Consumer Credit Loans: The Dominant Segment in the Peer to Peer Lending Market

Within the Peer to Peer Lending Market, Consumer Credit Loans represent the single largest revenue-generating segment by loan type, commanding a dominant share of total origination volumes globally. This segment's primacy is attributable to a combination of structural demand factors, accessible digital interfaces, and the relative simplicity of underwriting personal credit compared to more complex commercial or real estate loan products.

Consumer credit loans channeled through P2P platforms typically serve borrowers seeking debt consolidation, medical expense financing, home improvement funding, and general-purpose liquidity. The average loan size in this segment ranges from $5,000 to $40,000 depending on the platform and geographic market, with loan tenors commonly spanning 12 to 60 months. These characteristics make consumer credit a natural fit for P2P mechanics — the ticket sizes are large enough to be meaningful for lenders seeking yield, yet small enough to enable risk diversification across large pools.

The dominance of this segment is further reinforced by platform user experience design. Leading platforms such as LendingClub Bank and Prosper Funding LLC have architected their onboarding workflows specifically around consumer borrower profiles, deploying proprietary credit scoring algorithms that incorporate non-traditional data signals. This has allowed approval rates on the Consumer Credit Loans segment to surpass those achievable through conventional bank underwriting for comparable risk cohorts.

From a lender perspective, consumer credit loans offer predictable amortization schedules and relatively short duration risk, making them attractive to both retail and institutional participants on the funding side. The secondary market liquidity for consumer P2P loan instruments has improved significantly over the past five years, with platforms introducing note trading facilities that allow lenders to exit positions before maturity — a feature that has meaningfully expanded the investor base for this segment.

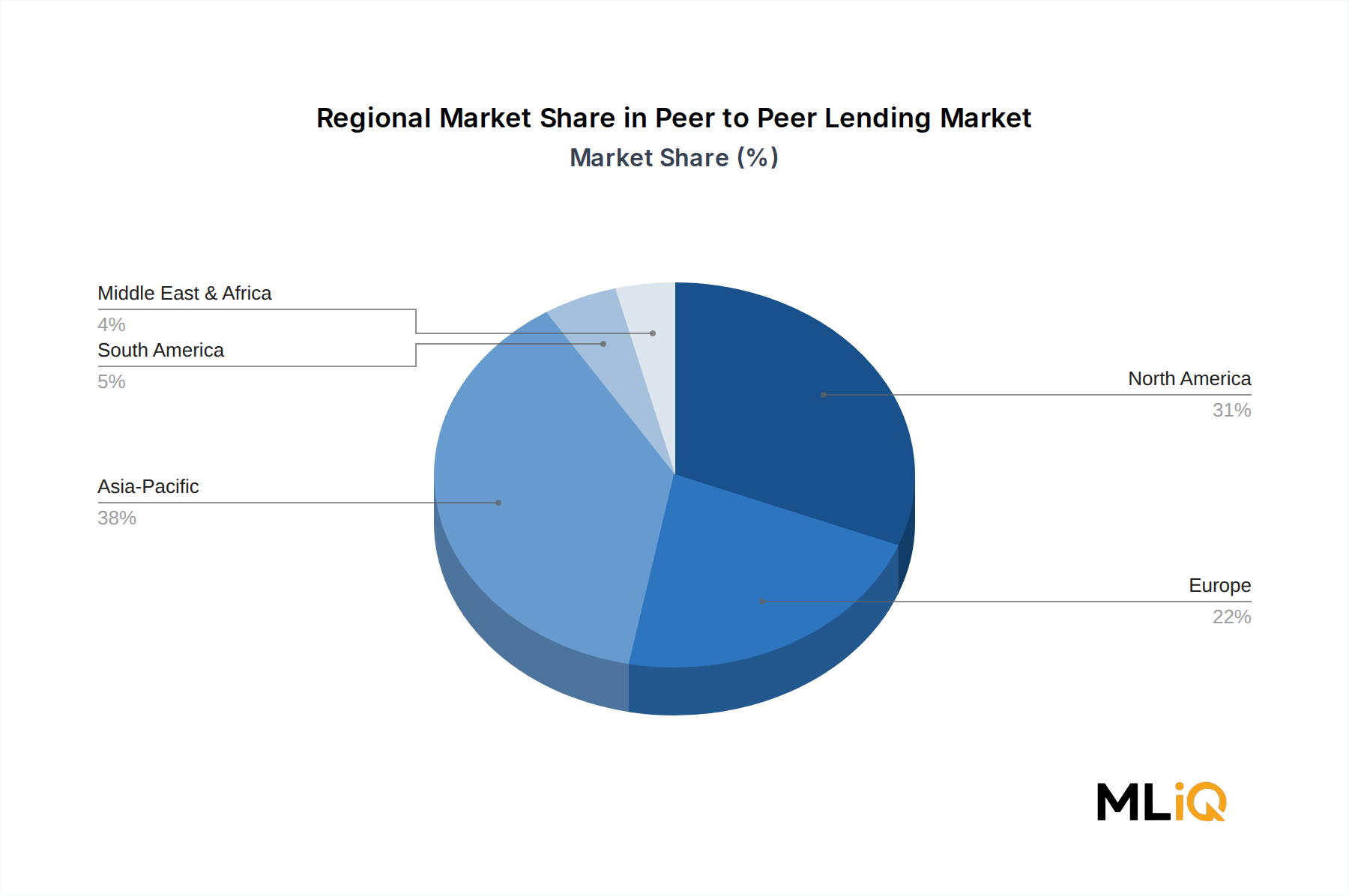

Geographically, North America leads consumer credit P2P originations, followed closely by the United Kingdom and Australia. In the U.S., the transition of LendingClub to a bank charter model marked a pivotal structural shift, with the platform now able to hold loans on balance sheet while simultaneously facilitating P2P-style marketplace lending. This hybrid model is increasingly being replicated by competitors seeking regulatory durability and capital efficiency.

The competitive intensity within the consumer credit segment is high. Upstart Network has emerged as a formidable challenger by deploying AI-driven underwriting that reportedly evaluates over 1,600 variables per application, resulting in materially lower default rates compared to FICO-only models. LendingTree operates as a marketplace aggregator within this segment, channeling borrower intent signals to multiple competing lenders and extracting monetization through lead generation economics.

The segment's share is growing rather than consolidating. New entrants — particularly those targeting specific borrower demographics such as Gen Z thin-file borrowers, gig economy workers, and immigrant communities — are expanding the total addressable market rather than merely redistributing existing origination volumes. This dynamic suggests that Consumer Credit Loans will continue to account for the plurality of Peer to Peer Lending Market revenue through at least 2028, even as business and real estate loan segments accelerate on a relative basis.

Platform differentiation within this segment is increasingly shifting from interest rate competition to experience, speed, and trust-signal differentiation. Same-day funding capabilities, embedded credit monitoring dashboards, and responsible lending disclosures have become table-stakes features rather than competitive differentiators, compelling platforms to invest in next-generation personalization and borrower retention capabilities.