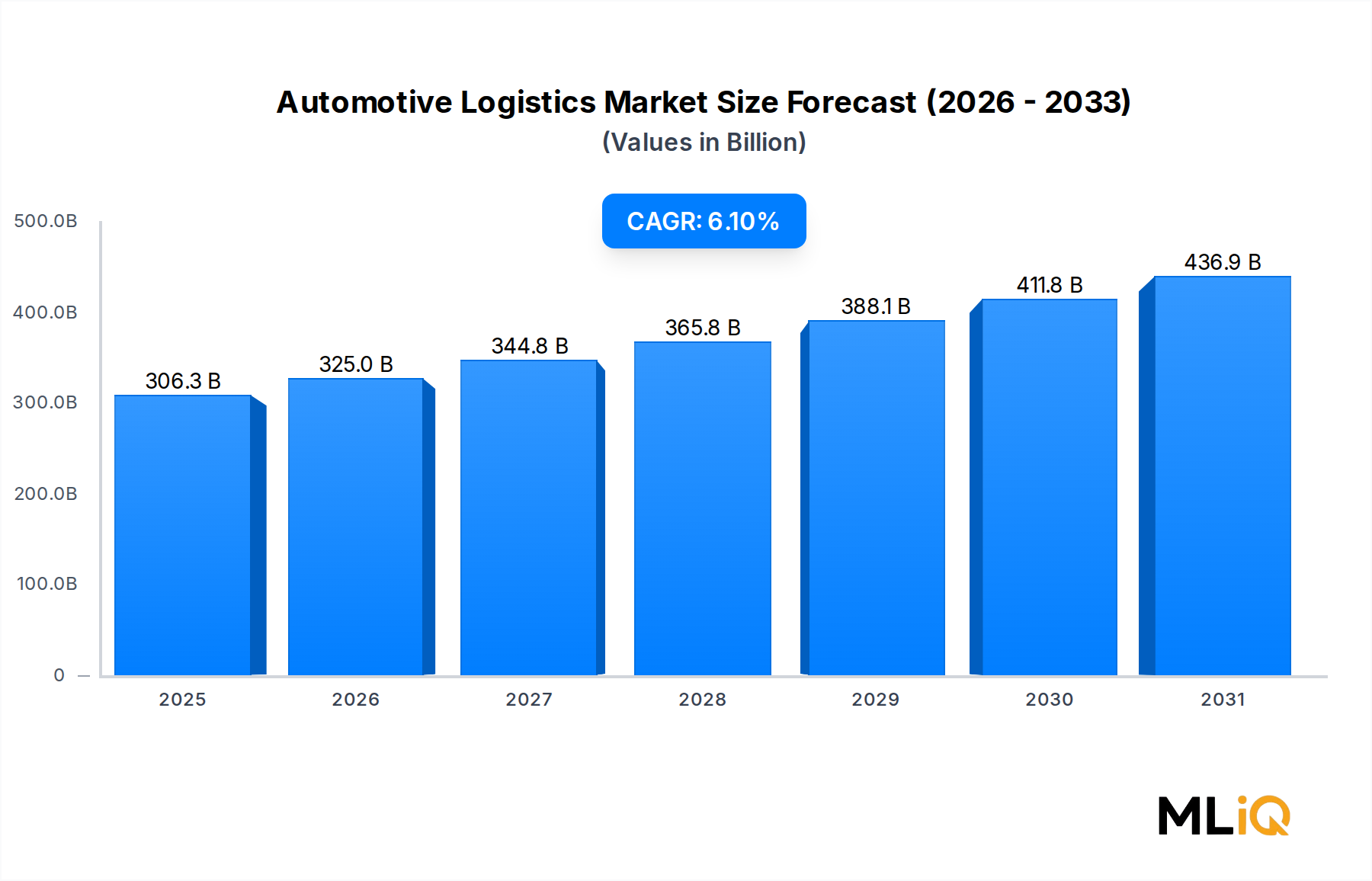

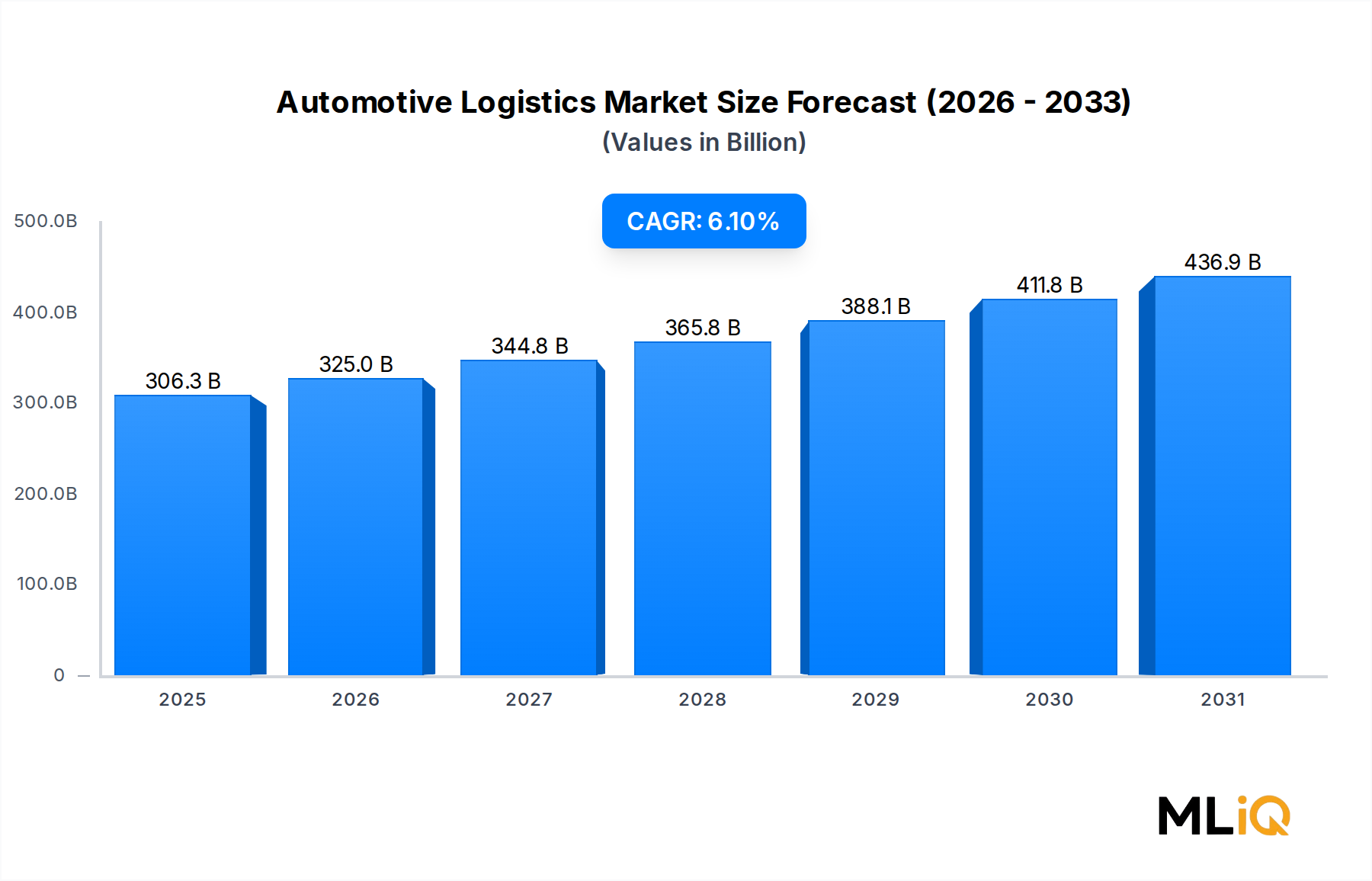

Transportation Segment Dominance in the Automotive Logistics Market

Within the service segmentation of the Automotive Logistics Market, transportation stands as the single largest revenue-generating category, consistently accounting for the majority share of total market value. This dominance reflects the fundamental nature of automotive logistics itself: every vehicle manufactured and every component sourced must physically traverse geographic distances before reaching its end destination, whether that is a dealership forecourt, an assembly plant, or an aftermarket distribution hub.

The transportation segment encompasses a diverse array of modal solutions, including road transport via car-carrier trucks and flatbed trailers, rail transport using specialized auto-rack wagons, ocean freight through roll-on/roll-off (RoRo) vessels and container shipping, and air freight for time-sensitive components. The inherent multi-modality of automotive supply chains ensures that transportation services remain mission-critical regardless of fluctuations in production volumes or inventory strategies.

Finished vehicle transportation represents a particularly capital-intensive sub-segment, requiring specialized rolling equipment such as enclosed multi-deck carriers and port processing facilities capable of storing and inspecting thousands of vehicles simultaneously. Port operators in Germany (Bremerhaven), South Korea (Pyeongtaek), Japan (Nagoya), and the United States (Port of Baltimore) function as pivotal nodes in the global finished-vehicle distribution network. The Vehicle Shipping Market, a closely adjacent sector, further amplifies demand for specialized ocean-going RoRo capacity, with leading shipping lines investing in larger, more fuel-efficient vessels to reduce per-unit transportation costs.

For automotive parts and components, transportation complexity is even more pronounced. Just-in-time (JIT) and just-in-sequence (JIS) manufacturing philosophies, pioneered by Japanese OEMs and now universally adopted across the industry, place extreme demands on the reliability, punctuality, and frequency of inbound delivery schedules. A single missed delivery of a critical component can halt an entire assembly line, generating losses that dwarf the cost of the component itself. This dynamic incentivizes OEMs to enter long-term contracts with transportation providers that can guarantee service-level agreements and offer contingency routing options.

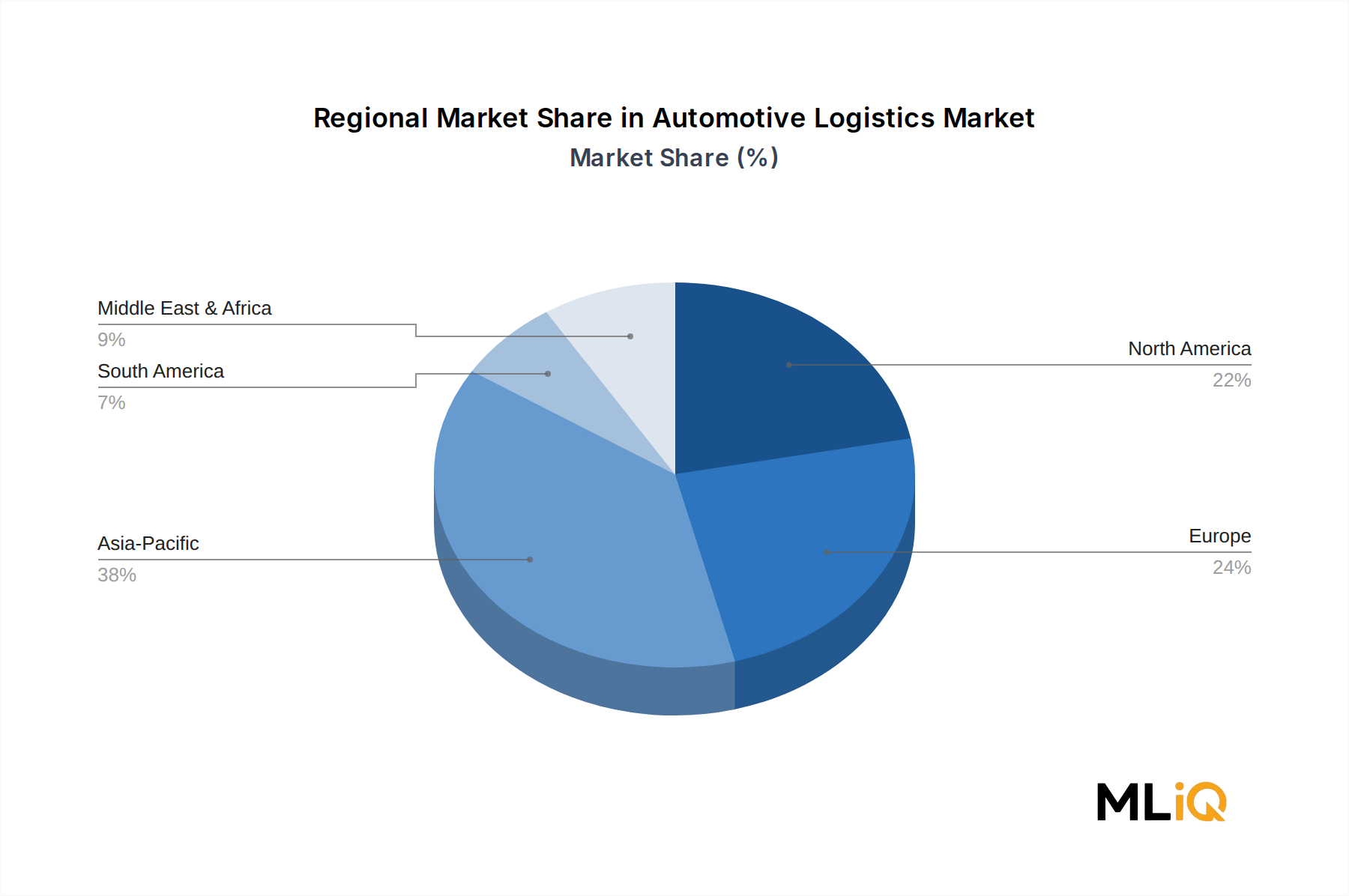

The mode-of-transport breakdown reveals that land transportation — road and rail combined — commands the largest share of volume movements globally, reflecting the short-haul nature of most inbound parts flows and the dense road network connecting Tier-1 suppliers to assembly plants in Europe, North America, and China. Air freight, while volumetrically small, is disproportionately valuable, serving emergency supply situations and supporting the rapid distribution of high-value electronic modules and semiconductor components. Sea transport dominates intercontinental flows, particularly for finished vehicles moving from export hubs in Japan, Germany, South Korea, and China to import markets in the United States, Australia, and the Middle East.

Key players driving growth within the transportation segment include Deutsche Post DHL Group, Kuehne+Nagel International AG, DSV A/S, and A.P. Moller – Maersk A/S, all of which have made substantial investments in automotive-dedicated divisions with specialized equipment pools, port handling capabilities, and technology platforms tailored to OEM requirements. The transportation segment's share is expected to remain dominant throughout the forecast period, consolidating as providers achieve scale efficiencies and expand multi-modal service offerings that reduce handoff friction between modes.

The ongoing transition to electric vehicles is introducing incremental complexity into the transportation segment, as battery packs classified as dangerous goods under international regulations require segregated handling, enhanced packaging standards, and trained personnel — all of which add cost but also create premium-priced service opportunities for providers investing in compliance capabilities.