Equities Segment Dominance in the Securities Lending Market

Among the four primary asset type segments — Equities, Government Bonds, Corporate Bonds, and Others — equities consistently command the largest revenue share in the Securities Lending Market. This dominance is structural, rooted in the mechanics of short selling, event-driven arbitrage strategies, and the sheer volume of equity securities outstanding across global exchanges.

Equity lending generates the highest per-transaction fee income compared to sovereign or investment-grade fixed income lending. This is because equity securities, particularly those that are in high demand for short positions (classified as "specials" in lending parlance), command significantly elevated lending fees — sometimes exceeding 500 basis points annualized for the most sought-after names. Government bonds, by contrast, typically trade as "general collateral" at lending fees of 5 to 20 basis points, reflecting their abundance and lower specificity of demand.

The dominance of equities is further reinforced by the behavior of hedge funds, the largest borrower segment. Quantitative hedge funds, long/short equity funds, and merger arbitrage funds all depend heavily on equity borrow availability to execute their strategies. As hedge fund assets under management globally have grown — reaching an estimated $4.5 trillion in recent years — so too has the demand for equity lending capacity.

On the supply side, the lendable pool of equities is anchored by large institutional holders: pension funds, sovereign wealth funds, insurance companies, and mutual fund complexes. Organizations such as State Street Corporation, The Bank of New York Mellon Corporation, and JPMorgan Chase & Co operate massive custodial and agency lending programs, channeling their clients' equity holdings into lending programs that generate basis-point returns on otherwise idle assets.

The equities segment is also benefiting from the proliferation of exchange-traded funds (ETFs). ETF providers, including Invesco Ltd and others, have embedded securities lending programs within their fund structures, using lending revenue to offset management fees and improve total returns for end investors. This has made ETF-based equity lending one of the fastest-growing sub-segments within the broader equities category.

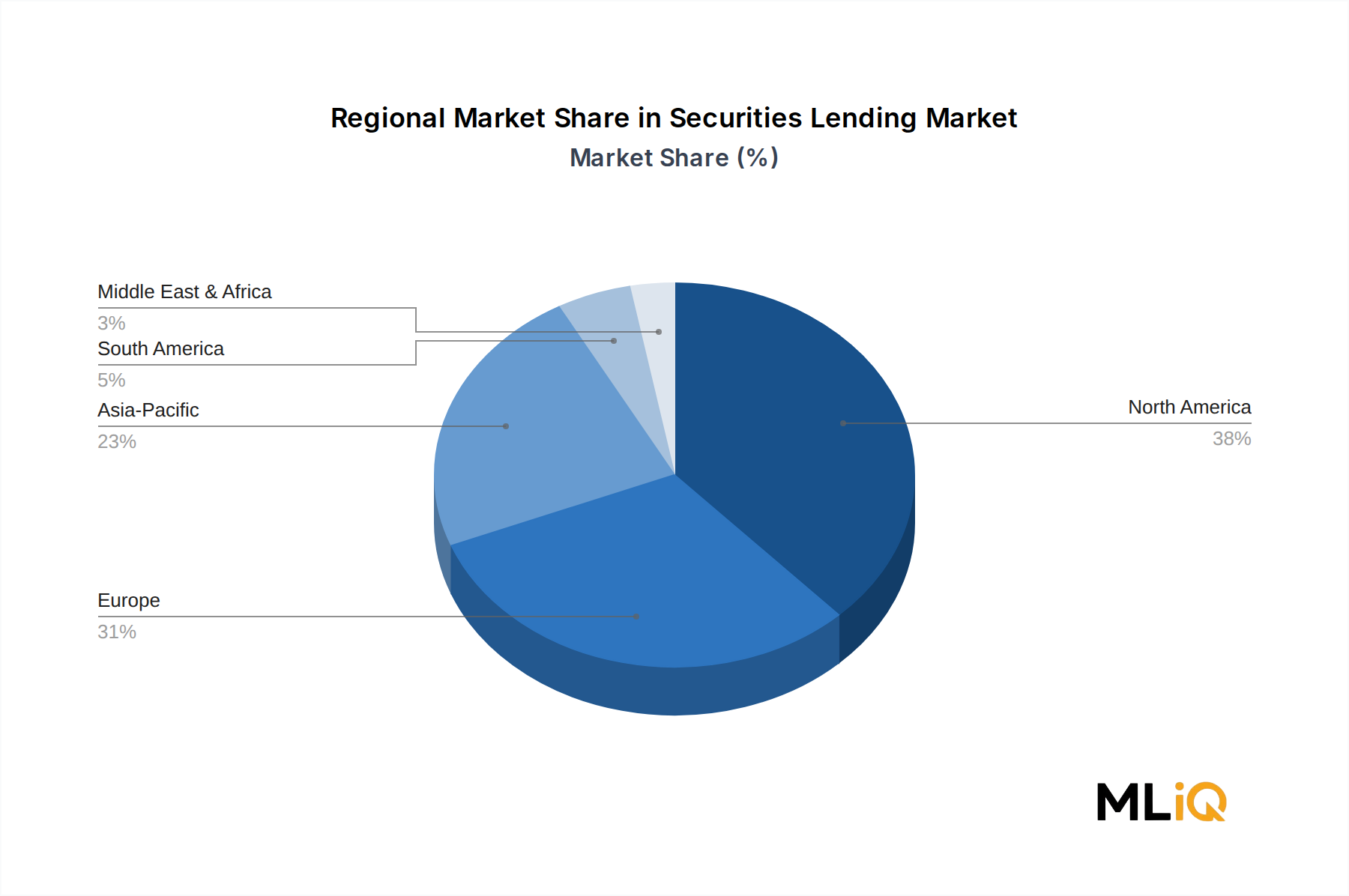

In terms of geographic concentration, equities lending is most active in North America and Europe, where equity markets are deepest and most liquid. The United States alone accounts for a disproportionate share of global equity lending volume, given the scale of its listed equity market capitalization and the density of its hedge fund ecosystem.

However, the equities segment is not without competitive pressure. The rise of synthetic exposure instruments — notably total return swaps and contracts for difference — offers borrowers an alternative to physical equity borrowing, compressing volumes at the margin. Regulatory requirements around stock loan disclosure and beneficial ownership reporting are also increasing compliance overhead for equity lending desks.

Nevertheless, the equities segment's share within the Securities Lending Market is expected to remain dominant through the forecast period. Structural demand from short sellers, arbitrageurs, and ETF mechanics, combined with the expanding universe of lendable equity assets driven by growing institutional AUM, ensures that equities will continue to anchor revenues across the market's value chain. Key players are investing in technology platforms to improve the speed and efficiency of equity borrow sourcing, with automated negotiation tools and real-time inventory management systems becoming standard infrastructure requirements for major lending desks.