Commercial Banks as the Dominant Segment in the Retail Banking Market

Within the Retail Banking Market, commercial banks represent the dominant segment by revenue share, accounting for the largest proportion of total market value across all measured geographies. This dominance is rooted in the institutional scale, regulatory licensing advantages, diversified product portfolios, and established customer trust that commercial banks have cultivated over decades. Their position is not merely historical inertia—it reflects active competitive reinforcement through technology investment, branch network rationalization, and strategic product bundling.

Commercial banks derive their strength from their ability to serve both individual consumers and small-to-medium enterprises simultaneously, creating cross-sell efficiencies that rural banks and non-bank financial intermediaries cannot replicate at scale. A typical commercial bank offering spans bank account opening, debit and credit card issuance, deposit management, personal and business loans, mortgage products, foreign exchange services, and increasingly, investment and insurance products distributed through bancassurance channels.

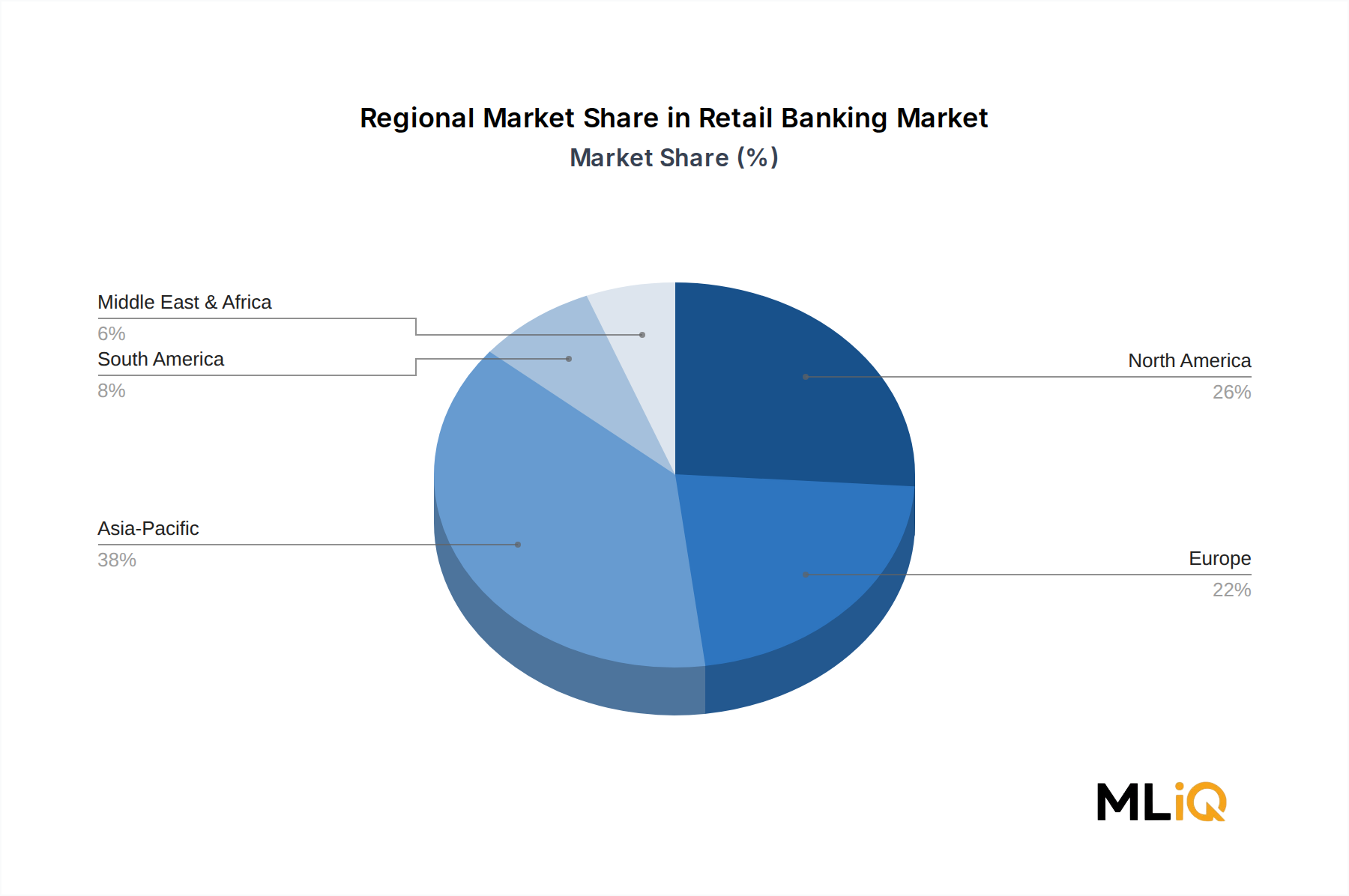

The segment's dominance is particularly pronounced in North America and Western Europe, where institutions such as JP Morgan Chase & Co., Wells Fargo & Company, BNP Paribas, and Barclays Bank Plc command multi-trillion-dollar asset bases and serve tens of millions of retail customers. In Asia Pacific, the Industrial and Commercial Bank of China (Asia) Limited and Mitsubishi UFJ Financial Group represent anchor institutions whose retail banking operations alone rival the total GDP of mid-sized economies.

A key structural advantage for commercial banks is their access to low-cost deposit funding through demand deposit accounts, which provides a significant funding cost advantage over non-bank lenders and fintech challengers. This net interest margin advantage, even as it has compressed in certain jurisdictions due to near-zero or negative policy rates, remains a core profitability driver. As central banks in the United States, Europe, and parts of Asia Pacific have moved into rate normalization cycles post-2022, commercial banks have benefited from margin expansion that has partially offset increased credit provisioning requirements.

The Wealth Management Market is increasingly becoming a strategic battleground within the commercial banking segment. Major commercial banks are expanding their private banking and investment advisory arms to capture high-net-worth and mass-affluent customer segments, recognizing that fee-based income from wealth management provides more stable revenue streams than cyclical interest income. Institutions like Goldman Sachs Group and Citigroup have restructured their retail and wealth units to better integrate these services under a unified client experience model.

Digitalization is reshaping the competitive dynamics within the commercial banking segment. The adoption of cloud-native core banking systems sourced from the Banking Software Market is enabling commercial banks to launch new products in weeks rather than months, a capability previously exclusive to fintech startups. Mobile-first account opening, AI-powered credit scoring, and real-time fraud detection are now table-stakes capabilities for any commercial bank seeking to retain millennial and Gen Z customer cohorts.

While rural banks and other financial institutions serve important geographic and demographic niches—particularly in frontier markets and agricultural communities—they lack the capital adequacy, product breadth, and technology investment capacity to challenge commercial banks for segment leadership in the near term. The commercial banking segment's share is therefore expected to consolidate further through 2033, driven by ongoing M&A activity, digital scale advantages, and regulatory capital requirements that favor well-capitalized incumbents.