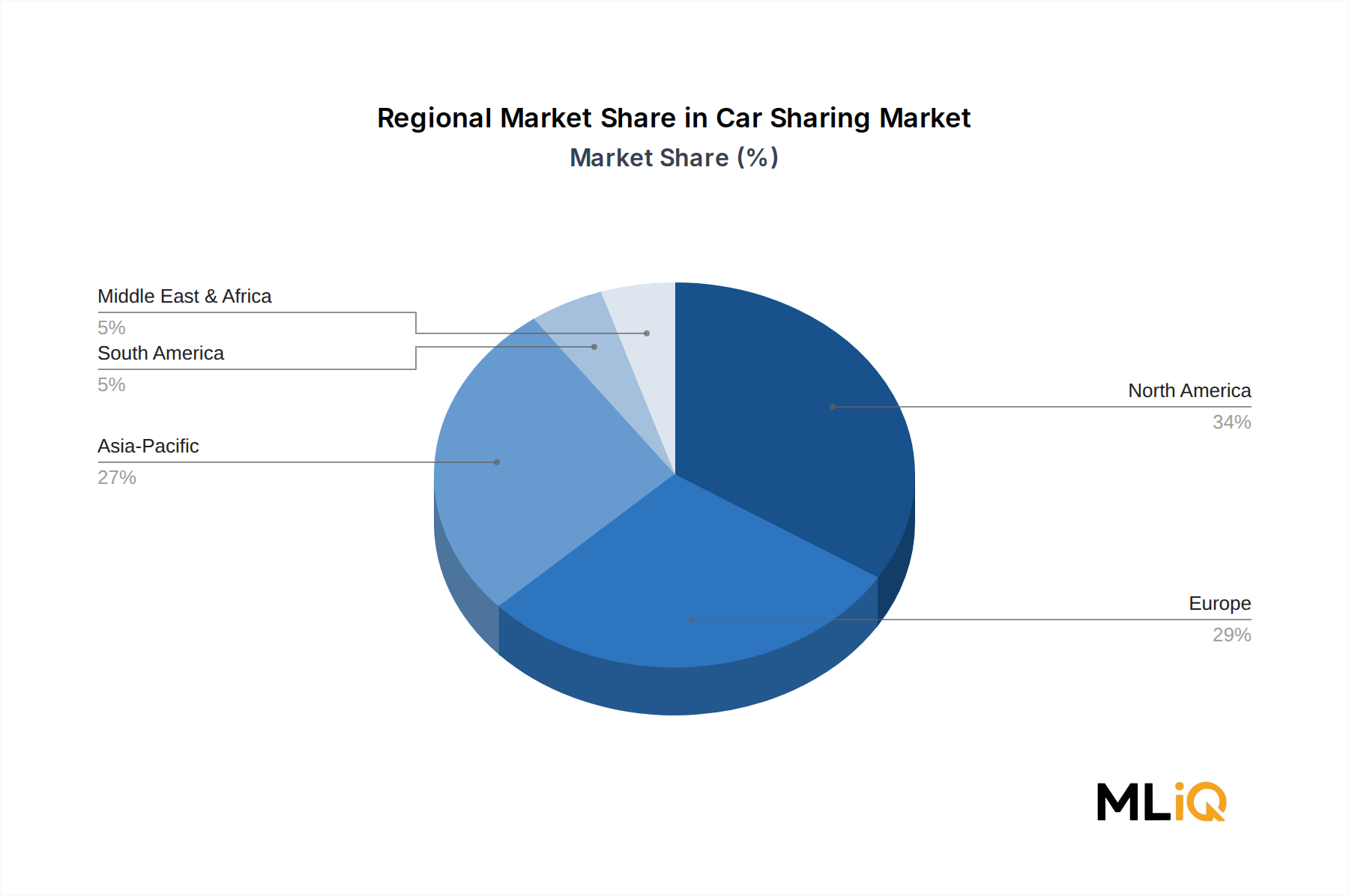

The car sharing market exhibits pronounced regional heterogeneity in terms of maturity, growth velocity, and dominant use-case profile.

North America represents the largest single regional revenue contributor, accounting for approximately 35–38% of global market value in the base year. The United States anchors this share, driven by high smartphone penetration, mature digital payment infrastructure, and a well-established peer-to-peer rental ecosystem led by platforms such as Turo Inc. and Getaround. The North American market is growing at an estimated regional CAGR of 17–19%, slightly below the global average, reflecting relative market maturity. Canada and Mexico represent incremental growth opportunities, particularly in Montreal, Toronto, and Mexico City, where municipal governments are actively incentivizing shared mobility adoption.

Europe is the second-largest region and arguably the most operationally sophisticated car sharing market globally. Germany, France, the United Kingdom, and the Benelux countries collectively generate approximately 30% of global revenue. European regulatory leadership — including urban low-emission zones, carbon pricing mechanisms, and dedicated shared mobility parking infrastructure — creates a uniquely favorable operating environment. The regional CAGR is estimated at 18–20%, supported by continued fleet electrification and free-float expansion.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 24–27% through 2033, driven by China, India, Japan, South Korea, and ASEAN urbanization dynamics. China alone represents a transformative opportunity, with over 60 cities exceeding 1 million population and a digitally native consumer base that has rapidly adopted app-based mobility services. India's car sharing market remains nascent but is scaling rapidly as per-capita income rises and urban congestion worsens. Singapore has emerged as the region's operational benchmark, with Goldbell Engineering Pte. Ltd. and international operators competing in a dense, tech-forward market.

The Middle East and Africa region, while smaller in absolute terms, is one of the most dynamic emerging markets. The GCC — particularly the UAE and Saudi Arabia — is investing heavily in smart city infrastructure, with Dubai's integrated mobility strategy serving as a regional template. Ekar Car Rental LLC's growth trajectory exemplifies the region's appetite for flexible mobility solutions. Regional CAGR is estimated at 22–25%.

South America remains the least developed major region, with Brazil and Argentina representing the primary markets. Infrastructure constraints, currency volatility, and regulatory uncertainty moderate growth, though urban centers such as São Paulo and Buenos Aires are witnessing early-stage platform proliferation.