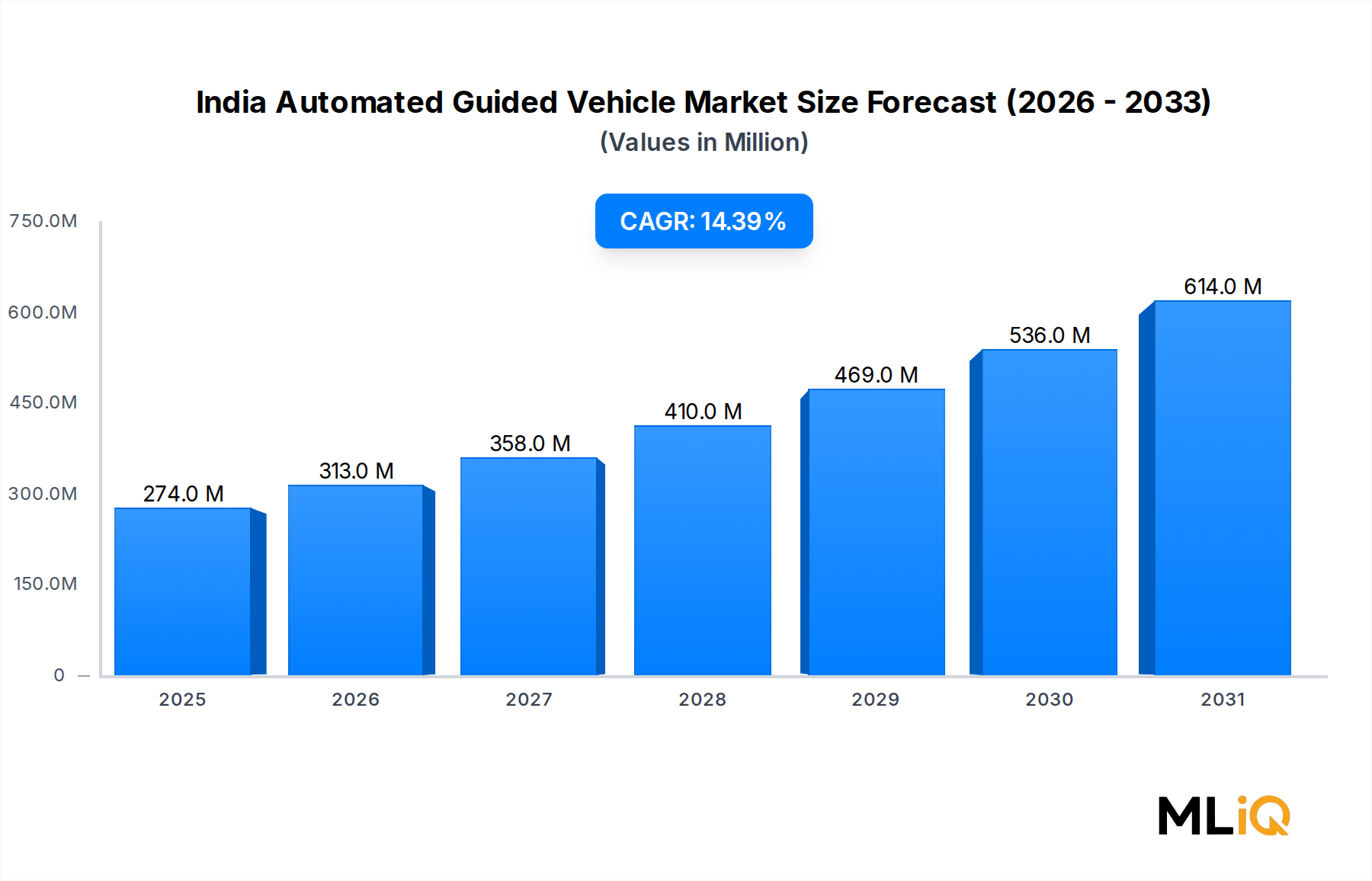

Dominant Segment Analysis in the India Automated Guided Vehicle Market

Among all vehicle type segments within the India Automated Guided Vehicle Market, unit load carriers represent the largest revenue-generating sub-segment, commanding a dominant share driven by their versatility across end-use industries. Unit load carriers are engineered to transport pallets, containers, bins, and flat goods across warehouse floors, manufacturing corridors, and distribution centers — making them the backbone of India's fast-expanding organized logistics infrastructure.

The dominance of unit load carriers is structurally anchored in India's e-commerce boom. With gross merchandise value of Indian e-commerce surpassing $70 billion annually, fulfillment center operators — including Amazon India, Flipkart, and Meesho — are scaling automated sortation and inventory movement capabilities. Unit load carriers are central to these deployments because they integrate seamlessly with conveyor systems, automated storage and retrieval systems (ASRS), and goods-to-person picking stations that modern fulfillment centers rely upon.

In manufacturing verticals, unit load carriers serve critical inter-station material transport roles. Automotive plants in Pune, Chennai, and Manesar utilize these vehicles to move body parts, sub-assemblies, and finished components between stamping, welding, painting, and final assembly zones. The scalability of unit load carrier fleets — operators can incrementally add vehicles as throughput demands grow — makes them particularly attractive for Indian manufacturers navigating unpredictable demand cycles.

The food and beverage sector further reinforces unit load carrier demand. Hygienic material handling requirements in FMCG production facilities align with the smooth-surface, low-maintenance operational characteristics of modern unit load carriers. Companies such as Hindustan Unilever, Nestlé India, and ITC have deployed automated material handling solutions in their larger production campuses.

Key players active within this segment include Toyota Material Handling India, which offers a range of load-carrier platforms engineered for Indian warehouse floor conditions, and GreyOrange, whose Ranger series blends AGV and autonomous mobile robot capabilities for flexible load transport. ATI Motors Pvt. Ltd. has also made significant inroads with its Sherpa series, purpose-built for Indian manufacturing environments, offering load capacities suited to mid-scale industrial deployments.

The segment's market share is not merely holding — it is consolidating. As Indian manufacturers shift from semi-automated to fully automated internal logistics, unit load carriers are upgraded from supplementary tools to mission-critical infrastructure. This shift is pushing average fleet sizes upward, from single-digit deployments at pilot stage to multi-dozen installations in full-production rollouts. Industry data indicates average fleet size per greenfield facility grew by approximately 35% between 2021 and 2024, signaling that the segment's share trajectory is one of active expansion rather than static dominance.

Navigation technology within this segment is evolving toward laser guidance and vision guidance from older magnetic tape solutions, improving positional accuracy and enabling more complex routing logic. This technology upgrade cycle is prompting existing unit load carrier customers to refresh their fleets, generating a secondary replacement demand wave that sustains revenue momentum within the segment.