Belt Starter Generator Dominance in the Automotive 48V System Market

Among the four primary architectural configurations in the Automotive 48V System Market — Belt Driven, Crankshaft Mounted, Dual-Clutch Transmission-Mounted, and Transmission Output Shaft — the Belt Driven segment, primarily implemented as a Belt Starter Generator (BSG) or Belt-integrated Starter Generator (BiSG), commands the dominant revenue share. This dominance is attributable to the BSG architecture's superior balance of performance improvement, packaging simplicity, and retrofit compatibility with existing engine platforms.

The BSG system replaces the conventional alternator with a combined motor-generator unit connected to the crankshaft via a serpentine belt. This design enables regenerative braking, engine-off coasting, boost assistance during acceleration, and seamless engine restarts — all of which contribute to measurable fuel economy gains. Critically, BSG integration does not require fundamental engine redesign, making it the preferred pathway for OEMs seeking rapid compliance with emissions standards across high-volume production lines.

From a revenue perspective, the Belt Driven segment accounts for an estimated 45–50% of total Automotive 48V System Market revenues in the current period. This share is expected to remain robust through 2028, after which Dual-Clutch Transmission-Mounted and Crankshaft Mounted architectures are projected to gain incremental share as OEMs shift toward more deeply integrated P0/P1 hybrid topologies in premium and performance segments.

Key players within the Belt Driven sub-segment include Robert Bosch GmbH, which has supplied BSG systems to multiple European OEM platforms including the Mercedes-Benz C-Class and Audi A6 mild hybrid variants; Valeo, whose i-StARS system represents one of the most widely deployed 48V BSG solutions globally; and Continental AG, which integrates BSG technology within its broader electrification portfolio targeting both European and Asian platforms.

BorgWarner Inc has also made meaningful inroads in BSG manufacturing through its Morse Systems division and subsequent electrification-focused acquisitions, while Magna International Inc offers modular BSG solutions adaptable across multiple powertrain configurations. MAHLE Powertrain Ltd contributes belt-integrated thermal management technologies that complement BSG efficiency by optimizing engine warm-up profiles.

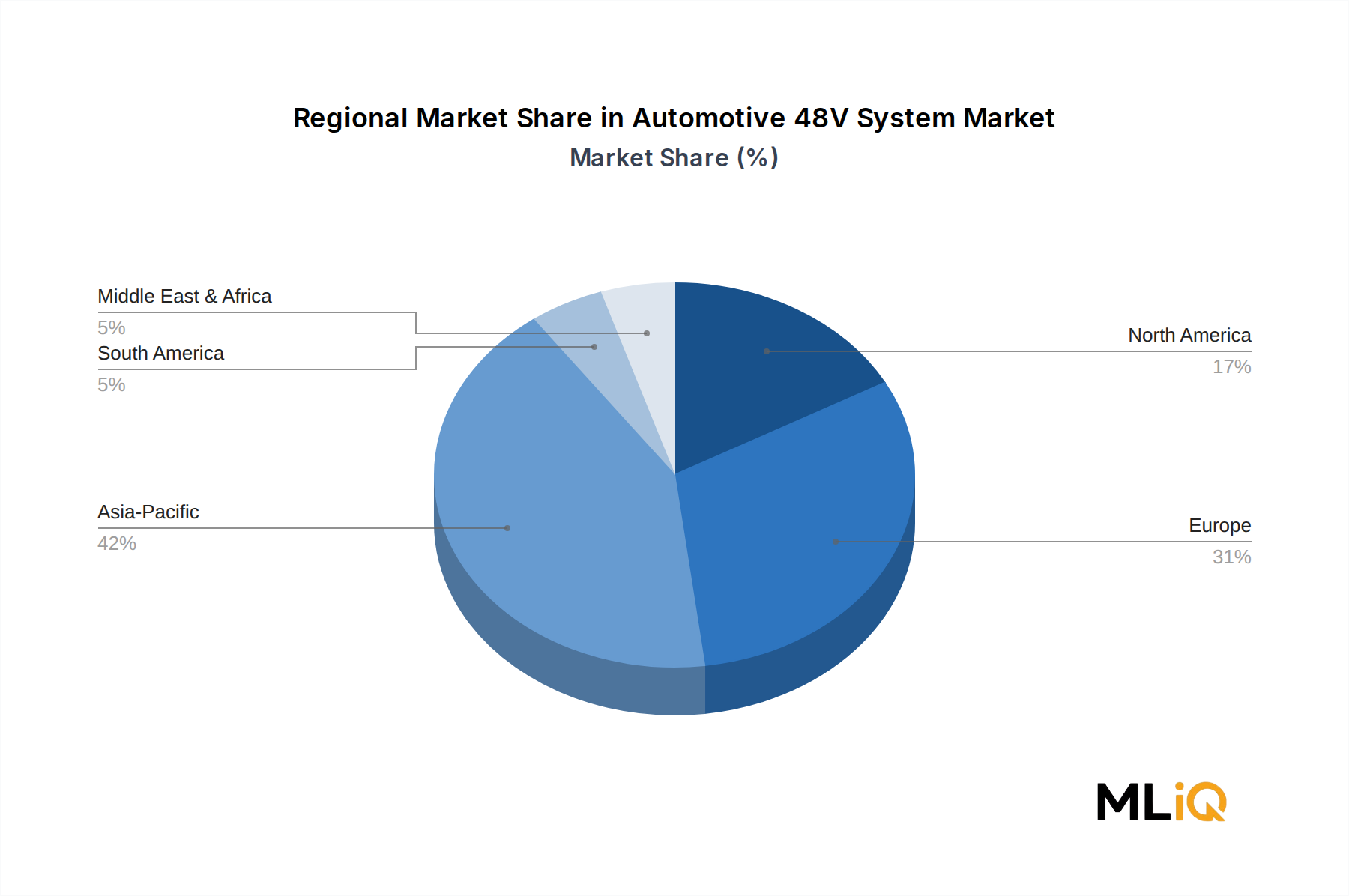

The geographic concentration of Belt Driven segment revenue is highest in Europe, where regulatory pressure is most acute, and in China, where domestic OEMs such as SAIC, Geely, and BYD (for their non-BEV product lines) are adopting BSG-based 48V mild hybrids as a transitional solution ahead of full electrification. In North America, Ford, General Motors, and Stellantis have initiated BSG programs primarily targeting truck and SUV platforms where fuel economy penalties from conventional powertrains are most significant.

The consolidating nature of the Belt Driven segment is evident from the concentration of supplier contracts among fewer than eight globally capable tier-1 manufacturers. Barriers to entry are rising as OEM qualification cycles lengthen, system integration complexity deepens, and capital requirements for 48V-specific electromagnetic and power electronics design escalate. These dynamics favor incumbent suppliers with established manufacturing footprints and validated system-level integration capabilities.

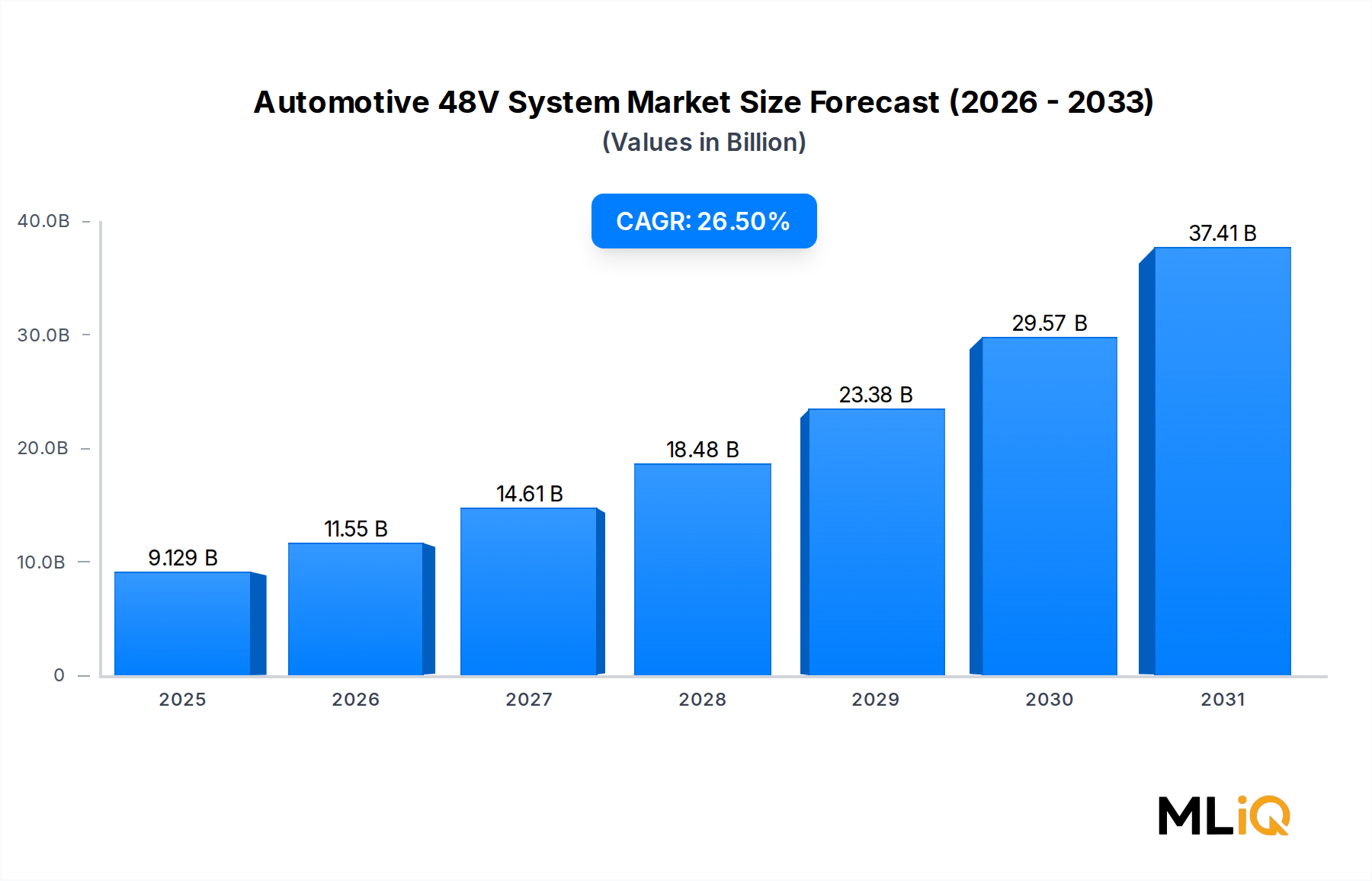

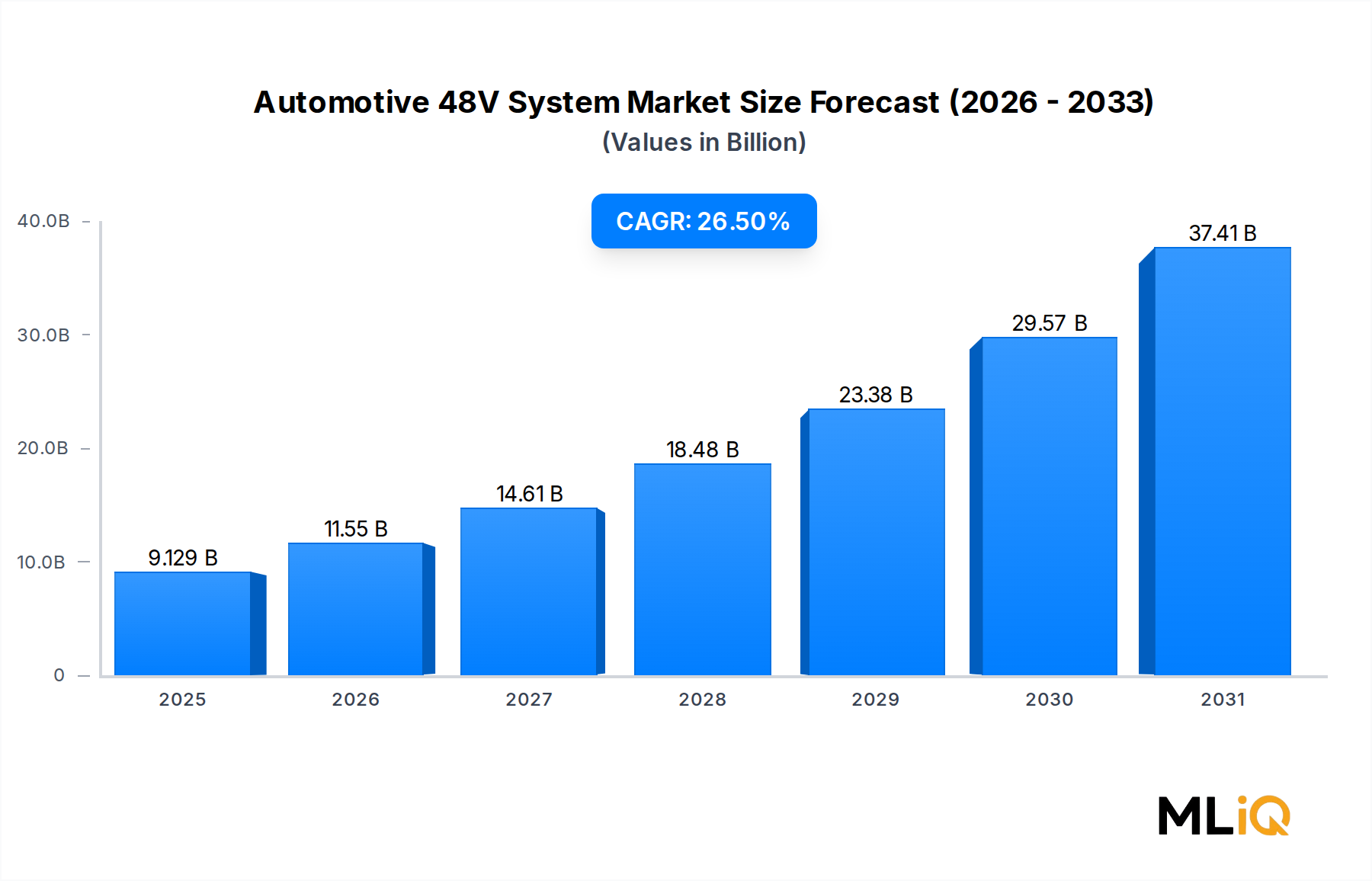

Looking ahead, the Belt Driven segment's dominance will be reinforced by its applicability across all vehicle classes — from Entry to Luxury — ensuring broad addressable volume even as competing architectures gain traction in niche performance and premium applications. The segment's CAGR is estimated at 24–26% through the forecast period, closely tracking the overall market growth trajectory.