Indirect Sales Channel Dominance in the Marine Cargo Insurance Market

Among the distribution channels segmenting the Marine Cargo Insurance Market, indirect sales channels constitute the dominant revenue-generating pathway, accounting for the largest share of gross written premiums globally. This dominance is rooted in the structural complexity of marine cargo risk, which necessitates intermediary expertise to navigate policy design, claims management, and regulatory compliance across multi-jurisdictional trade routes.

Indirect sales channels encompass a broad ecosystem of brokers, agents, freight forwarders acting as insurance intermediaries, and bancassurance networks embedded within trade finance platforms. Insurance brokers — particularly global firms with specialized marine practices — command significant influence over premium placement decisions, leveraging their market access across Lloyd's syndicates, P&I clubs, and conventional carriers to optimize coverage terms for large commercial clients. The broker-mediated segment is especially prominent among cargo owners managing high-value or complex supply chains, where bespoke coverage structures require underwriter negotiation that direct channels cannot efficiently replicate.

Freight forwarders represent an increasingly consequential subcategory within indirect distribution, as their dual role in logistics coordination and cargo insurance facilitation positions them as embedded risk advisors. Many freight forwarders have formalized agency agreements with insurers, allowing them to offer contingency coverage and shipper's interest policies directly through their operational platforms. This convergence of logistics and insurance services reflects a broader trend toward bundled value propositions that reduce administrative friction for cargo owners.

Digital intermediary platforms — insurtechs operating as licensed brokers — are expanding the indirect channel's reach into the SME and mid-market segments. These platforms use API-driven integrations with shipping data providers, customs authorities, and freight management systems to generate real-time coverage recommendations, automate certificate issuance, and facilitate digital claims filing. The operational efficiency unlocked by these platforms is compressing the cost-to-serve for indirect distribution, making it viable at transaction value thresholds previously considered uneconomical for broker involvement.

The indirect channel's dominance is unlikely to erode significantly through 2033, primarily because the complexity of international trade risk — encompassing multi-modal transit, containerized and break-bulk cargo, open cover policies, and accumulation risk management — demands advisory intermediation that automated direct channels cannot yet replicate at scale. Large corporates with dedicated risk management departments and logistics operations spanning multiple geographies consistently prefer broker-led placements for their ability to aggregate capacity across multiple underwriters and negotiate manuscript policy language.

Key players leveraging indirect distribution architectures include MARSH LLC., which commands one of the largest global marine brokerage practices, and Lloyd's, whose syndicate structure is inherently broker-dependent. Allianz and Chubb have also invested in broker relationship management programs to secure preferred placement status within top-tier intermediary networks. The consolidation of brokerage assets — through mergers and acquisitions among mid-tier regional brokers — is concentrating placement volumes within fewer, larger intermediary firms, which reinforces the structural weight of the indirect channel within total market revenue.

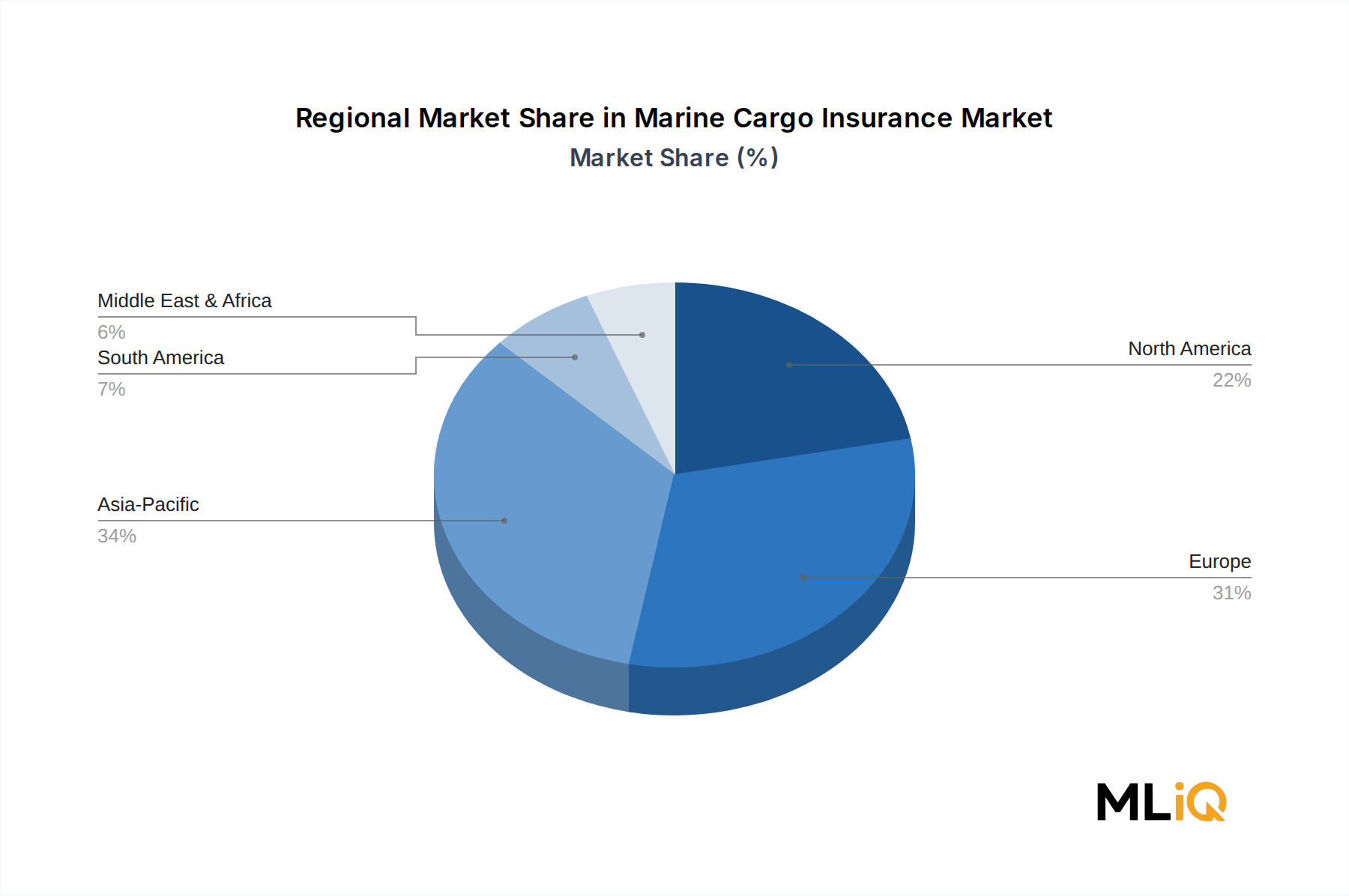

The indirect sales trajectory is also being shaped by bancassurance expansion, particularly in emerging markets where trade finance banks are bundling cargo insurance into their letter of credit and documentary collection services. This embedded distribution model is proving particularly effective in Asia Pacific and the Middle East, where SME exporters rely heavily on bank-facilitated trade finance and benefit from the simplified underwriting embedded within bank product suites.