Long-Term Loans as the Dominant Segment in the Term Loan Market

Within the Term Loan Market, long-term loans — defined as credit facilities with repayment tenors exceeding five years and extending in many cases to twenty-five or thirty years — represent the single largest segment by revenue share. This dominance stems from the structural characteristics of long-term loans that align perfectly with the needs of capital-intensive borrowers in sectors such as infrastructure, commercial real estate, energy transition, and heavy manufacturing.

The primacy of long-term loans is fundamentally rooted in asset-liability matching. Large-scale borrowers require financing that matches the productive life of the underlying asset. A toll road with a thirty-year concession period, for instance, demands a debt instrument of commensurate duration. This logic extends across utilities, telecommunications networks, offshore energy platforms, and hospital construction, all of which rely on long-duration term debt to maintain manageable debt service coverage ratios during early operational phases.

From a lender perspective, long-term loans generate sustained interest income streams that are valuable for institutions managing liability-driven investment portfolios, particularly insurance companies and pension funds. This creates a natural investor base that actively seeks to deploy capital into long-tenor credit instruments, reinforcing supply-demand equilibrium in this segment.

Key players operating prominently in the long-term loan segment include established universal banks with deep balance sheet capacity, development finance institutions such as the World Bank Group and regional multilateral lenders, and infrastructure-focused private credit funds. Among the companies tracked in this report, Tata Capital Limited has built a substantial long-term corporate lending portfolio in South and Southeast Asia, while Funding Circle Limited has explored longer loan tenors for small business clients, particularly those in the commercial real estate and professional services verticals.

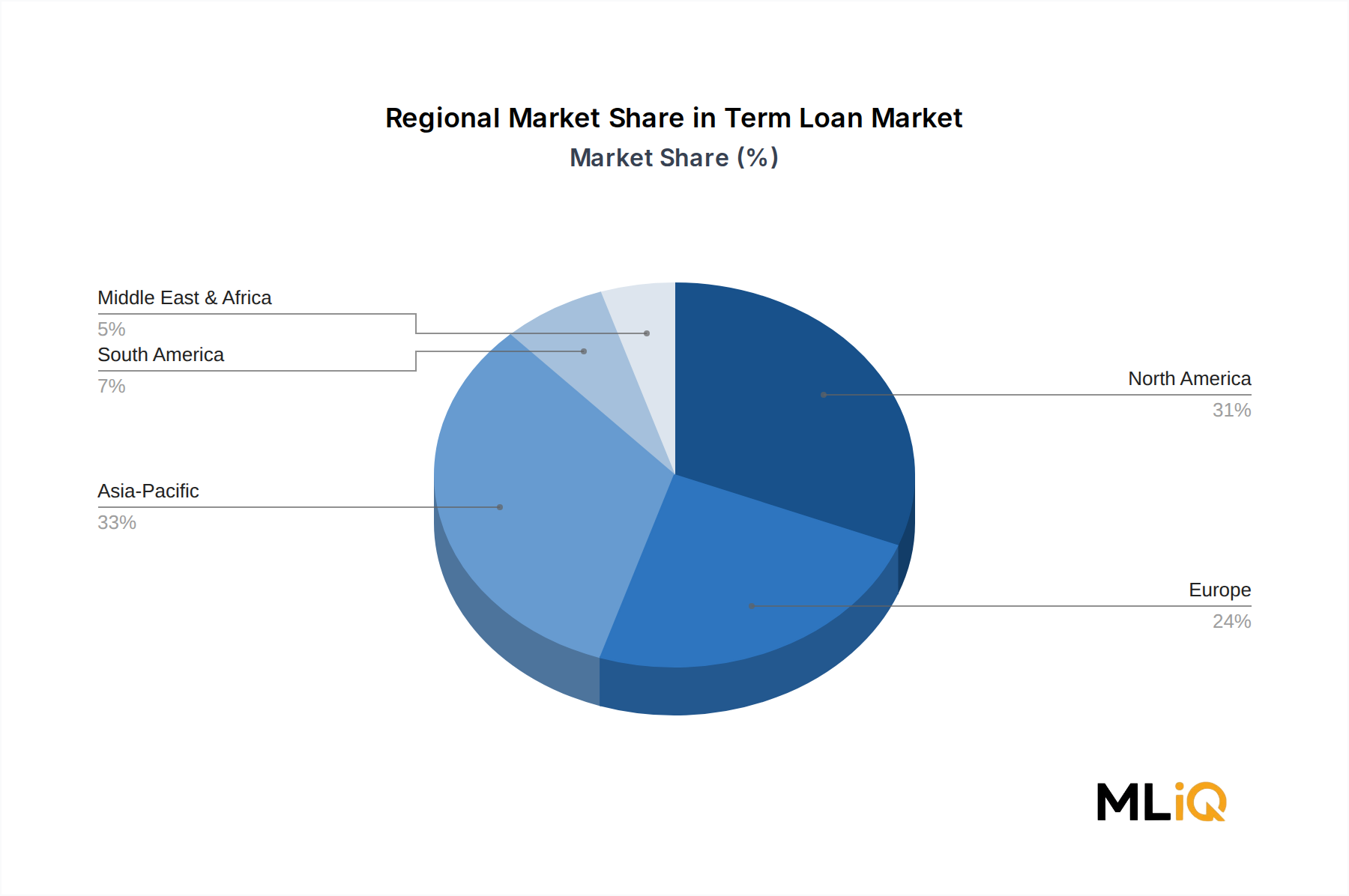

Geographically, North America and Europe account for the largest absolute volumes in long-term lending, driven by mature real estate markets, sophisticated project finance ecosystems, and deep institutional investor bases. However, Asia Pacific — particularly China and India — is rapidly closing the gap as domestic infrastructure pipelines accelerate and local capital markets deepen.

The segment's share is currently consolidating rather than growing rapidly in percentage terms, as intermediate-term loans take a larger slice of incremental demand. This reflects the structural shift toward shorter investment cycles in technology-intensive industries, where asset obsolescence occurs faster and borrowers prefer flexibility over duration certainty. Nevertheless, long-term loans remain unchallenged as the highest-volume category in absolute dollar terms, and their relevance will persist as long as global infrastructure investment remains a political and economic priority.

Finally, regulatory trends such as Basel IV capital adequacy requirements are influencing how banks structure and distribute long-term loan exposures. Syndication, securitization, and loan sales to insurance and pension investors are increasingly common mechanisms by which originating banks manage long-term credit concentrations, effectively creating a secondary market ecosystem around this dominant segment.