Demand Modeling & Market Estimation

Market sizing and forecasting for the Automotive RADAR Market (2026–2034) were executed using a dual-methodology framework combining top-down and bottom-up approaches, validated through multi-level data triangulation.

Top-Down Approach: Global automotive production volumes (sourced from OICA and NHTSA) were used as the macro-level denominator. ADAS penetration rates by vehicle segment and region were layered onto these volumes, with regulatory mandates (e.g., EU GSR 2022 AEB requirements) used to establish minimum adoption floors. RADAR attachment rates per vehicle (differentiated by LRR and S&MRR configurations) were then applied to derive addressable unit volumes, which were subsequently monetized using average selling price (ASP) benchmarks.

Bottom-Up Approach: Revenue was constructed from the component level upward using the following specific metrics and variables:

- RADAR Unit ASP by Frequency Band — Differentiated ASPs for 24 GHz (legacy BSD), 77 GHz (ACC/AEB LRR), and 79 GHz (high-resolution imaging RADAR) modules, sourced from Tier-1 supplier contract disclosures and procurement manager interviews

- RADAR Sensors per Vehicle by Automation Level — Average number of RADAR modules installed per vehicle platform, segmented by SAE Level 1–2 (1–3 sensors) versus Level 2+ (3–6 sensors), used to calculate per-vehicle RADAR content value

- OEM ADAS Fitment Rate by Region & Vehicle Class — The percentage of new vehicles in each region (North America, Europe, Asia Pacific, MEA, South America) equipped with factory-fitted ACC, AEB, or BSD systems, disaggregated by passenger car vs. commercial vehicle

- RADAR IC & Component Bill of Materials (BoM) Cost Breakdown — Granular cost decomposition including MMIC chipset cost, PCB and antenna array cost, radome, and ECU integration cost, used to validate ASP assumptions and gross margin trajectories through 2034

Multi-Level Data Triangulation: All demand model outputs were cross-validated against: (1) primary interview-derived volume and revenue estimates from Tier-1 and OEM stakeholders; (2) regulatory fitment mandates and compliance deadlines; and (3) financial disclosures from publicly listed RADAR system suppliers. Discrepancies exceeding ±8% between model layers were resolved through additional expert consultation rounds.

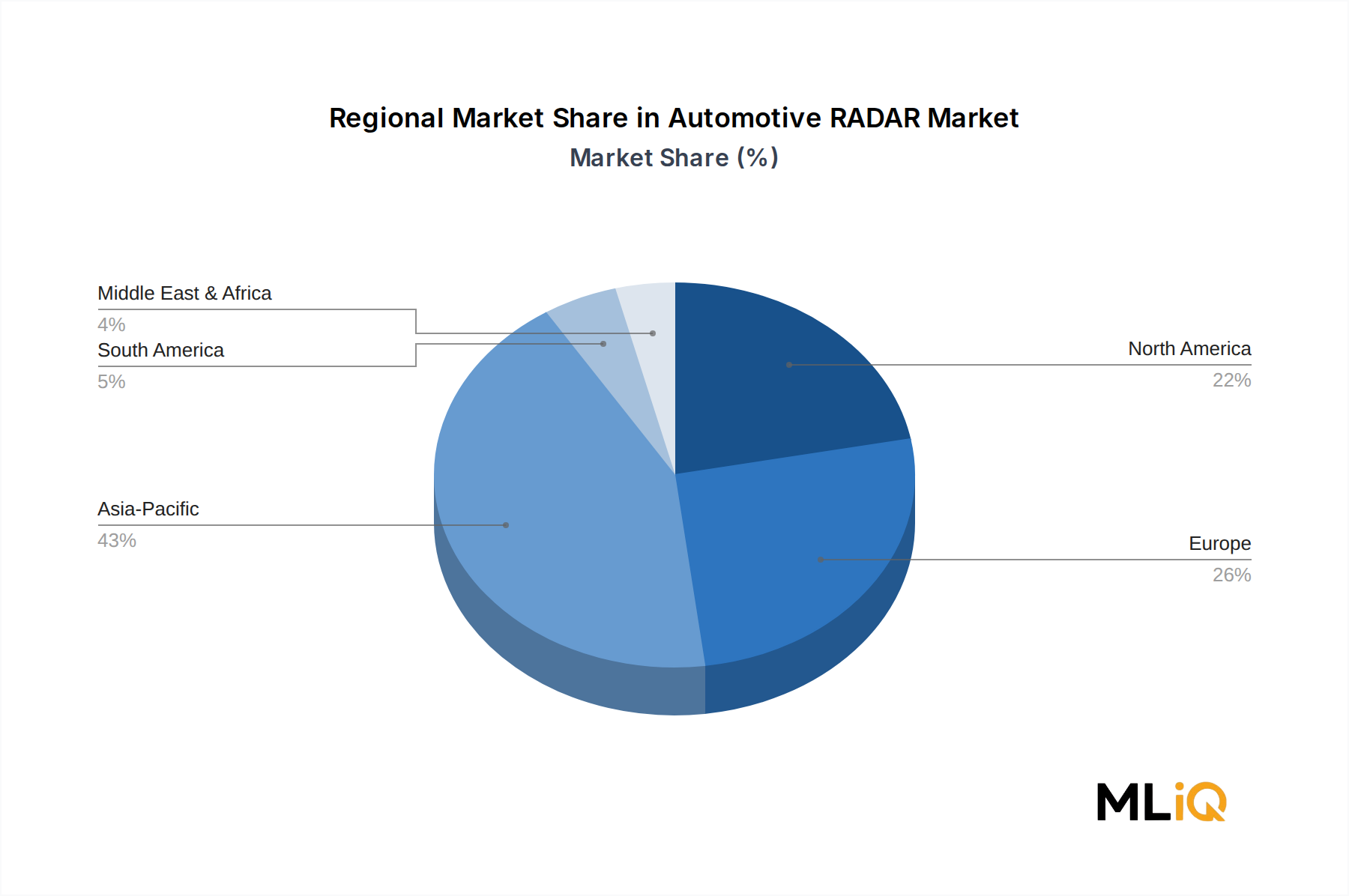

Regional forecasts for North America (U.S., Canada, Mexico), South America (Brazil, Argentina, Rest of South America), Europe (UK, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of MEA), and Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of APAC) were independently modeled using region-specific vehicle production data, regulatory calendars, and ADAS adoption curves before being aggregated into global totals.