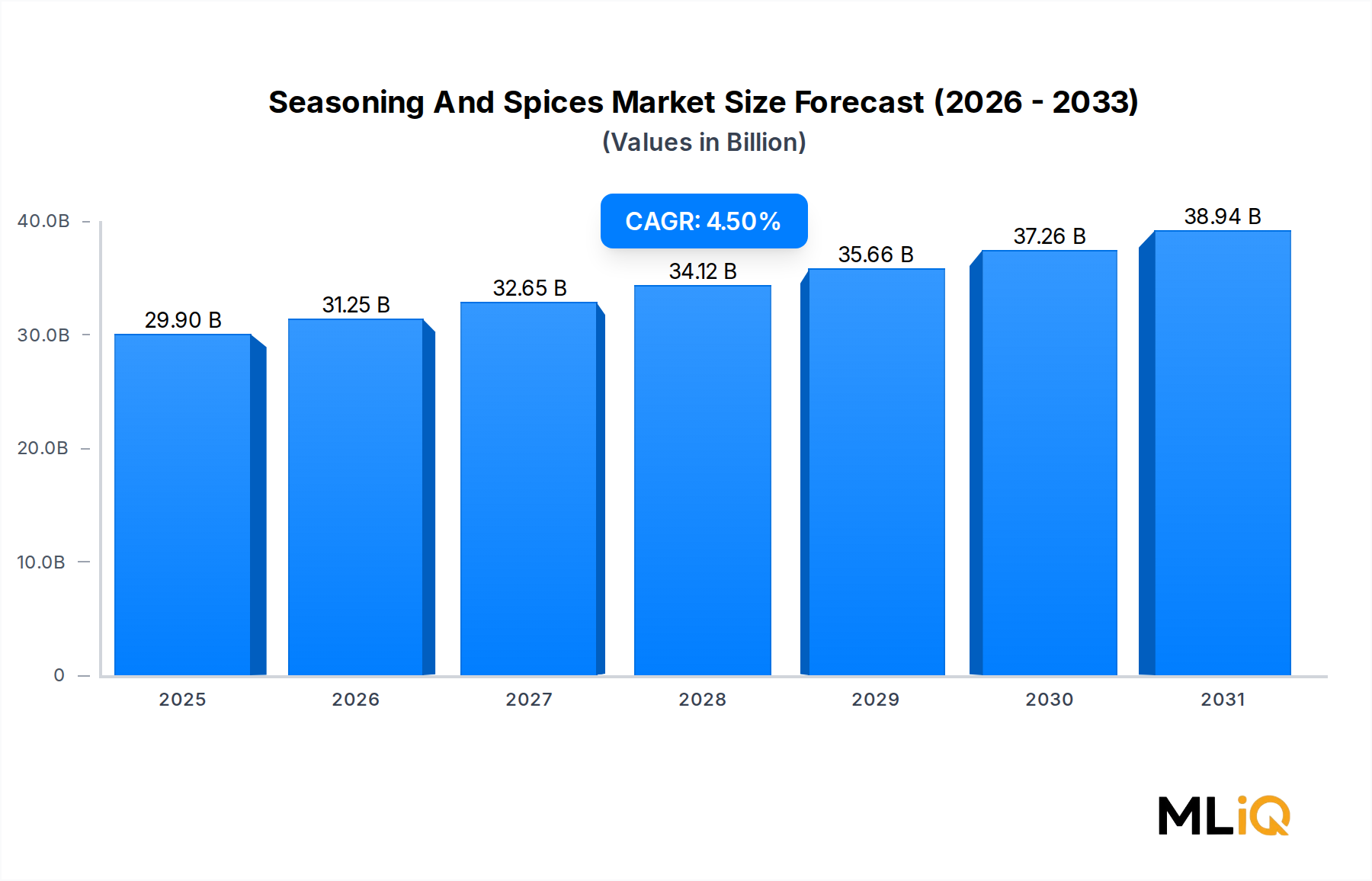

Overall, the spices sub-segment is expected to maintain its dominant position throughout the forecast period, growing at a pace slightly above the overall market CAGR of 4.5%, supported by both volume and pricing tailwinds.