Life Insurance Dominance in the Bancassurance Market

Within the Bancassurance Market segmented by insurance type, Life Insurance consistently commands the largest revenue share, accounting for an estimated 55–60% of total bancassurance premiums globally. This dominance is deeply structural, rooted in the natural alignment between banking relationships and long-term financial planning behaviors that life insurance products address.

Life insurance products — including term life, whole life, endowment plans, unit-linked insurance plans (ULIPs), and annuities — are inherently complementary to core banking products such as home loans, savings accounts, and retirement planning services. Banks possess a unique vantage point: they hold comprehensive financial data about their customers, enabling relationship managers to identify life-stage triggers (mortgage origination, marriage, childbirth, retirement planning) that create natural selling moments for life insurance products.

The structural alignment between Life Insurance Market dynamics and banking distribution is further reinforced by the premium economics of life products. Life insurance policies, particularly savings-linked and investment-linked varieties, carry higher average premiums and longer policy durations compared to general or non-life products, generating more sustained commission income streams for banking partners. This economic profile makes life insurance the preferred product category for bancassurance channel investment.

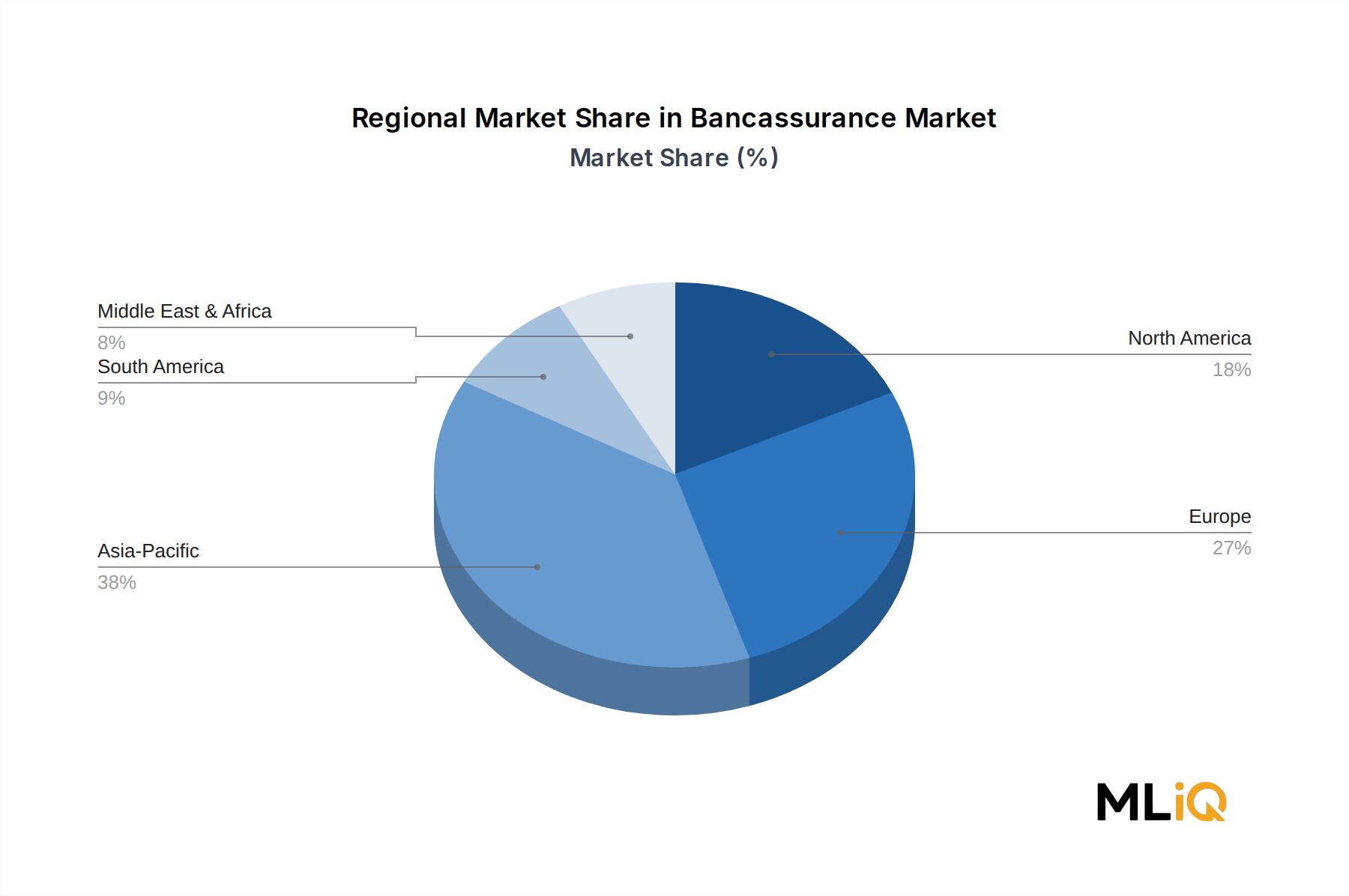

In Europe — particularly France, Italy, Spain, and Belgium — bancassurance has historically been the dominant channel for life insurance distribution, with bank-distributed life insurance premiums exceeding 40–50% of total life premiums in these markets. French banks such as Crédit Agricole and BNP Paribas have fully integrated insurance subsidiaries, offering a vertically integrated financial holding model that maximizes revenue retention within the banking group.

In Asia Pacific, the Life Insurance Market via bancassurance has experienced explosive growth. China, India, and ASEAN markets have seen banks partnering with major insurers to distribute savings-oriented life products to a rapidly expanding middle class. State Bank of India, through its strategic tie-ups with SBI Life Insurance, exemplifies the scale at which bancassurance life insurance distribution operates in emerging markets — with millions of policies distributed annually through a network of over 22,000 branches.

Key players driving life insurance dominance within bancassurance include BNP Paribas (through BNP Paribas Cardif), HSBC Group (through HSBC Life), Mitsubishi UFJ Financial Group in Japan, and Scotiabank across Latin America. These institutions have invested heavily in product design, digital onboarding, and relationship manager training to maximize conversion rates within their customer bases.

The life insurance segment's share within bancassurance is not merely stable — it is consolidating further as banks invest in proprietary insurance capabilities. The trend toward financial holding and joint venture models, where banks take equity stakes in insurance entities, deepens the strategic commitment to life insurance distribution and aligns the incentives of banking and insurance management teams.

However, competitive pressure within the life insurance bancassurance segment is intensifying. Digital-first insurtech entrants are beginning to partner directly with neobanks and digital banking platforms, challenging incumbent arrangements. This dynamic is accelerating innovation in product bundling, digital underwriting, and instant policy issuance — capabilities that incumbent bancassurers must develop to maintain their structural advantage.

Non-Life Insurance Market products, while growing within bancassurance channels — particularly home insurance, travel insurance, and credit-linked accident coverage — remain secondary in premium contribution, typically representing 40–45% of bancassurance revenues globally. Their growth is, however, notable in markets with expanding property ownership and mandatory insurance requirements.