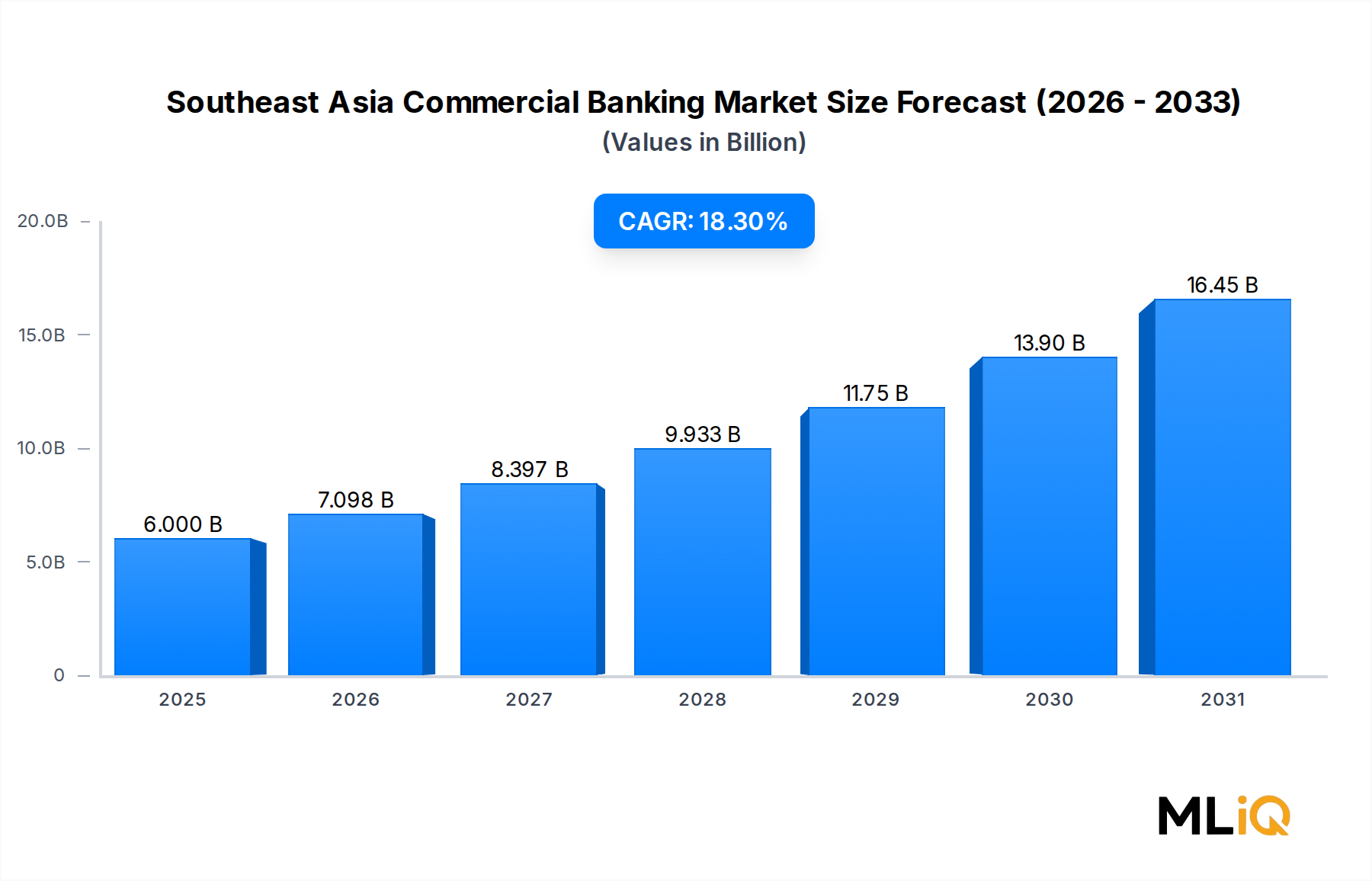

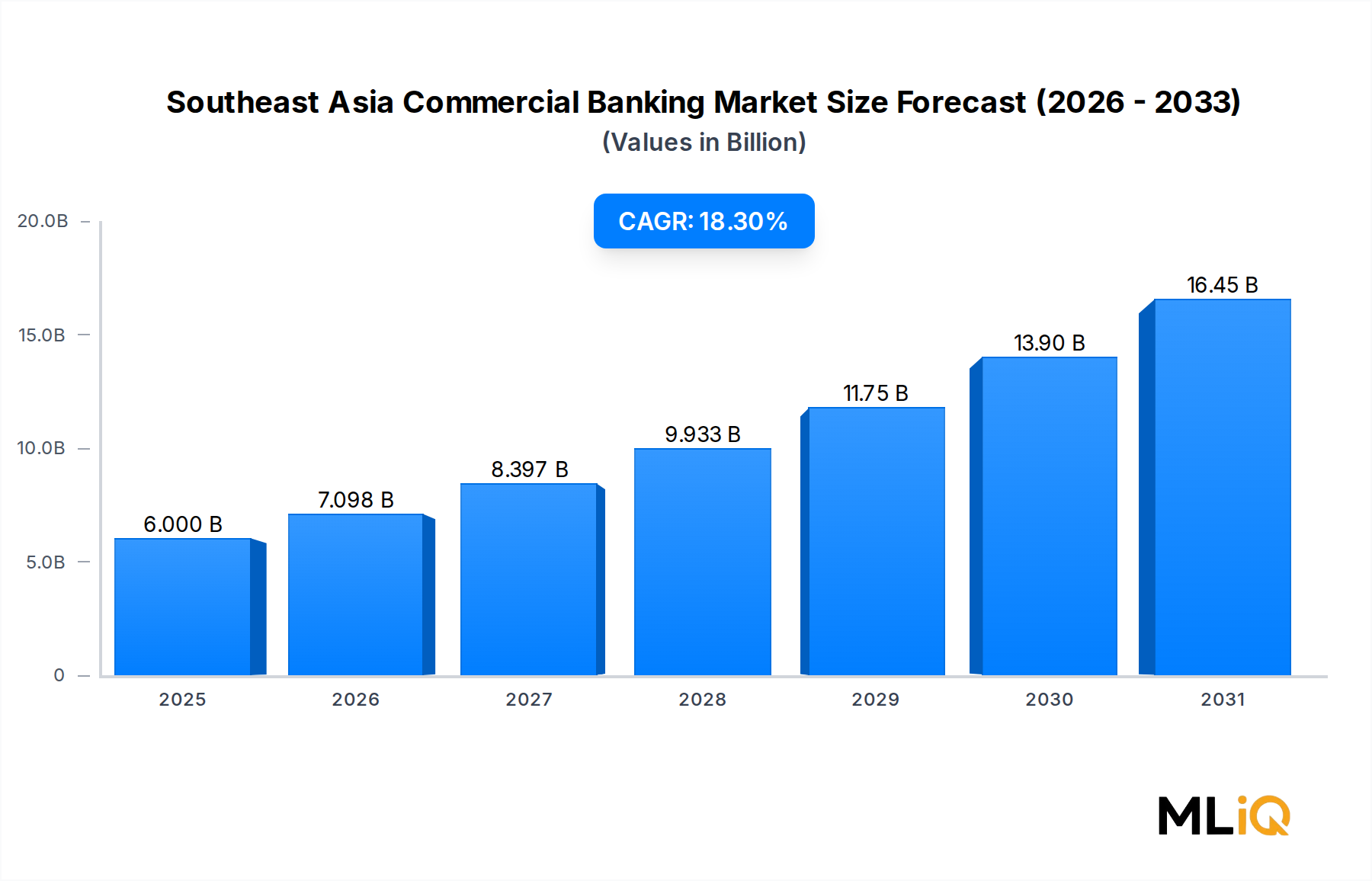

Commercial Lending Dominance in the Southeast Asia Commercial Banking Market

Commercial lending stands as the single largest and most strategically significant segment within the Southeast Asia Commercial Banking Market, contributing the dominant share of total revenues across the forecast period. Its primacy is driven by the region's insatiable demand for credit across corporate, mid-market, and infrastructure-linked borrower profiles, supported by favorable demographic trends, expanding manufacturing bases, and deepening integration into global supply chains.

At its core, commercial lending in Southeast Asia encompasses working capital facilities, term loans, revolving credit lines, and structured credit products tailored for large corporates, state-owned enterprises, and increasingly, mid-market businesses. The segment's dominance is not merely a function of volume but also of margin quality. Commercial loans in emerging ASEAN markets typically carry wider spreads than those in developed markets, reflecting both the risk premium and the structural underpenetration of formal credit.

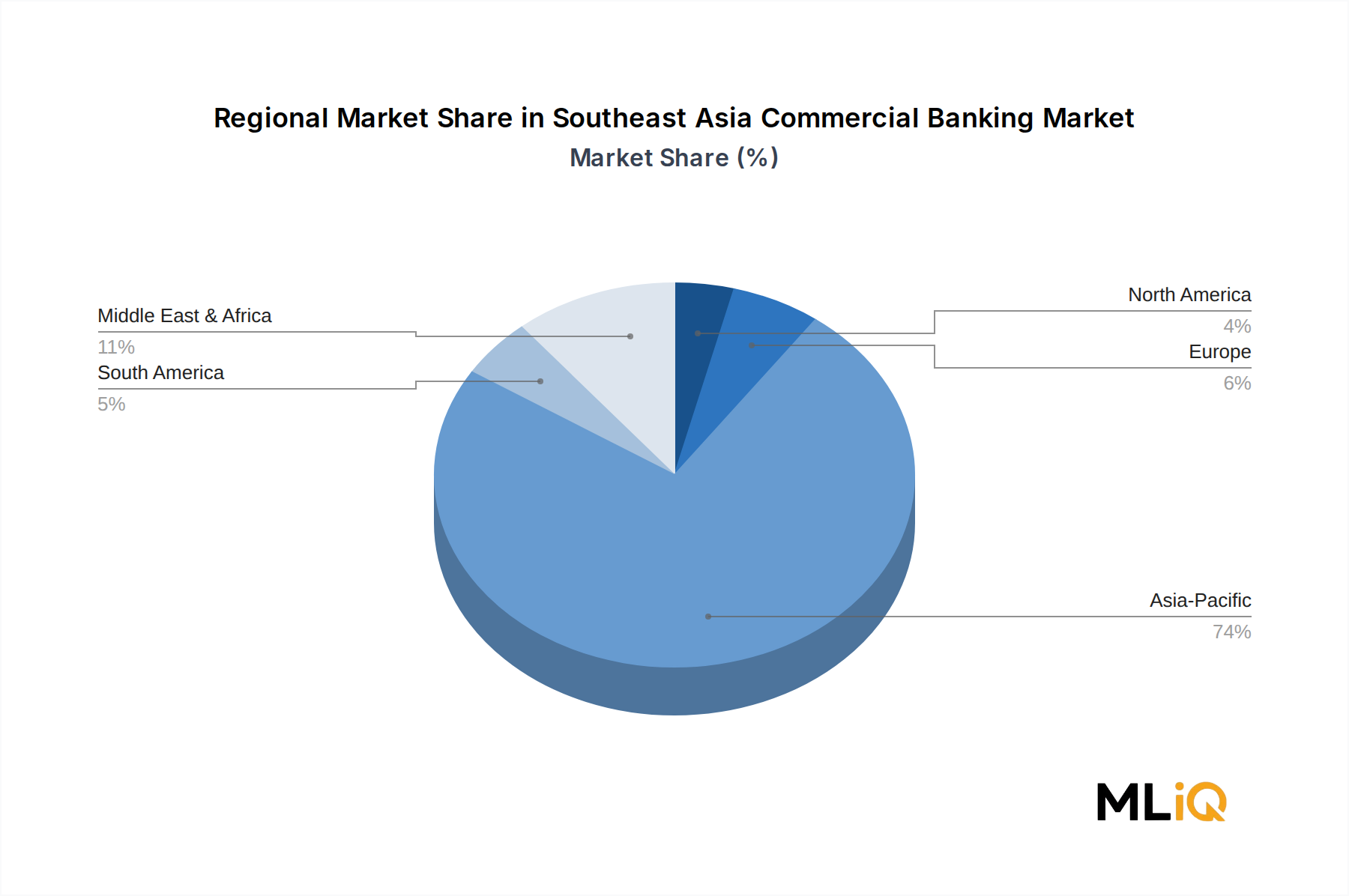

Indonesia, the region's largest economy, has been a primary engine of commercial lending growth. Infrastructure development programs under successive government administrations have generated enormous demand for project-linked credit, benefiting institutions such as PT Bank Mandiri (Persero) Tbk. and PT Bank Rakyat Indonesia (Persero) Tbk., both of which have aggressively expanded their corporate lending books. In Malaysia, Malayan Banking Berhad and CIMB GROUP HOLDINGS BERHAD have leveraged their regional networks to originate cross-border commercial loans, particularly in the infrastructure, energy, and real estate sectors.

Singapore continues to serve as the regional headquarters for multinational commercial lending operations. DBS Bank Ltd has emerged as a leading arranger of syndicated loans across ASEAN, while OCBC Bank and United Overseas Bank Limited have deepened their corporate banking franchises through targeted sector strategies in technology, real estate, and commodities. The presence of global banks such as HSBC Group and Citigroup, Inc. further intensifies competition, particularly for large-cap mandates and cross-border financing structures.

Several structural factors are reinforcing the commercial lending segment's dominance. First, the ASEAN region's trade-to-GDP ratios remain among the highest globally, generating persistent demand for trade-linked lending instruments. Second, the regionalization of supply chains post-pandemic has accelerated investment in manufacturing capacity across Vietnam, Thailand, and Indonesia, directly fueling term lending demand. Third, governments across the region have introduced credit guarantee schemes and development finance instruments that de-risk commercial bank lending, particularly to priority sectors such as renewable energy, healthcare, and digital infrastructure.

The segment is also undergoing a qualitative transformation. Banks are moving beyond plain-vanilla lending to offer structured solutions that blend commercial credit with hedging, cash management, and advisory services. This bundling strategy not only deepens client relationships but also supports fee income diversification, a critical priority as interest rate cycles introduce margin volatility.

Consolidation dynamics within the commercial lending segment are worth noting. Larger regional banks are progressively capturing market share from smaller domestic institutions, driven by superior technology platforms, broader product suites, and stronger capital bases. This concentration trend is expected to intensify over the forecast period as regulatory capital requirements and digital investment costs create meaningful barriers to scale. The Asia Pacific Retail Banking Market intersects with commercial banking here, as dual-purpose banking groups cross-sell corporate and retail products to owner-managed enterprises, blurring traditional segmentation lines.