Digital Channel Dominance Reshaping the Singapore Remittance Market

Among all segments analyzed within the Singapore Remittance Market, the digital channel — encompassing mobile applications, online platforms, and API-driven money transfer operator (MTO) networks — has emerged as the unambiguously dominant segment by both transaction value and volume growth trajectory. This segment's supremacy is rooted in a confluence of structural, behavioral, and regulatory factors that have permanently altered how remittances are executed in Singapore.

Historically, banks dominated the Singapore remittance landscape due to their established trust, branch networks, and integration with SWIFT infrastructure. However, the enactment of the Payment Services Act in 2019, which created a unified licensing regime for payment service providers, catalyzed entry from fintech operators offering dramatically lower fees, faster settlement times, and superior user experience. Banks, while retaining a significant share of high-value corporate and SME transfers, have progressively ceded the high-frequency, low-value consumer segment to digital MTOs.

The digital channel's dominance is reflected in adoption metrics: smartphone penetration among Singapore's migrant worker population has crossed 78%, with platforms such as Wise, WorldRemit, and Instarem reporting year-on-year user growth exceeding 20% in Singapore-originating corridors. Nium Pte. Ltd. (Instarem) has been particularly aggressive, leveraging its regional payment infrastructure to offer real-time transfers to over 60 countries with transparent, mid-market exchange rates.

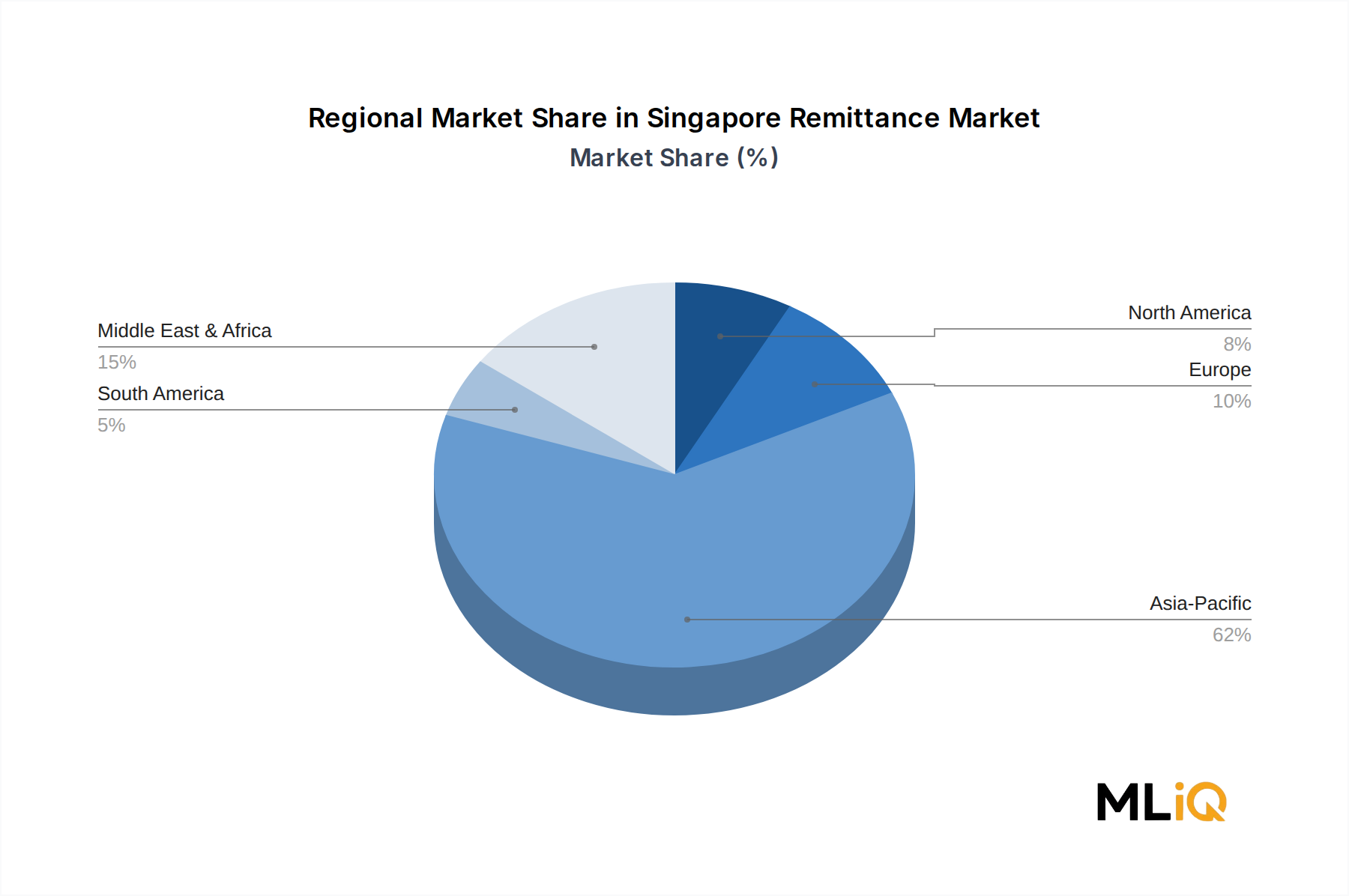

Within the digital segment, the Consumer-to-Consumer (C2C) mode remains the largest sub-segment by transaction count, driven by migrant workers remitting wages to families in South and Southeast Asia. The Philippines-Singapore corridor alone processes an estimated USD 1.2 billion annually, while the India-Singapore corridor exceeds USD 2.5 billion, making these two corridors the market's highest-volume arteries.

The Business-to-Business (B2B) mode, while smaller by transaction count, generates disproportionately large transaction values and is the fastest-growing digital sub-segment. Singapore's role as a regional treasury and procurement hub for multinationals and SMEs drives B2B cross-border flows, with platforms like Nium and Wise for Business capturing treasury teams seeking alternatives to expensive bank wire transfers.

Key players driving digital channel growth include Wise Payments Limited, which has established direct bank integrations and a local SGD account offering; Revolut Ltd, which bundles remittance within a broader multi-currency banking proposition; and WorldRemit, which has focused on mobile money delivery to Southeast Asian and South Asian corridors. DBS Bank Ltd has responded by launching Paylah! international transfer capabilities and integrating with PayNow's cross-border links, attempting to retain digitally native customers.

The digital channel's share is consolidating rather than simply growing — traditional cash-agent networks operated by Western Union and MoneyGram still serve a residual niche among workers without smartphones or bank accounts, but this niche is contracting at approximately 4–6% annually as financial inclusion programs, employer-facilitated digital wallets, and MAS-mandated dormitory Wi-Fi access expand digital reachability.

The segment's continued dominance is secured by the MAS sandbox environment, which encourages innovation, and by bilateral fast-payment linkages that reduce settlement risk and cost for digital operators, creating a structurally favorable environment for sustained market share expansion through the forecast period.